- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

How a 70 Percent Trade-In Surge on iPhone 17 Launch May Shape ATRenew (RERE) Investor Outlook

- ATRenew announced a 70% surge in consumer trade-in orders on the first day of Apple's iPhone 17 launch compared to last year's iPhone 16 debut.

- This rapid rise, combined with ongoing collaborations with Xiaomi and Huawei, highlights ATRenew’s ability to benefit from technology upgrade cycles and broaden its supply channels.

- We'll explore how ATRenew's sharp increase in trade-in orders during a major product launch could influence its investment outlook.

This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

ATRenew Investment Narrative Recap

To be a shareholder in ATRenew, you need to believe in the long-term growth of China's device recommerce market, supported by rising consumer trade-in activity and strong brand collaborations. The recent 70% surge in iPhone 17 launch trade-ins underscores ATRenew's exposure to cyclical upgrade events, a key short-term catalyst for transaction volume, but competitive pressure from direct trade-in programs and other marketplaces remains the biggest risk and is unchanged by this news.

Among recent developments, ATRenew's continued share buyback program stands out for its relevance. Ongoing buybacks reflect management's confidence and may provide support for the stock price during periods of heightened volatility, especially as trade-in demand surges from major tech launches. However, in contrast, competitive threats from both multinational electronics brands and alternative marketplaces pose structural risks investors should be aware of if...

Read the full narrative on ATRenew (it's free!)

ATRenew's narrative projects CN¥35.8 billion revenue and CN¥1.1 billion earnings by 2028. This requires 24.5% yearly revenue growth and an increase of approximately CN¥890 million in earnings from current earnings of CN¥210.4 million.

Uncover how ATRenew's forecasts yield a $7.00 fair value, a 54% upside to its current price.

Exploring Other Perspectives

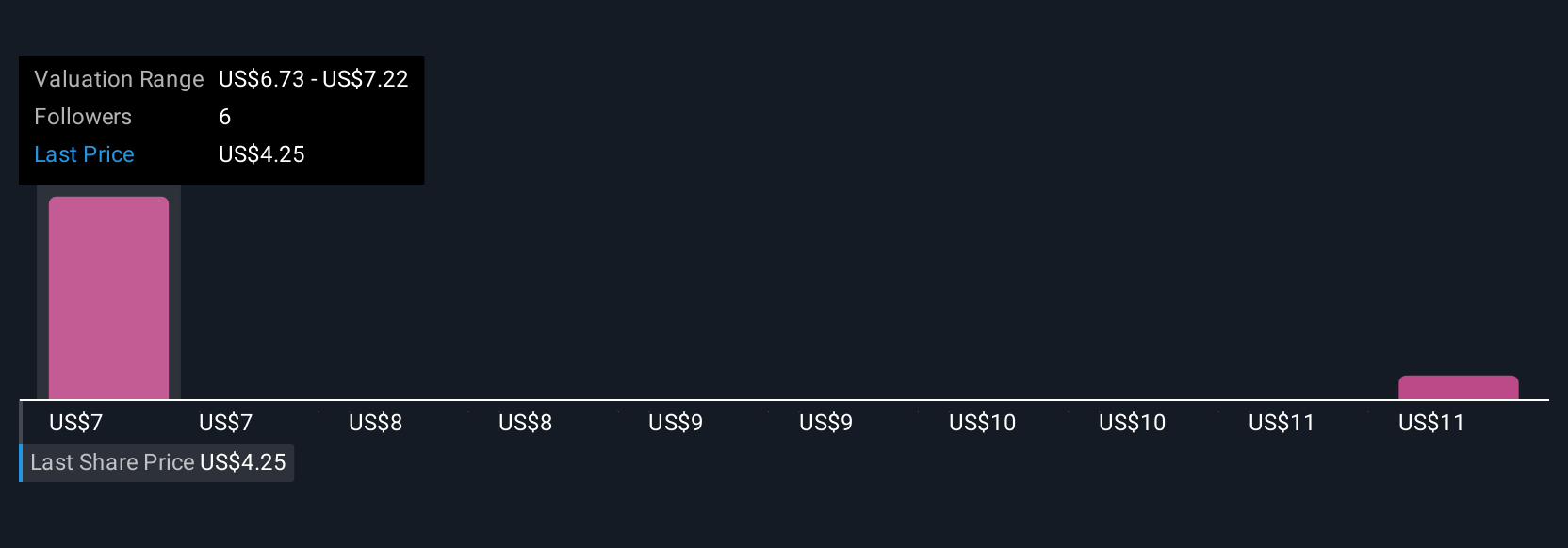

Three members of the Simply Wall St Community estimate ATRenew’s fair value between $6.72 and $11.64 per share. As expectations for trade-in growth remain high, participants are encouraged to consider how increased competition could influence future results.

Explore 3 other fair value estimates on ATRenew - why the stock might be worth just $6.72!

Build Your Own ATRenew Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your ATRenew research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free ATRenew research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate ATRenew's overall financial health at a glance.

Ready For A Different Approach?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- AI is about to change healthcare. These 31 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com