- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Butterfly Network, Inc.'s (NYSE:BFLY) P/S Is Still On The Mark Following 37% Share Price Bounce

Butterfly Network, Inc. (NYSE:BFLY) shareholders are no doubt pleased to see that the share price has bounced 37% in the last month, although it is still struggling to make up recently lost ground. Longer-term shareholders would be thankful for the recovery in the share price since it's now virtually flat for the year after the recent bounce.

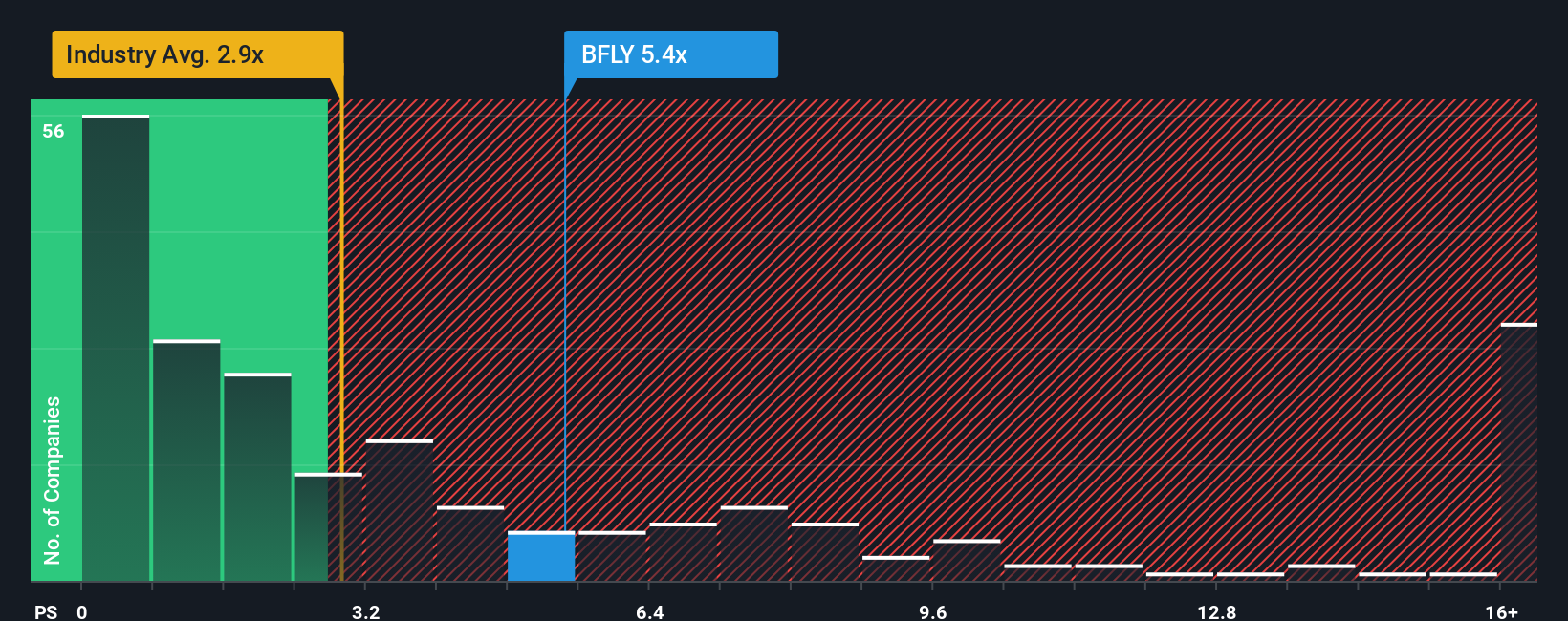

Following the firm bounce in price, given around half the companies in the United States' Medical Equipment industry have price-to-sales ratios (or "P/S") below 2.9x, you may consider Butterfly Network as a stock to avoid entirely with its 5.4x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/S.

View our latest analysis for Butterfly Network

How Butterfly Network Has Been Performing

With revenue growth that's superior to most other companies of late, Butterfly Network has been doing relatively well. The P/S is probably high because investors think this strong revenue performance will continue. However, if this isn't the case, investors might get caught out paying too much for the stock.

Want the full picture on analyst estimates for the company? Then our free report on Butterfly Network will help you uncover what's on the horizon.How Is Butterfly Network's Revenue Growth Trending?

There's an inherent assumption that a company should far outperform the industry for P/S ratios like Butterfly Network's to be considered reasonable.

If we review the last year of revenue growth, the company posted a terrific increase of 23%. Revenue has also lifted 28% in aggregate from three years ago, mostly thanks to the last 12 months of growth. Therefore, it's fair to say the revenue growth recently has been respectable for the company.

Turning to the outlook, the next year should generate growth of 14% as estimated by the four analysts watching the company. That's shaping up to be materially higher than the 9.6% growth forecast for the broader industry.

In light of this, it's understandable that Butterfly Network's P/S sits above the majority of other companies. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Bottom Line On Butterfly Network's P/S

The strong share price surge has lead to Butterfly Network's P/S soaring as well. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

We've established that Butterfly Network maintains its high P/S on the strength of its forecasted revenue growth being higher than the the rest of the Medical Equipment industry, as expected. It appears that shareholders are confident in the company's future revenues, which is propping up the P/S. Unless the analysts have really missed the mark, these strong revenue forecasts should keep the share price buoyant.

Don't forget that there may be other risks. For instance, we've identified 3 warning signs for Butterfly Network that you should be aware of.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.