- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

A Look at Raymond James Financial’s Valuation as It Elevates AI Leadership and Boosts Tech Investment

If you’ve been tracking Raymond James Financial (RJF) lately, the headlines are all about AI. The firm just named David Solganik as its new head of AI strategy, with Stuart Feld stepping up as chief AI officer. What stands out is the size of RJF’s commitment: $975 million a year on technology, much of it funneled into AI initiatives. It is a bold move that signals leadership sees next-generation tech as a serious way to drive client value, boost efficiency, and stay ahead on compliance, all while maintaining the personal relationships that built the brand.

Alongside these executive changes, RJF’s stock performance has been quietly gathering steam. Shares are up over 45% in the past year, outpacing many peers in the diversified financials space. Short-term momentum has picked up too, with a 12% gain in the past three months. Investors have seen a steady drumbeat of AI-related investments and product launches, but this latest leadership change may be fueling expectations for even deeper transformation and future growth.

So, is RJF’s valuation now an opportunity, or has the recent AI excitement already been priced in by the market?

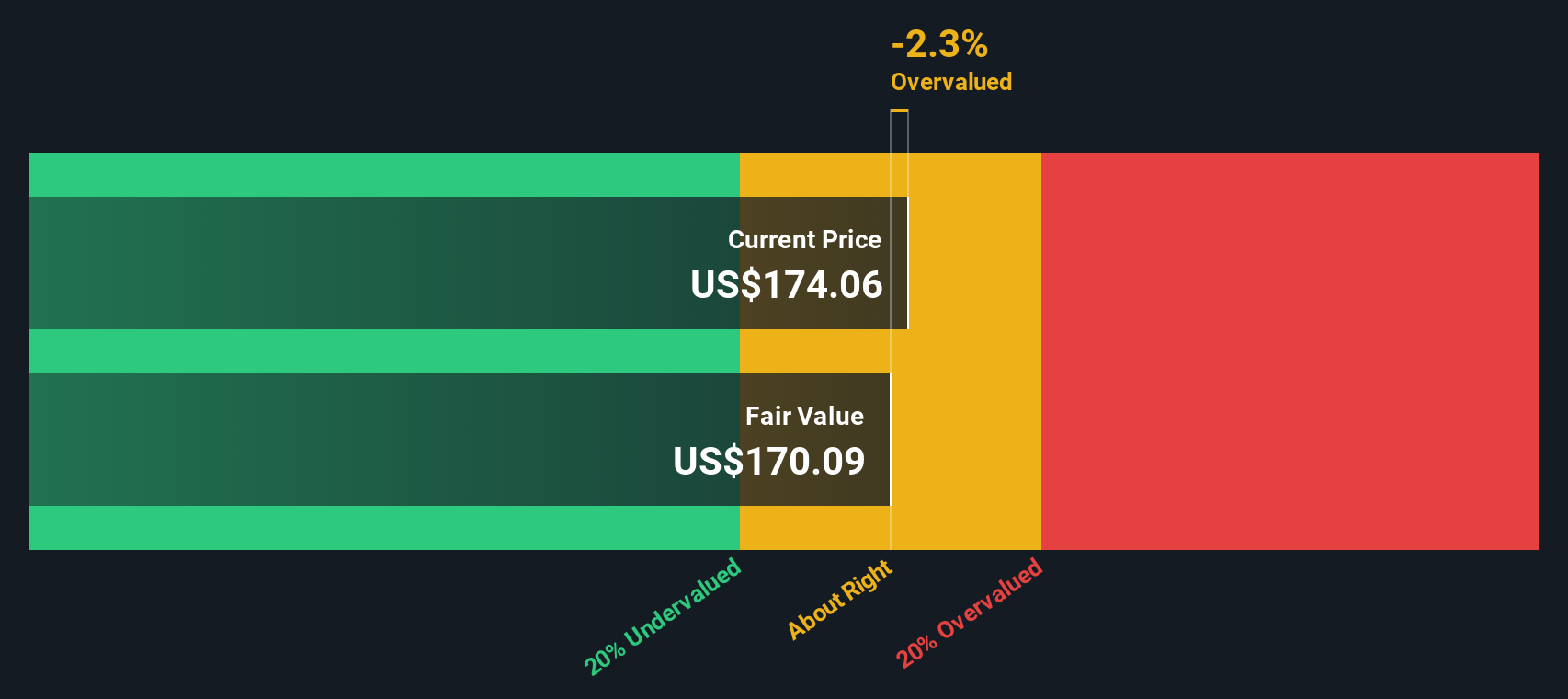

Most Popular Narrative: 3.8% Undervalued

According to the most widely followed narrative, Raymond James Financial is viewed as moderately undervalued. The fair value is estimated above the current share price, based on a blend of projected earnings growth, margin expansion, and future profitability assumptions.

Raymond James' successful recruiting of financial advisors with high trailing production and assets from other firms has bolstered client assets under administration. This is expected to drive future revenue growth through increased client assets and new business inflows.

The establishment of a Chief AI Officer role highlights Raymond James' investment in artificial intelligence to enhance financial professional capabilities and client service. This could potentially improve net margins through increased operational efficiencies.

Curious what’s fueling this undervaluation call? There is a growth engine in play here, fueled by ambitious profit targets and hidden leverage in future margins. The analyst narrative hints at long-term earnings power driving the fair value above today’s price. Want to see the precise projections behind this conviction? The real story lies in the detailed breakdown of the next few years.

Result: Fair Value of $173.27 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, heightened market volatility or delays in return on recent tech investments could cast doubt on analysts' optimism for steady earnings growth.

Find out about the key risks to this Raymond James Financial narrative.Another View: SWS DCF Model Weighs In

Taking a different angle, the SWS DCF model also suggests Raymond James Financial is trading below its estimated fair value. Both views point to upside. However, does the consensus miss something?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Raymond James Financial Narrative

If the consensus view doesn't quite match your perspective, you can dig into the numbers and craft your own narrative in just a few minutes. Do it your way.

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Raymond James Financial.

Looking for more investment ideas?

Ready to take charge of your investing journey? Find surprising opportunities, fresh growth trends, and powerful dividend plays using the handpicked tools below. These hidden gems could be your edge in the market.

- Uncover fast-moving companies with strong financials by checking out our list of penny stocks with strong financials.

- Spot the next leaders in artificial intelligence with a curated selection of AI penny stocks.

- Boost your portfolio’s cash flow with access to top picks among dividend stocks with yields > 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com