- LIVE QUOTES

- LEARN

- HELP

EN

A Look at Canadian Natural Resources (TSX:CNQ) Valuation Following New Debt Shelf Registrations

Canadian Natural Resources (TSX:CNQ) just filed two shelf registrations, paving the way to issue up to CA$3 billion in unsecured debt securities and an additional $4.5 billion in unsubordinated unsecured debt. Moves like this do not always mean new debt will hit the market right away, but they are watched closely, especially by investors trying to read the company’s next move. It could signal preparation for future investments, more cash for big projects, or simply a push to increase financial flexibility in a changing energy market.

This filing comes at a time when Canadian Natural Resources’ stock performance has been mixed. Shares have slipped about 5% year-to-date, despite growing nearly 3% over the last month. Looking farther back, the company’s longer-term returns have been much more encouraging, with a strong run-up over three and five-year periods, even as its revenue and net income dipped slightly over the past year. These recent developments and the company’s willingness to build up its financing toolkit are happening against a backdrop of shifting investor sentiment and changing risk appetite in the sector.

With the latest shelf registrations on the table and the stock’s momentum shifting, investors might be considering whether this represents a compelling entry point or if the market is already pricing in everything Canadian Natural Resources might do next.

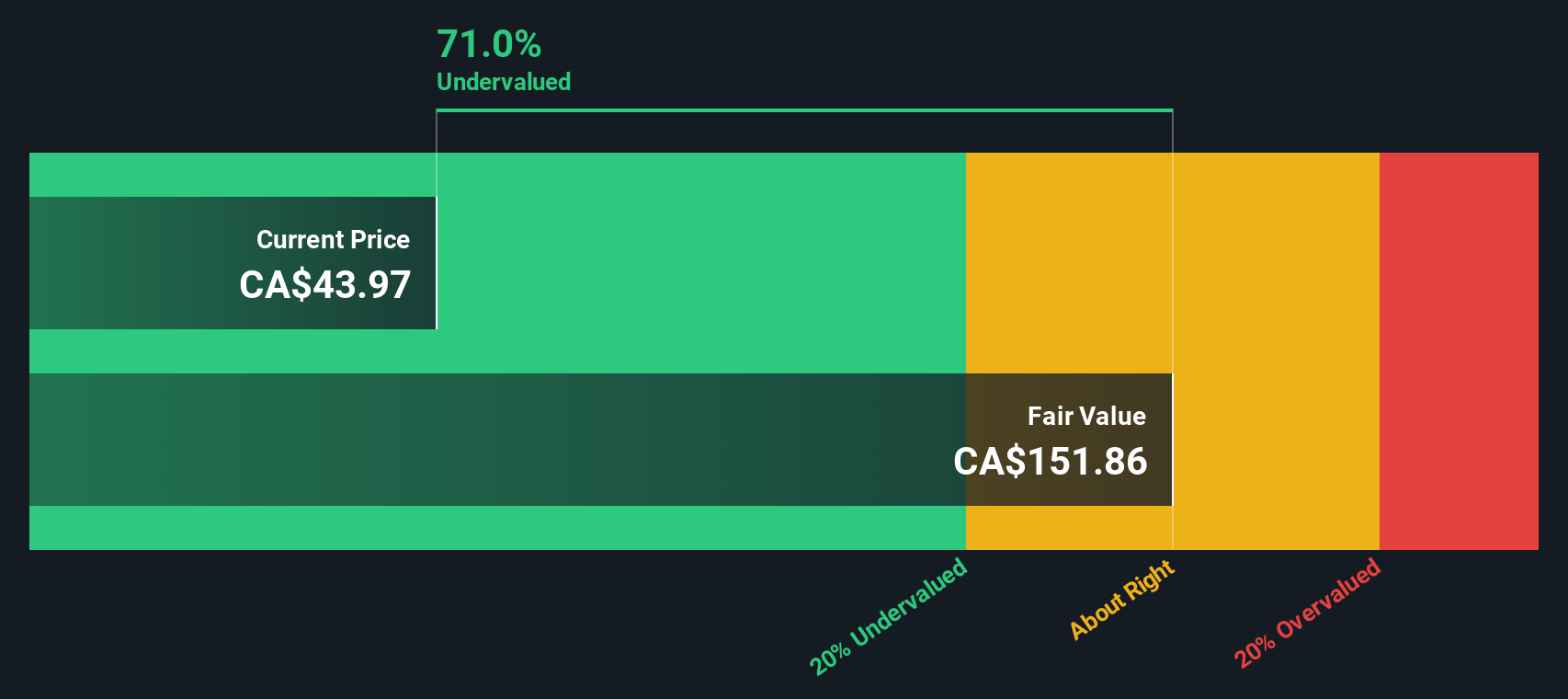

Most Popular Narrative: 18% Undervalued

The most widely followed narrative suggests Canadian Natural Resources is trading below its fair value, pointing to a potential upside for investors. This view is supported by expectations of stable earnings, enhanced margins, and strategic asset growth despite a challenging sector backdrop.

Recent accretive acquisitions have expanded production and reserves with minimal increase to the 2025 capital budget. This positions Canadian Natural for immediate cash flow growth and increased future revenues as these assets are developed. Operational execution and ongoing cost efficiencies, such as reduced drilling, completion, and operating costs across both oil and gas segments, are lowering the company's operating breakeven. This should sustainably expand net margins and free cash flow.

Want to know what is fueling this undervaluation? The main driver is a mix of margin expansion and future profit growth that rivals top industry performers. Curious which forecasts and hidden assumptions are setting this price target? Explore the key numbers and discover the calculations pushing this narrative higher.

Result: Fair Value of $52.14 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, persistent pipeline bottlenecks and increasing regulatory scrutiny could disrupt Canadian Natural Resources' growth path and challenge the bullish valuation narrative.

Find out about the key risks to this Canadian Natural Resources narrative.Another View: SWS DCF Model

While most analysts see Canadian Natural Resources as undervalued using future earnings and industry multiples, our SWS DCF model comes to the same conclusion from a cash flow perspective. Could both methods be missing a hidden risk?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Canadian Natural Resources Narrative

If you see things differently or want to dig deeper into the numbers, it's easy to draw your own conclusions and shape your own outlook for Canadian Natural Resources. You can do this in under three minutes. Do it your way

A great starting point for your Canadian Natural Resources research is our analysis highlighting 5 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Why stop at one opportunity? Make your money work even harder by checking out handpicked collections of fast-growing and resilient companies other investors might be missing.

- Uncover companies with robust potential and strong balance sheets by browsing our selection of penny stocks with strong financials, which may offer opportunities for growth and financial stability.

- Explore the next generation of healthcare with our collection of innovators in medical technology and artificial intelligence through healthcare AI stocks.

- Find high-value opportunities with stocks considered undervalued based on key fundamentals in our handpicked group of undervalued stocks based on cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com