- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Insperity (NSP): Valuation in Focus After Earnings Miss, Guidance Cut, and Legal Investigation

Most Popular Narrative: 7.4% Undervalued

The latest consensus narrative points to Insperity trading below fair value. Analysts view the current share price as offering a discount based on long-term earnings prospects and margin expansion potential.

The upcoming launch of Insperity HRScale, a joint solution with Workday, targets a broader and more lucrative mid-market segment. By leveraging both advanced HR technology and comprehensive services, this initiative is expected to drive higher revenue growth and improved operating leverage. Premium pricing and larger average client size become possible as a result.

Curious how analysts arrived at this optimistic valuation? The secret lies in aggressive forecasts around revenue recovery, margin improvement, and one especially bold profit assumption. Want to uncover which ambitious numbers are baked into this fair value calculation? The answers could reshape your outlook on Insperity’s future.

Result: Fair Value of $57.75 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, persistent rises in healthcare costs and challenges in executing the Workday partnership could quickly undermine this bullish outlook for Insperity.

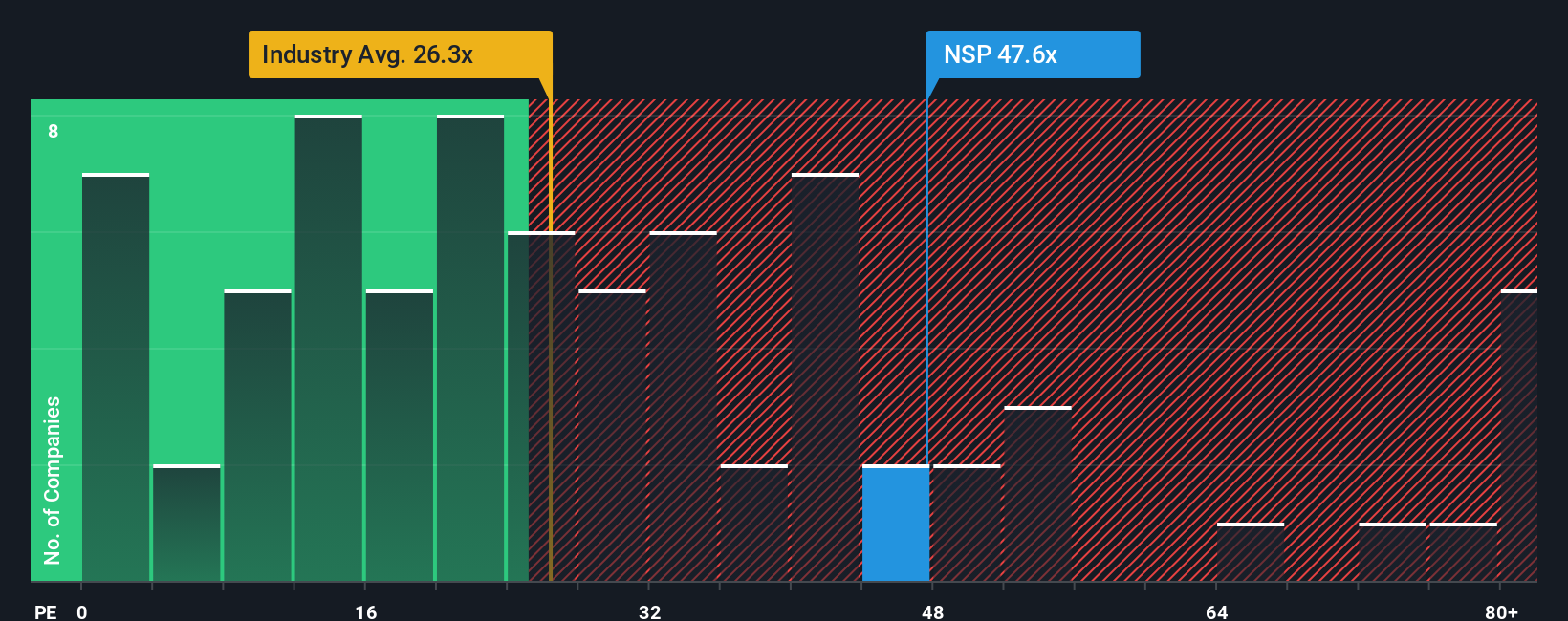

Find out about the key risks to this Insperity narrative.Another View: Market-Based Comparison

While analyst forecasts suggest Insperity could be undervalued, a market-based lens paints a more skeptical picture. Compared to the industry, the company’s current share price looks expensive. Which lens truly reflects reality?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Insperity Narrative

If you want to check the numbers for yourself or have your own interpretation, you can build your personal narrative in just a few minutes. Do it your way.

A great starting point for your Insperity research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Stay ahead by finding investment opportunities others might overlook. Use the Simply Wall Street Screener to uncover stocks with unique potential that could fit your strategy.

- Unlock high-yield potential and spot stable returns by checking out dividend stocks with yields > 3%, which consistently deliver more than 3% dividend yields.

- Get ahead of the curve with rapidly growing healthcare breakthroughs by browsing through healthcare AI stocks, leading the charge in AI-driven medical innovations.

- Seek out bargains before the crowd notices by zeroing in on undervalued stocks based on cash flows, currently trading below their intrinsic value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com