- LIVE QUOTES

- LEARN

- HELP

EN

Evaluating CT REIT (TSX:CRT.UN): Is There More Value After Recent Share Price Momentum?

If you have been watching CT Real Estate Investment Trust (TSX:CRT.UN), you might have noticed the recent uptick in its share price this month. There is no single headline-grabbing event behind this move. Such positive momentum often gets investors wondering if a shift in sentiment is underway, or if this is just a pause before the next leg up or down.

So far this year, CT Real Estate Investment Trust has made steady progress, with yearly returns outpacing the wider market. The past month in particular has seen shares continue their climb, building on modest gains over the past three months. While there have not been major announcements or fundamental changes recently, the ongoing trend hints at renewed interest and perhaps a changing view on the company’s growth prospects.

Is the current price reflecting all the future upside, or could there still be overlooked value for investors willing to take a closer look?

Price-to-Earnings of 19.2x: Is it justified?

CT Real Estate Investment Trust currently trades at a price-to-earnings (P/E) ratio of 19.2x, which is lower than the North American Retail REITs industry average of 25.4x. This suggests the stock may be undervalued compared to its sector peers.

The P/E ratio compares a company’s share price to its earnings per share. It offers investors a quick measure of market expectations for future growth and profitability. For Real Estate Investment Trusts, P/E is a frequently used metric because it reflects how much investors are willing to pay for earnings generated from property rents and related income.

Given that CRT.UN trades below the industry average, investors might be discounting the company, despite its solid growth in recent years. However, this valuation could reflect moderate growth expectations or concerns about sustainability of recent gains.

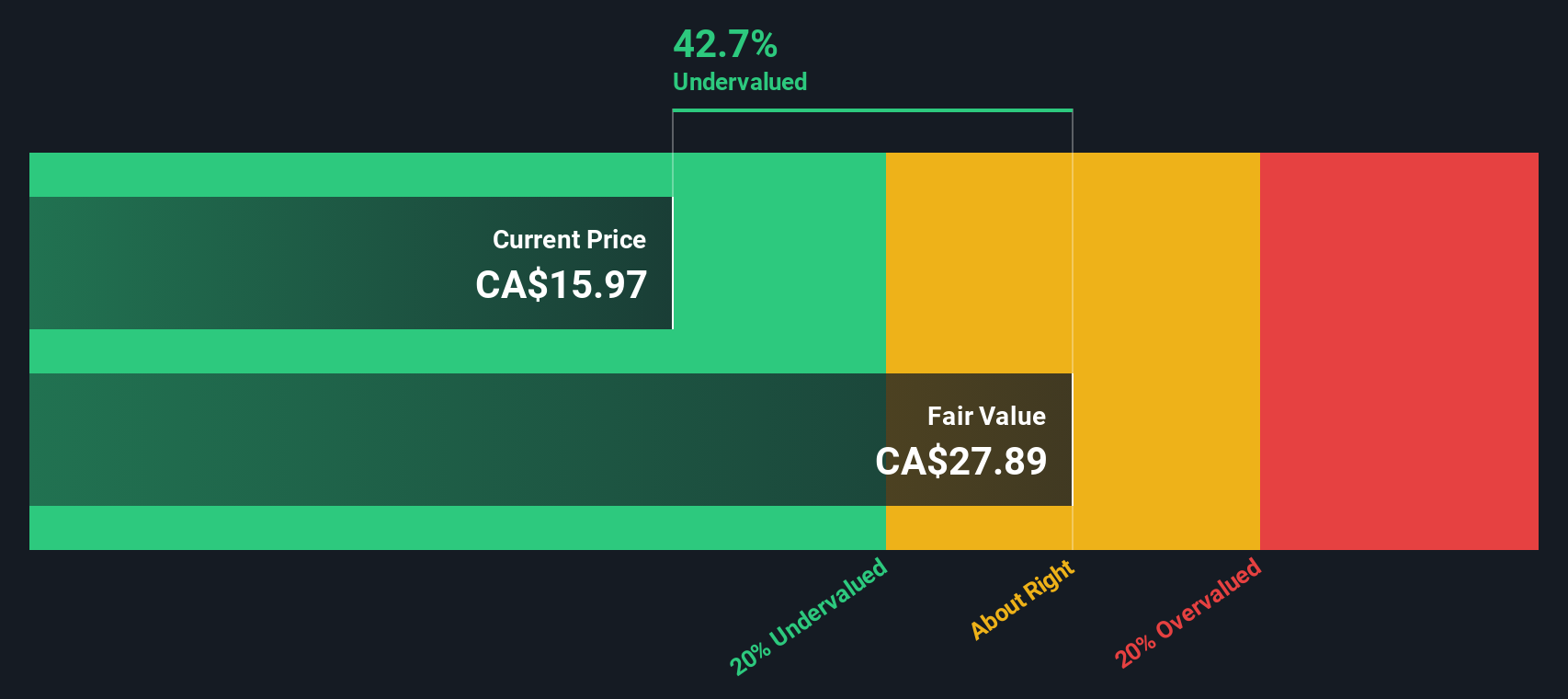

Result: Fair Value of $26.58 (UNDERVALUED)

See our latest analysis for CT Real Estate Investment Trust.However, moderate revenue growth and potential concerns about sustaining recent gains could limit further upside in CT Real Estate Investment Trust shares.

Find out about the key risks to this CT Real Estate Investment Trust narrative.Another View: What Does Our DCF Model Say?

Looking at CT Real Estate Investment Trust through the lens of our SWS DCF model offers a similar perspective and suggests that the company may indeed be undervalued. However, can two methods really agree, or could the reality lie somewhere in between?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own CT Real Estate Investment Trust Narrative

Of course, if you see the numbers differently or want to dig deeper into the details yourself, you can put together your own view in just a few minutes. Do it your way.

A great starting point for your CT Real Estate Investment Trust research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Unlock even more investing opportunities with our top hand-picked lists. Miss out now and you might overlook tomorrow’s best performers. Set yourself up for smarter decisions.

- Uncover companies benefiting from robust recurring payouts as you tap into dividend stocks with yields > 3% for income potential above 3% yields.

- Spot hidden gems in rapidly evolving medical technology by starting your search with innovative healthcare AI stocks leaders transforming healthcare through AI.

- Stay ahead of major tech shifts by targeting high-potential disruptors with our quantum computing stocks focused on quantum computing breakthroughs.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com