- LIVE QUOTES

- LEARN

- HELP

EN

Acadia Realty Trust (AKR): Valuation in Focus After Fresh Analyst Buy Ratings and Insider Selling Trends

Acadia Realty Trust (AKR) has come back onto investors’ radars after analysts at Bank of America Securities and Jefferies both maintained their Buy ratings this month. These reaffirmations from major institutions are shining a spotlight on the real estate trust, even as company insiders are moving the opposite way with an uptick in insider selling. It is not unusual for positive analyst coverage and rising insider selling to send mixed signals, so it is no surprise that many investors are now taking a closer look at what is driving the story.

This renewed attention has had an impact. After a challenging start to the year, AKR’s stock has seen a moderate turnaround, gaining over 5% in the past month and in the past three months, despite being down around 7% over twelve months and still in the red year-to-date. The long-term view tells a different story, with impressive three- and five-year returns reminding investors that momentum for this retail-focused REIT can shift quickly. Recent analyst votes of confidence are adding new energy, but the divergence with insider activity is raising questions about where the balance of risk and reward stands now.

So is the market underestimating AKR’s potential after a muted year, or have these new developments already been factored into the price? Let us dig into the valuation picture next.

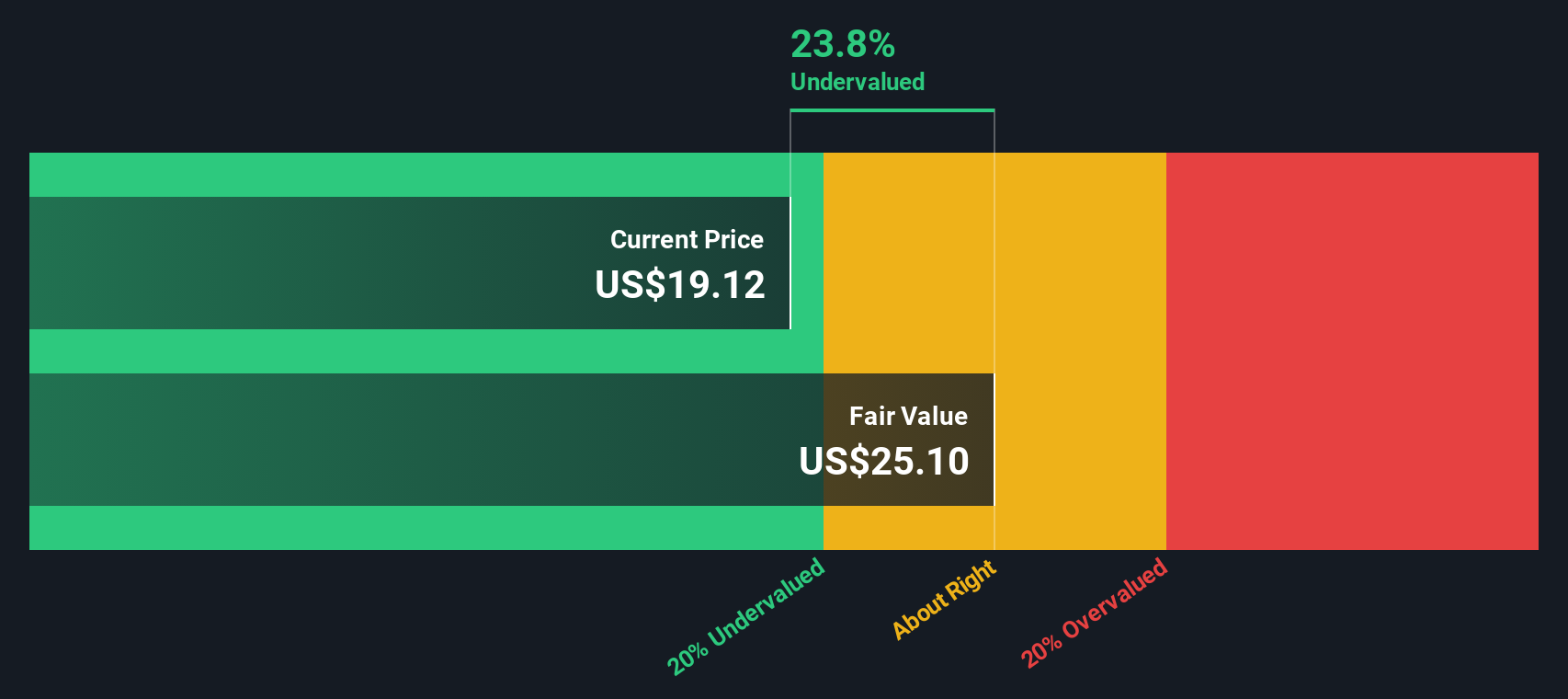

Most Popular Narrative: 11.6% Undervalued

According to community narrative, Acadia Realty Trust is currently being valued at a notable discount to its estimated fair value. This reflects analyst optimism about future growth drivers, balanced against distinct risks.

The company’s outsized exposure to dense, affluent urban corridors—where urbanization trends and demographic shifts continue to drive premium consumer demand and limited new retail development—supports strong occupancy rates, rent increases, and margin expansion. Acadia’s ability to proactively “pry loose” and re-lease under-market spaces at double-digit rent spreads, especially across high-growth corridors where they control a critical mass of storefronts, provides a clear path to accelerating net operating income (NOI) and revenue growth.

Curious why Wall Street thinks Acadia’s urban retail empire deserves a double-digit uplift? The narrative hints at rapid gains in profitability and a future profit multiple that breaks the mold for retail REITs. Want to see how bullish rent growth assumptions and an ambitious earnings forecast stack up beneath this eye-catching valuation? The story behind the numbers might surprise you.

Result: Fair Value of $22.67 (UNDERVALUED)

--- Here is your revised article text, with all em dashes removed and replaced with better formatting:Most Popular Narrative: 11.6% Undervalued

According to community narrative, Acadia Realty Trust is currently being valued at a notable discount to its estimated fair value. This reflects analyst optimism about future growth drivers, balanced against distinct risks.

The company’s outsized exposure to dense and affluent urban corridors, where urbanization trends and demographic shifts continue to drive premium consumer demand and limited new retail development, supports strong occupancy rates, rent increases, and margin expansion. Acadia’s ability to proactively "pry loose" and re-lease under-market spaces at double-digit rent spreads, especially across high-growth corridors where it controls a critical mass of storefronts, provides a clear path to accelerating net operating income (NOI) and revenue growth.

Curious why Wall Street thinks Acadia’s urban retail holdings deserve a double-digit uplift? The narrative points to rapid gains in profitability and a future profit multiple that stands out among retail REITs. Interested in how bullish rent growth assumptions and an ambitious earnings forecast compare to this valuation? The story behind the numbers might surprise you.

Result: Fair Value of $22.67 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts. However, concentrated exposure to urban retail and changing consumer habits could challenge Acadia’s optimistic outlook if high-income demand or regulatory conditions shift unexpectedly. Find out about the key risks to this Acadia Realty Trust narrative.Another View: What Does the DCF Say?

While the community narrative points to undervaluation based on future earnings potential, our DCF model also suggests the stock is trading significantly below its intrinsic value. Could both methods be signaling an opportunity? Alternatively, are there hidden risks the numbers cannot capture?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Acadia Realty Trust Narrative

If you see the story differently, or would rather reach your own conclusions, the data is ready for you to build your own narrative in just a few minutes. do it your way.

A great starting point for your Acadia Realty Trust research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Do not limit your strategy to a single stock. With so many compelling opportunities in the market, make your next smart move by tapping into investment themes powered by insightful data. Connect with top trends and find companies that match your priorities. You do not want to miss what could be your next big winner.

- Target stable income by checking out dividend stocks with yields > 3%, which offers robust yields and strong fundamentals, making it ideal for building reliable cash flow.

- Capitalize on the surge in artificial intelligence by searching for AI penny stocks. These companies are positioned to disrupt industries and accelerate growth.

- Expand your portfolio into the quantum leap by exploring quantum computing stocks, which includes organizations at the forefront of tomorrow’s computing technology.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com