- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Why Valvoline (VVV) Is Up 5.2% After Raising Guidance on Strong Q3 Results and What's Next

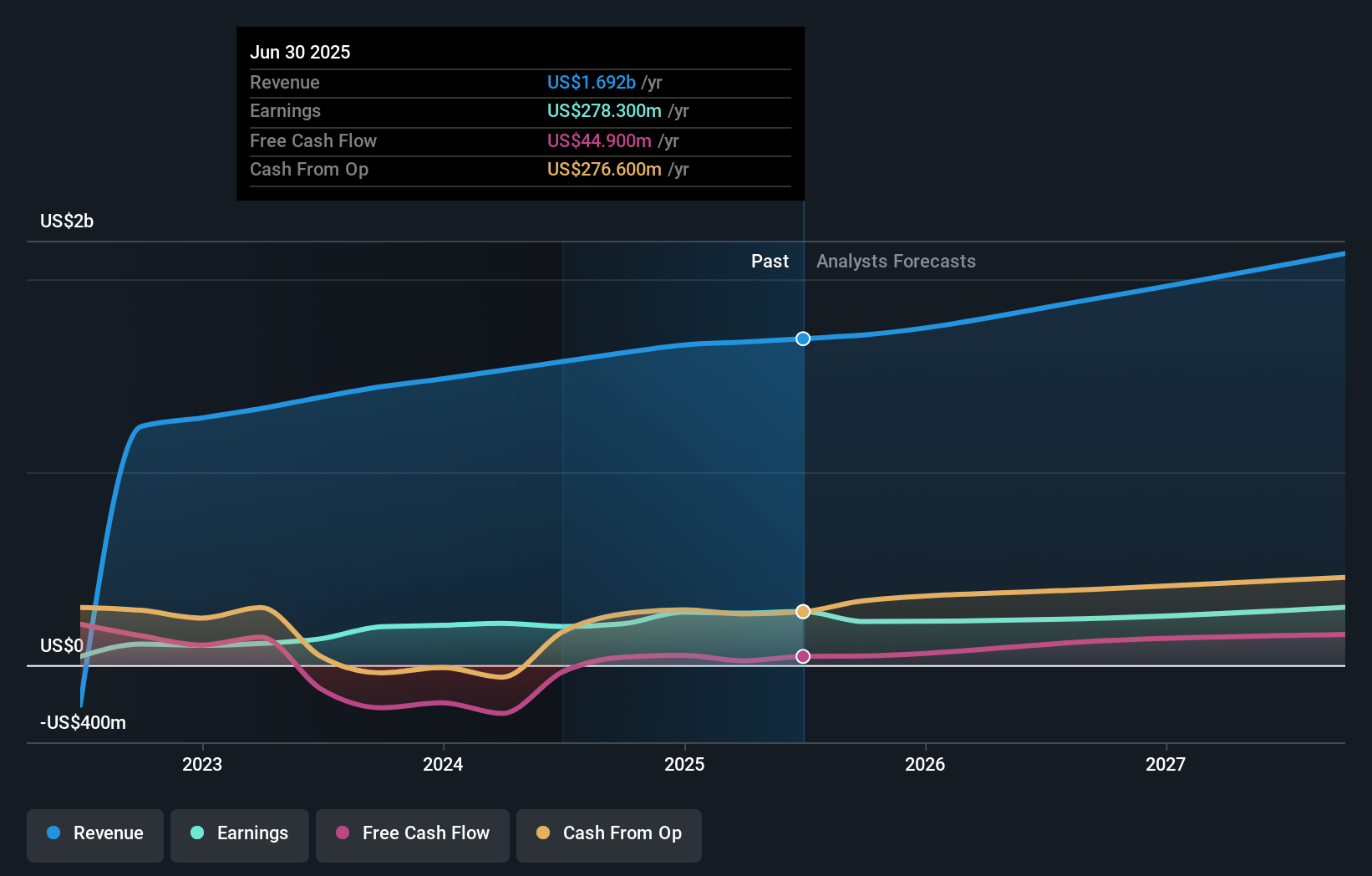

- Valvoline Inc. recently reported third-quarter 2025 earnings, revealing sales of US$439 million and net income of US$56.5 million, both increasing from the prior year, and also updated its full-year revenue guidance to US$1.69 billion–US$1.72 billion.

- These results highlight Valvoline's ability to grow both revenue and earnings, strengthening its outlook as it raises expectations for the remainder of the year.

- We'll explore how Valvoline's higher earnings guidance and solid profit gains shape its future investment narrative and industry position.

These 15 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

Valvoline Investment Narrative Recap

For Valvoline shareholders, the case centers on the company's ability to sustain profit growth in a maturing preventative maintenance industry, despite structural headwinds from the shift toward electric vehicles (EVs). The recent third-quarter earnings beat, with sales and net income up year over year and full-year revenue guidance slightly raised, points to solid execution. However, these results do not materially change the short-term catalyst of continued same-store sales growth nor do they reduce the biggest risk: the mounting EV transition and its longer-term impact on Valvoline's core business model.

Of the latest announcements, the plan to add 160 to 185 new store locations in 2025 stands out. This expansion effort is directly linked to Valvoline’s revenue growth catalyst, aiming to boost geographic reach and maximize exposure to the aging vehicle fleet still requiring regular maintenance. Store growth helps offset macro risks and supports near-term revenue, but its future effectiveness depends on evolving vehicle technology trends.

But while revenue is rising and expansion is underway, investors should be aware that the accelerating adoption of EVs still poses a structural risk to the business if...

Read the full narrative on Valvoline (it's free!)

Valvoline is projected to reach $2.3 billion in revenue and $194.6 million in earnings by 2028. This outlook assumes annual revenue growth of 10.5% and a decrease in earnings of $83.7 million from current earnings of $278.3 million.

Uncover how Valvoline's forecasts yield a $43.31 fair value, a 9% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community fair value estimates for Valvoline range from US$25.79 to US$43.31, reflecting three different viewpoints. With this diversity of opinion in mind, consider that continued store expansion may be supporting current revenue, but long-term growth faces challenges as more vehicles transition to EVs.

Explore 3 other fair value estimates on Valvoline - why the stock might be worth 35% less than the current price!

Build Your Own Valvoline Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Valvoline research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Valvoline research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Valvoline's overall financial health at a glance.

Seeking Other Investments?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Rare earth metals are the new gold rush. Find out which 27 stocks are leading the charge.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com