- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Gibraltar Industries' Margin Pressures and Lower Outlook Might Change The Case For Investing In ROCK

- Gibraltar Industries recently reported its second quarter 2025 results, showing sales increased to US$309.52 million while net income declined to US$26 million, and also issued full-year guidance below 2024 levels.

- The combination of rising sales but decreasing profitability, along with a lowered earnings outlook, highlights mounting pressures on operational margins despite top-line growth.

- We’ll examine how the reduced full-year earnings guidance impacts Gibraltar Industries’ investment narrative and future business prospects.

This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

Gibraltar Industries Investment Narrative Recap

To be a Gibraltar Industries shareholder, you’d need to be confident in the company’s ability to grow earnings from its core building products and structures businesses following its Renewables segment sale. The recent guidance cut and margin pressures do materially shift the near-term outlook, making sustained margin recovery and residential end-market stabilization the key catalyst and risk, respectively.

Among Gibraltar’s recent actions, the June announcement to sell the renewables business stands out, as it shifts the growth profile away from high-growth solar into more cyclical traditional construction markets, intensifying the importance of operational execution in residential and infrastructure segments for any rebound in financial results.

However, with interest rate pressures and affordability headwinds lingering in residential construction, investors should be aware that...

Read the full narrative on Gibraltar Industries (it's free!)

Gibraltar Industries' outlook forecasts $1.7 billion in revenue and $176.5 million in earnings by 2028. This scenario assumes a 9.9% annual revenue growth rate and a $43 million increase in earnings from the current $133.5 million.

Uncover how Gibraltar Industries' forecasts yield a $90.33 fair value, a 47% upside to its current price.

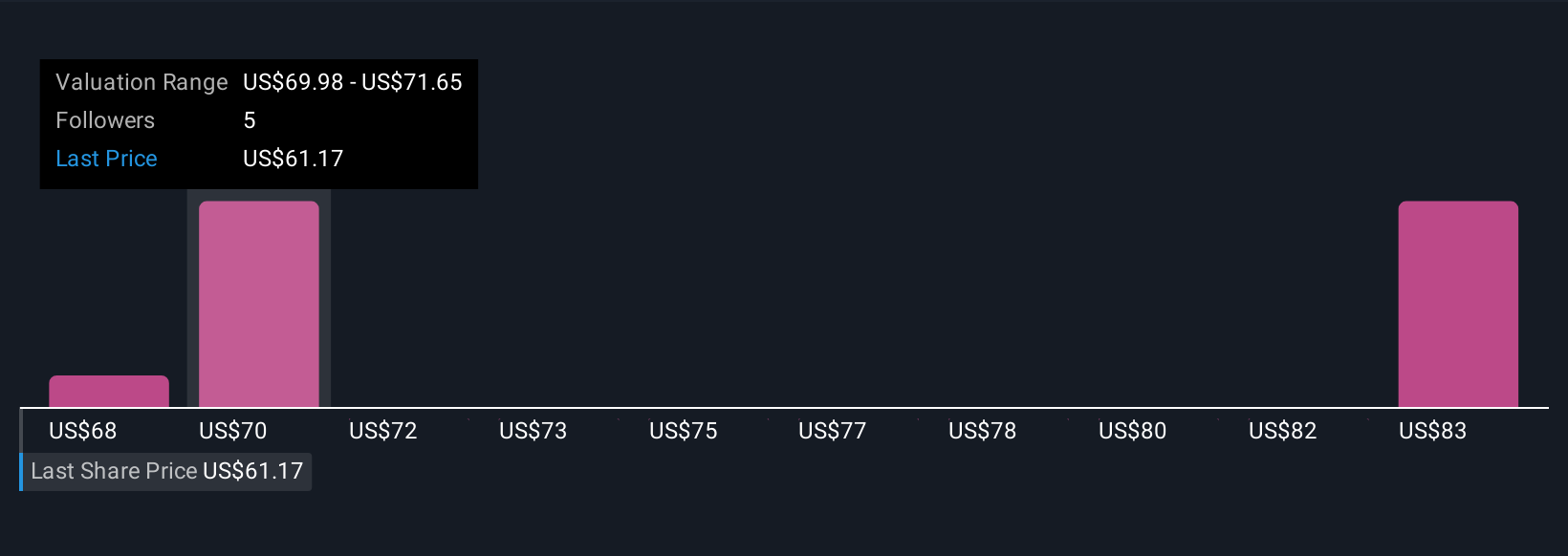

Exploring Other Perspectives

Fair value estimates from the Simply Wall St Community range from US$68.31 to US$90.33 based on three distinct forecasts. With residential market softness now a primary risk, consider how these varied outlooks might reflect differing views on Gibraltar’s ability to stabilize margins and grow earnings.

Explore 3 other fair value estimates on Gibraltar Industries - why the stock might be worth just $68.31!

Build Your Own Gibraltar Industries Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Gibraltar Industries research is our analysis highlighting 5 key rewards that could impact your investment decision.

- Our free Gibraltar Industries research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Gibraltar Industries' overall financial health at a glance.

Interested In Other Possibilities?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Rare earth metals are the new gold rush. Find out which 27 stocks are leading the charge.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 18 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com