- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Garmin (GRMN) Is Up 6.2% After Strong Q2 Results and Raised 2025 Revenue Guidance

- In the past week, Garmin reported second quarter earnings with sales rising to US$1.81 billion and net income reaching US$400.82 million, while also increasing its full-year revenue guidance to approximately US$7.1 billion for 2025.

- An interesting aspect of this report is the strong contribution from international markets, particularly EMEA, which exceeded analyst expectations and accounted for more than a third of total revenue.

- We'll explore how Garmin's raised full-year guidance following the robust quarterly results could influence its investment narrative going forward.

This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

Garmin Investment Narrative Recap

To be a Garmin shareholder, one needs confidence in the durability of its product innovation, strong brand across wearables and aviation, and geographically diverse revenue streams. The latest quarterly results, driven by robust sales and raised guidance, reinforce the idea that international growth, particularly in EMEA, is the most important near-term catalyst, while risks like a soft Marine segment and potential margin pressures remain, with this news not materially shifting the risk landscape just yet.

Among Garmin’s recent moves, the update on its share buyback program stands out as most relevant: the company completed the repurchase of 827,000 shares for US$156.8 million, reflecting continued execution on capital allocation priorities. This action sits alongside growth catalysts like product launches and margin improvement efforts, which remain central for supporting the company’s investment case as management seeks to build on positive momentum in its core markets.

However, investors should be aware that international revenue strength could be tested if...

Read the full narrative on Garmin (it's free!)

Garmin's outlook projects $8.2 billion in revenue and $1.9 billion in earnings by 2028. This scenario assumes an annual revenue growth rate of 8.2% and a $0.4 billion increase in earnings from the current level of $1.5 billion.

Uncover how Garmin's forecasts yield a $205.33 fair value, a 12% downside to its current price.

Exploring Other Perspectives

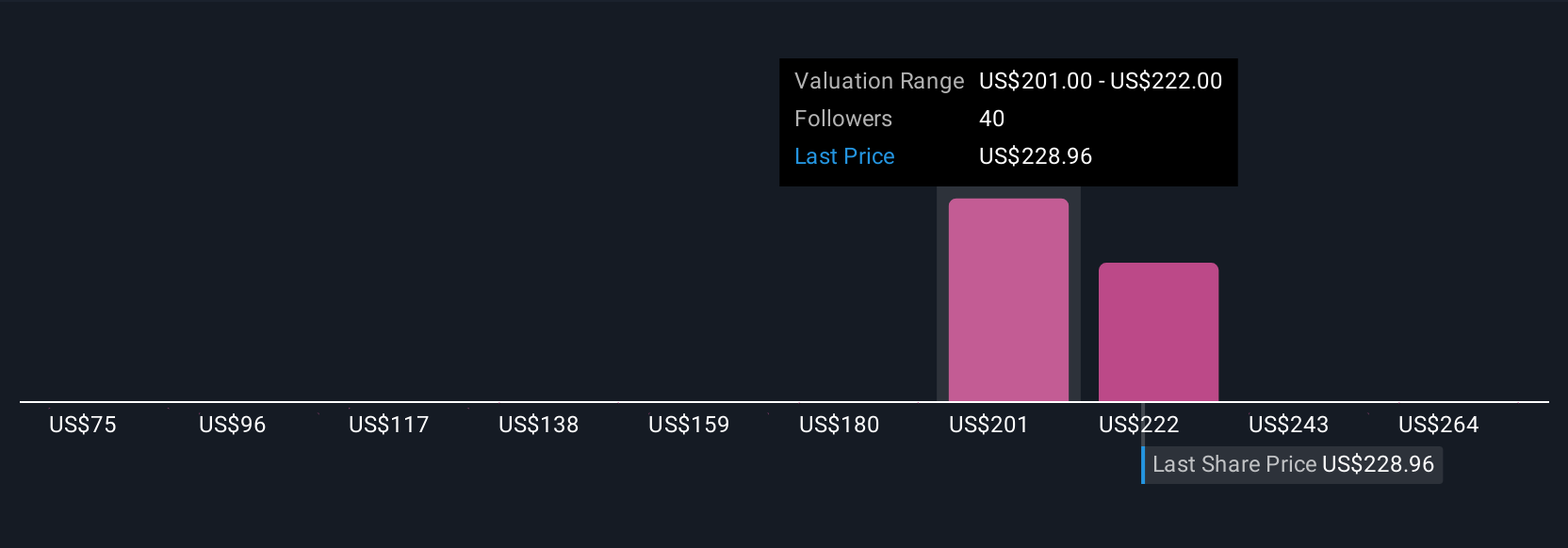

Simply Wall St Community members provided nine fair value estimates for Garmin, ranging from US$75 to US$285 per share. While opinions differ widely, many focus on international market contributions as pivotal for future returns, explore these contrasting perspectives in detail.

Explore 9 other fair value estimates on Garmin - why the stock might be worth as much as 23% more than the current price!

Build Your Own Garmin Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Garmin research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Garmin research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Garmin's overall financial health at a glance.

Curious About Other Options?

Our top stock finds are flying under the radar-for now. Get in early:

- Find companies with promising cash flow potential yet trading below their fair value.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 26 companies in the world exploring or producing it. Find the list for free.

- The end of cancer? These 26 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com