- LIVE QUOTES

- LEARN

- HELP

EN

China Index Research Institute: Relaxed policies and limited financing highlights the financing advantages of leading housing enterprises

The Zhitong Finance App learned that on July 11, the China Index Research Institute published an article stating that in the first half of 2025, good cities and good house projects will continue to improve, but the overall real estate market is still under some pressure. Housing enterprise financing support policies remain relaxed, the scale of bond financing continues to decline, and credit bonds and ABS have become the absolute main forces. The progress of debt restructuring has accelerated, and debt reduction has become an important choice for many housing enterprise restructuring plans, and debt risk mitigation is also expected to improve the industrial financing environment. Looking ahead to the second half of the year, the strengthening of policies is expected to drive the recovery of expectations, but the recovery of the real estate market still faces many challenges. The financing policy is still expected to maintain a relaxed trend, but the scale of financing will still be affected by market recovery.

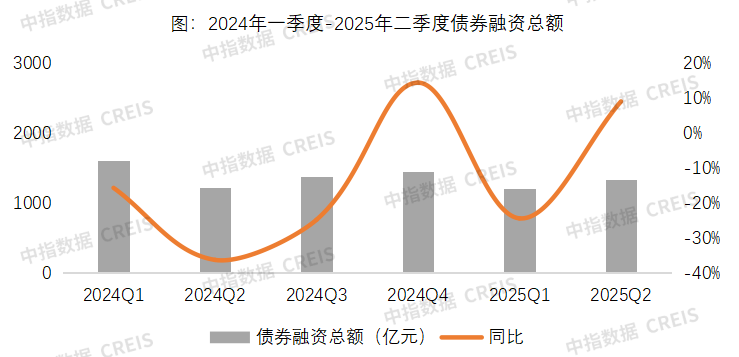

Financing scale: 10.0% year-on-year decrease, continuing the downward trend

In the first half of 2025, the central government and supervisory authorities continued to implement the “stabilizing the property market” policy, which mainly focused on removing inventory, expanding demand, new models and risks. The acquisition of existing vacant land and commercial housing stocks was the focus. In terms of chemical risk, the real estate financing coordination mechanism continues to expand and increase efficiency, and do a good job of securing housing delivery. According to data disclosed by the General Financial Supervisory Authority, as of the beginning of May, “white list” loans approved by commercial banks had increased to 6.7 trillion yuan, supporting the construction and delivery of more than 16 million residential units. Continuing to do a good job of securing housing delivery has a positive effect on repairing market sentiment and alleviating residents' concerns about buying homes.

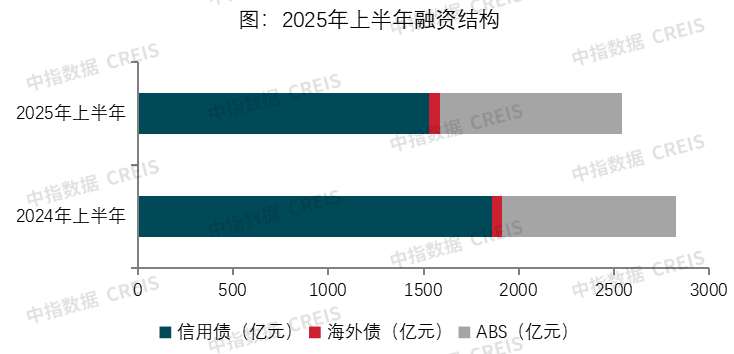

In the first half of 2025, the real estate industry achieved a total of 254.19 billion yuan in bond financing, a year-on-year decrease of 10.0%. Since the second half of 2021, the real estate market has continued to adjust, and the scale of financing has declined sharply. The decline continued in the first half of 2025, and the decline was narrower than the previous year. Overseas bonds have recovered from a low base, but the overall size is still very small. Credit bonds have become the absolute main source of financing. ABS financing accounts for more than one-third, a slight increase over the previous year, and the importance of ABS financing is becoming more and more prominent. Looking at a single month, the total amount of bond financing from March to April exceeded 40 billion yuan; total bond financing declined slightly in May and rebounded in June.

Data source: Middle Index Data CREIS

Judging from the funding available to real estate development companies, the year-on-year decline has narrowed significantly. Among them, the share of domestic loans increased markedly compared to the previous year, boosted by financing policies such as the “white list” of the urban financing coordination mechanism. Deposits, advance accounts, and personal mortgage loans were the main sources of capital, which declined slightly compared to the previous year, and the decline in sales still had an adverse impact on the financial side of housing enterprises. From January to May 2025, real estate development enterprises received 4023.2 billion yuan in capital, a year-on-year decrease of 5.3%, and the decline was 11.7 percentage points narrower than the previous year.

Financing structure: Credit bonds are the main source of financing, and the share of ABS issuance has increased

Data source: Middle Index Data CREIS

Credit bonds: The monthly issuance scale has rebounded since May, and leading central state-owned enterprises are the absolute main issuers

In the first half of 2025, the real estate industry's credit bond issuance scale was 152.66 billion yuan, a year-on-year decrease of 17.9%, accounting for 60.1% of the total financing scale, down 5.8 percentage points from the same period last year. The average distribution period was 3.92 years, of which 58.4% had an issuance period of 3 years or more, an increase of 12.8 percentage points over the previous year, and the period was significantly extended.

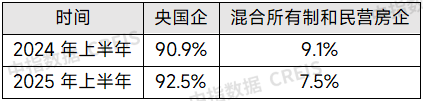

Judging from the issuance structure, the issuers of credit bonds are mainly state-owned enterprises and local state-owned enterprises. In the first half of the year, central state-owned enterprises already accounted for more than 90%, up 1.6 percentage points from the same period last year, and the share of issuance by private enterprises and mixed ownership enterprises declined. There were only 4 private enterprises and mixed ownership enterprises that issued bonds in the first half of 2025, a significant decrease from the previous year. They are all large-scale enterprises that have not yet taken risks.

Table: Share of various types of corporate credit bonds issued in the first half of 2025

Data source: Middle Index Data CREIS

Judging from the share of issuance by leading housing enterprises, the top 10 enterprises in the issuance scale accounted for 48.2% of the financing amount, an increase of 4.1 percentage points over the previous year. Credit bond funds were also concentrated in leading companies. The top 10 companies issuing credit bonds are mainly central state-owned enterprises. Poly Development and China Resources Land issued more than 10 billion dollars, and initial shares, CCCC Real Estate, C&D Real Estate, and Pioneer issued more than 5 billion dollars. The financial advantage of leading companies is not only based on their good credit qualifications, but also related to maintaining resilient sales and strong land acquisition efforts. Judging from credit qualifications, China Resources Land insisted on increasing revenue and expenditure, and strictly adhering to the bottom line of cash flow safety. At the end of 2024, China Resources Land had cash reserves of 133.21 billion yuan, an increase of 16.5% over the previous year. The total interest-bearing debt ratio and net interest-bearing debt ratio remained low in the industry. Overall weighted average financing costs reached a record low. S&P, Moody's and Fitch maintained the company's BBB+, BaA1, and BBB+ industry's best credit ratings. In terms of sales, the share of sales of leading companies continues to rise, and their performance remains strong and resilient. In the first half of 2025, of TOP100 real estate companies' sales, TOP10 companies accounted for 48.7% of sales, an increase of 0.5 percentage points over 2024. TOP20 companies each accounted for 64.8% of sales, an increase of 0.8 percentage points over 2024. Poly Development and China Resources Land both surpassed 100 billion dollars in sales, ranking in the top five in the industry, and the second of the 4 real estate companies with sales exceeding 100 billion dollars in the first half of the year. Judging from the amount of land acquired, leading companies are continuously strengthening their land acquisition efforts, and their share has increased markedly. In the first half of 2025, the TOP10 companies accounted for 55.3% and the TOP20 companies accounted for 69.3%, up 13.9 percentage points and 14.4 percentage points respectively at the end of last year. The share of land acquisition amounts of leading real estate companies increased markedly. Housing companies such as Poly Development, China Resources Land, and C&D Real Estate acquired more than 20 billion dollars, and the land acquisition sales ratio exceeded 30%, indicating that these housing enterprises are relatively strong in acquiring land, and have both the will and ability to invest.

Credit bond issuance channels are shrinking after a long period of market adjustments and corporate insurance. In particular, private housing enterprises have their willingness to finance and their ability to finance have all been suppressed. During the shift between old and new forces in the market, credit bond issuance may continue to maintain an open policy and limited scale. Small and medium-sized private housing enterprises, which are a new force, still need to gradually establish credit debt channels. At the same time, due to their generally small scale of development, these private enterprises adopt a strategy focusing on deep cultivation, and demand for open market financing may not be high. As the main force in the market, all financing channels of central and state-owned enterprises are relatively unobstructed. They have the need to keep various financing channels open, but they will still flexibly match the financing structure according to the characteristics of their own development scale, financing costs, and ease of financing, so as to keep the debt structure healthy and costs manageable.

Overseas bonds: year-on-year growth at a low base, with very few issuers

In the first half of 2025, the amount of overseas bonds issued was only RMB 5.73 billion, up 14.5% year on year, accounting for 2.3% of the total financing scale, up 0.5 percentage points from the same period last year. Overseas bonds were still issued sporadically. In 2025, Greentown and Xincheng successively issued overseas bonds, opening the door to overseas bonds. Judging from the use of capital, the two housing enterprises mainly raise funds to repay overseas bonds that are about to expire and adjust the financing structure. Against the backdrop of continued pressure on the sales side, there are still doubts about whether investor confidence can continue to improve.

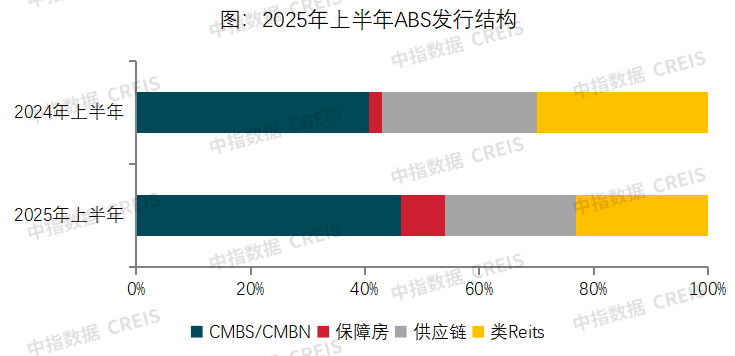

ABS: The share of financing has increased, with CMBS/CMBN and REITs supported by underlying assets accounting for nearly 70%

In the first half of 2025, the financing scale of ABS was 95.80 billion yuan, an increase of 4.8% over the previous year, accounting for 37.7% of the total financing scale, an increase of 5.3 percentage points over the same period last year. The increase in the share of ABS issuance indicates that there is huge room for revitalizing existing assets, and that financing channels are open to companies with high-quality holding assets.

Looking at the distribution structure, CMBS/CMBN is the main distribution type, accounting for 46.3%. The proportion of ABS in REITs and supply chain is 23.0%. The CMBS/CMBN ratio increased rapidly. The share of distribution increased 5.6 percentage points compared to the same period last year, and the share of ABS in the supply chain declined slightly. ABS accounts for less than a quarter of the supply chain, while CMBS/CMBN and REITs account for nearly 70%, indicating that ABS financing based on high-quality underlying assets is favored by investors, which is also conducive to revitalizing existing assets. It should be noted that today, when the commercial real estate market continues to be under pressure, falling vacancy rates and declining rents will still plague stock asset operations, and the excessive decline may cause some ABS to become another type of debt burden.

Data source: Middle Index Data CREIS

In terms of public REITs, the policy focuses on the expansion and expansion of the infrastructure REITs market, and the types of underlying assets are constantly being enriched. Industrial parks and public rental housing REITs continued to expand. Huaxia Jinyu Smart Manufacturing Factory REIT and Huitianfu Shanghai Real Estate Rental Housing REIT were successfully expanded.

In terms of ABS for holding real estate, the Shanghai Stock Exchange and Shenzhen Stock Exchange promoted the accelerated implementation of ABS products for holding real estate in 2025, which is another financial tool to revitalize existing assets. According to public reports, the ABS market for holding real estate in Shanghai is beginning to take shape. Currently, there are 6 products, with a escrow scale of about 12.096 billion yuan, and 14 projects under review; the underlying asset industry covered by ABS for holding real estate is becoming more diverse, and has formed a new situation where multiple highways, guaranteed housing, office buildings, and data centers are progressing.

Financing interest rate: Significant reduction in capital costs

The average interest rate on industry bonds in the first half of 2025 was 2.83%, down 0.28 percentage points from the previous year. Affected by factors such as interest rate cuts this year and changes in financing enterprise structure and channel structure, the average financing cost of industry bonds has declined markedly. Among them, the average interest rate for credit bonds was 2.61%, down 0.44 percentage points from the previous year; the average interest rate for overseas bonds was 9.73%, up 4.14 percentage points from the previous year; and the average interest rate for ABS was 2.77%, down 0.32 percentage points from the previous year.

Table: Average financing interest rates by channel

Data source: Middle Index Data CREIS

Conclusions

The financing policy continued to be relaxed in the first half of 2025, but the scale of bond financing was still declining. The uncertainty and fragmentation of market recovery increased investors' concerns about the real estate industry, and also caused enterprises to take a cautious attitude about new financing. The scale of financing is still shrinking, and the decline has narrowed somewhat.

Looking ahead to the second half of the year, the real estate policy environment is expected to remain relaxed, and various policies already in place are expected to be further implemented, but the fragmentation of the city and project market may continue. Enterprises should also plan cash flow in advance based on sales and land acquisition conditions to prevent capital chain risks. Actively use financing policies such as the project's “white list” mechanism, operating property loans, and supporting housing companies' debt issuance, fixed growth, public REITs, and ABs for holding real estate to expand financing cash inflows through multiple channels, or it may be possible to roll over existing debt and borrow new and old.