- LIVE QUOTES

- LEARN

- HELP

Wall Street Journal

Wall Street JournalEN

EnerSys (ENS): Exploring Valuation After Steady Gains and Renewed Investor Interest

EnerSys (ENS) is back on investors' watchlists after a recent move that, while not tied to any specific news development, has sparked fresh questions about what’s next for the company. Sometimes, it’s these quieter moments that deserve the most attention, especially when the market starts shifting direction without an obvious headline. This situation can reveal as much about sentiment as a splashy announcement.

Over the past year, EnerSys shares have moved steadily higher, gaining 10% and building momentum over the past month with nearly a 9% lift. While there have not been headline-grabbing developments, steady gains and positive trends in both annual revenue and net income growth suggest that investors are reconsidering the company’s long-term potential, perhaps in response to shifting outlooks for the industrial sector. The stock continues to trade above its level from the start of the year and sits well above where it was three years ago, underscoring interest in the company’s execution even in the absence of major news.

With that in mind, is EnerSys trading at a bargain based on its fundamentals, or is the market already factoring in the next phase of growth?

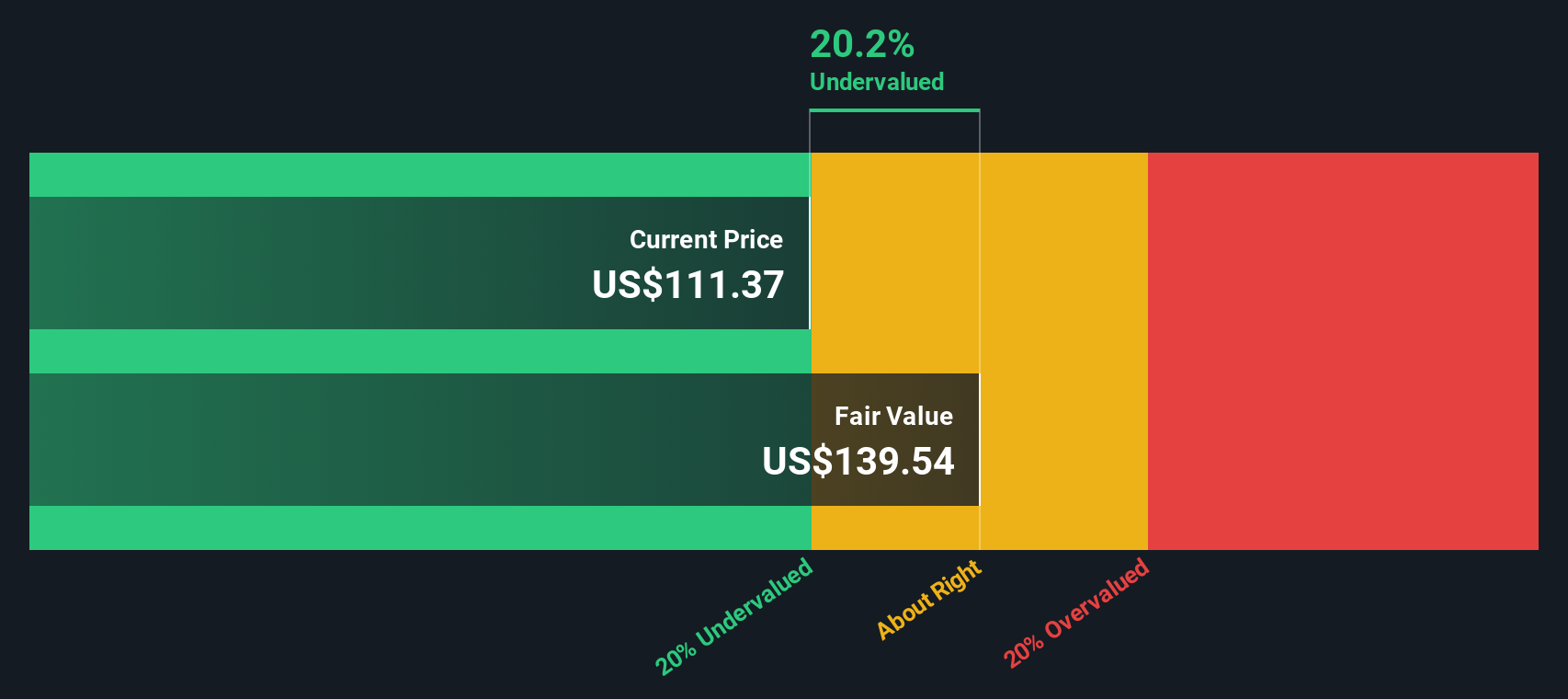

Most Popular Narrative: 12.8% Undervalued

According to the most widely followed narrative, EnerSys is currently trading below its estimated fair value, with room for potential upside based on earnings and margin expansion forecasts.

Major cost-reduction initiatives, including a strategic realignment and transition to Centers of Excellence (CoEs), are expected to generate $80 million in annualized savings starting in fiscal 2026. These measures are projected to structurally expand net and operating margins. The electrification of industrial equipment (for example, forklifts and lift trucks) and automation trends are driving increased demand for maintenance-free batteries and advanced charger solutions. This positions Motive Power for a rebound in volumes and margin expansion as macro and tariff headwinds abate.

Curious about what's fueling that discounted valuation? The growth story hinges on transformative margin improvements and ambitious financial targets that set this forecast apart. What bold projections are analysts betting on, and how do they stack up against industry standards? Explore the full narrative to uncover the crucial numbers shaping this undervalued call.

Result: Fair Value of $120 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, policy uncertainty around tariffs and reliance on acquisitions rather than organic growth could quickly change the outlook if conditions worsen.

Find out about the key risks to this EnerSys narrative.Another View: What Does Our DCF Model Suggest?

Taking a different approach, our SWS DCF model also points toward undervaluation for EnerSys. This echoes the earlier optimism but relies on its own set of assumptions about future cash flows. Could both methods be missing key risks or signals?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own EnerSys Narrative

Whether you see things differently or want to dig deeper into the numbers yourself, you can craft your own take in just a few minutes. Do it your way.

A great starting point for your EnerSys research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investing Opportunities?

Turn market curiosity into action. The Simply Wall Street Screener puts powerful ideas at your fingertips. Now is the moment to find what others might miss.

- Spot tomorrow’s tech giants early by targeting AI penny stocks leading advancements in artificial intelligence and automation for outsized return potential.

- Unlock pockets of value by pursuing undervalued stocks based on cash flows that boast strong financial fundamentals and have been overlooked by the broader market.

- Capture lasting income streams through dividend stocks with yields > 3% designed for stability and reliable payouts above the usual 3% threshold.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com