- LIVE QUOTES

- LEARN

- HELP

Wall Street Journal

Wall Street JournalEN

What Marzetti (MZTI)'s Rising Sales but Lower Profits Could Mean for Long-Term Investors

- The Marzetti Company recently announced fourth quarter results, reporting sales of US$475.43 million, up from US$452.83 million a year earlier, but net income fell to US$32.53 million from US$34.83 million in the previous year.

- This combination of higher sales but slightly lower profits highlights ongoing demand for Marzetti's products, while also signaling cost or margin pressures over the quarter.

- We'll explore how Marzetti's increased revenue alongside reduced earnings per share could impact its longer-term growth investment narrative.

This technology could replace computers: discover 23 stocks that are working to make quantum computing a reality.

Marzetti Investment Narrative Recap

Owning shares in The Marzetti Company often comes down to believing in steady consumer demand for its specialty food brands and its ability to manage margins in a competitive sector. The latest quarter's higher sales but lower net earnings do not significantly impact the biggest short-term catalyst, continued rollout of premium licensed brands, while the most material near-term risk remains cost and margin pressure from rising input and promotional expenses.

From all the recent company updates, the most relevant to these results is the ongoing dividend declaration, as it supports a reliable income stream even when earnings fluctuate. This consistency speaks to management's focus on rewarding shareholders, but does not mitigate uncertainty about margins or underlying demand shifts.

By contrast, investors should be aware that rising promotions and cost pressures could weigh on profitability if trends persist...

Read the full narrative on Marzetti (it's free!)

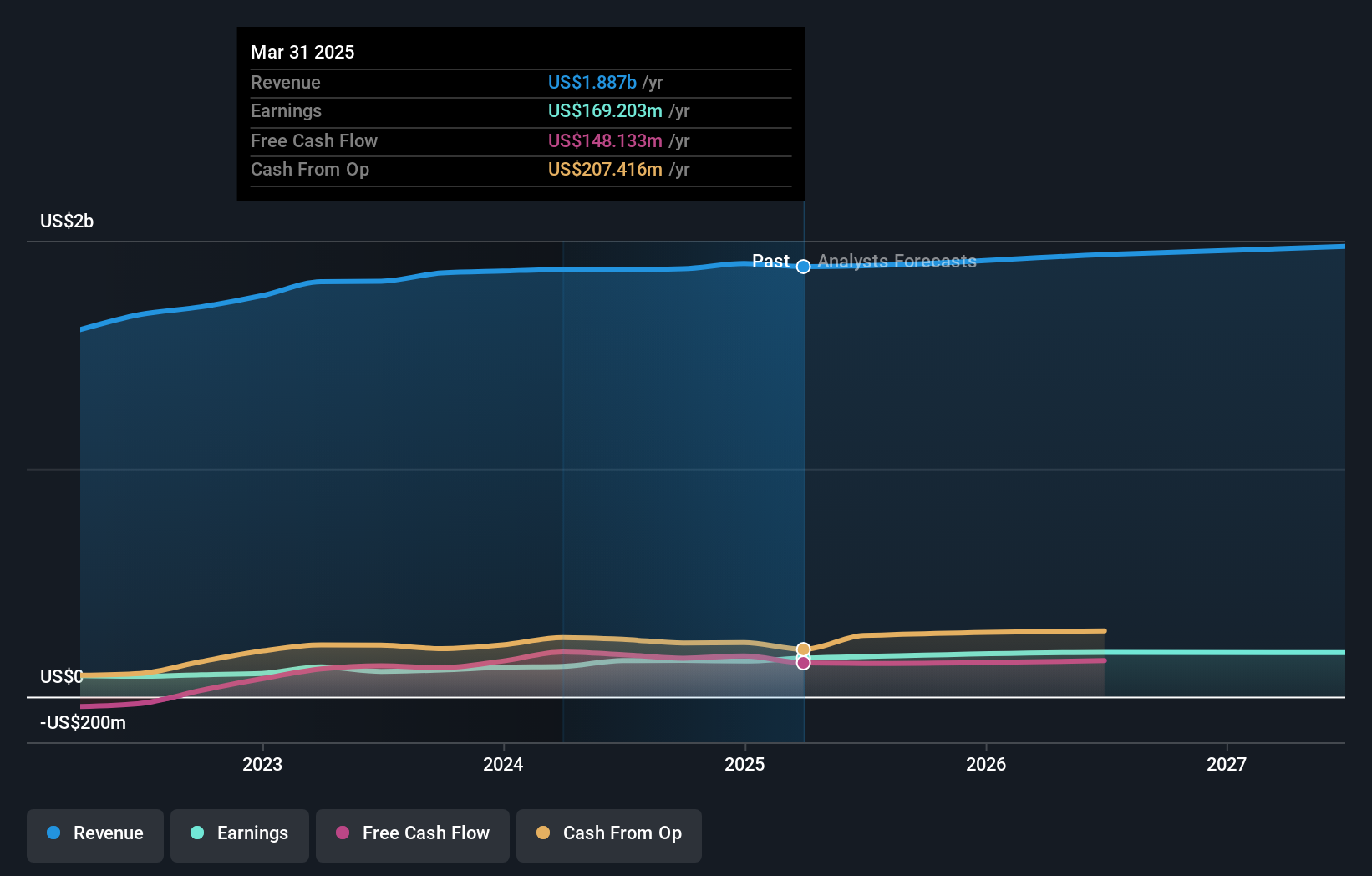

Marzetti's narrative projects $2.0 billion revenue and $208.5 million earnings by 2028. This requires 2.1% yearly revenue growth and a $39.3 million earnings increase from $169.2 million.

Uncover how Marzetti's forecasts yield a $196.33 fair value, a 4% upside to its current price.

Exploring Other Perspectives

Two fair value estimates from the Simply Wall St Community range from US$78.83 to US$139.54 per share prior to the latest results. With many expecting incremental revenue gains from expanding premium brands, opinions vary strongly, explore several viewpoints on Marzetti’s possible performance.

Explore 2 other fair value estimates on Marzetti - why the stock might be worth as much as $139.54!

Build Your Own Marzetti Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Marzetti research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Marzetti research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Marzetti's overall financial health at a glance.

Looking For Alternative Opportunities?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 28 companies in the world exploring or producing it. Find the list for free.

- Outshine the giants: these 20 early-stage AI stocks could fund your retirement.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com