- LIVE QUOTES

- LEARN

- HELP

Wall Street Journal

Wall Street JournalEN

Will United Airlines’ (UAL) JetBlue Partnership and Buyback Shape Its Revenue Trajectory?

- In recent weeks, United Airlines Holdings completed the U.S. Department of Transportation review for its partnership with JetBlue Airways, unlocking new opportunities for collaboration and enhanced customer benefits, while also executing a share buyback of over 3.5 million shares.

- These developments have coincided with increased travel bookings, a rise in airfares, and declining fuel costs, highlighting positive industry trends and potentially improving United Airlines' revenue outlook.

- To assess how these factors impact United Airlines' investment narrative, we'll consider how the new JetBlue partnership and recent demand indicators reinforce prospects for stronger revenue growth.

Explore 24 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

United Airlines Holdings Investment Narrative Recap

To be a shareholder in United Airlines Holdings, one needs to believe in recovering and sustained demand for air travel, alongside the company’s ability to leverage scale, partnerships, and premium offerings to offset industry-wide pressures. The recent Department of Transportation approval for collaboration with JetBlue coincides with increased bookings, higher fares, and lower fuel costs, momentum that could further support the company’s most important near-term catalyst: stronger revenue growth. Yet, operational complexity and exposure to rising costs remain the most immediate risks.

Of all recent developments, the completion of United's share buyback program, repurchasing over 3.5 million shares, stands out as directly tied to this news cycle. Such capital returns may reinforce investor confidence amid positive booking and fare trends, offering additional support to United’s investment case during a period of encouraging demand signals.

However, investors should also be aware that, despite upbeat demand and partnership news, United's exposure to rising operational costs and...

Read the full narrative on United Airlines Holdings (it's free!)

United Airlines Holdings' narrative projects $67.6 billion revenue and $4.2 billion earnings by 2028. This requires 5.2% yearly revenue growth and a $0.9 billion earnings increase from $3.3 billion.

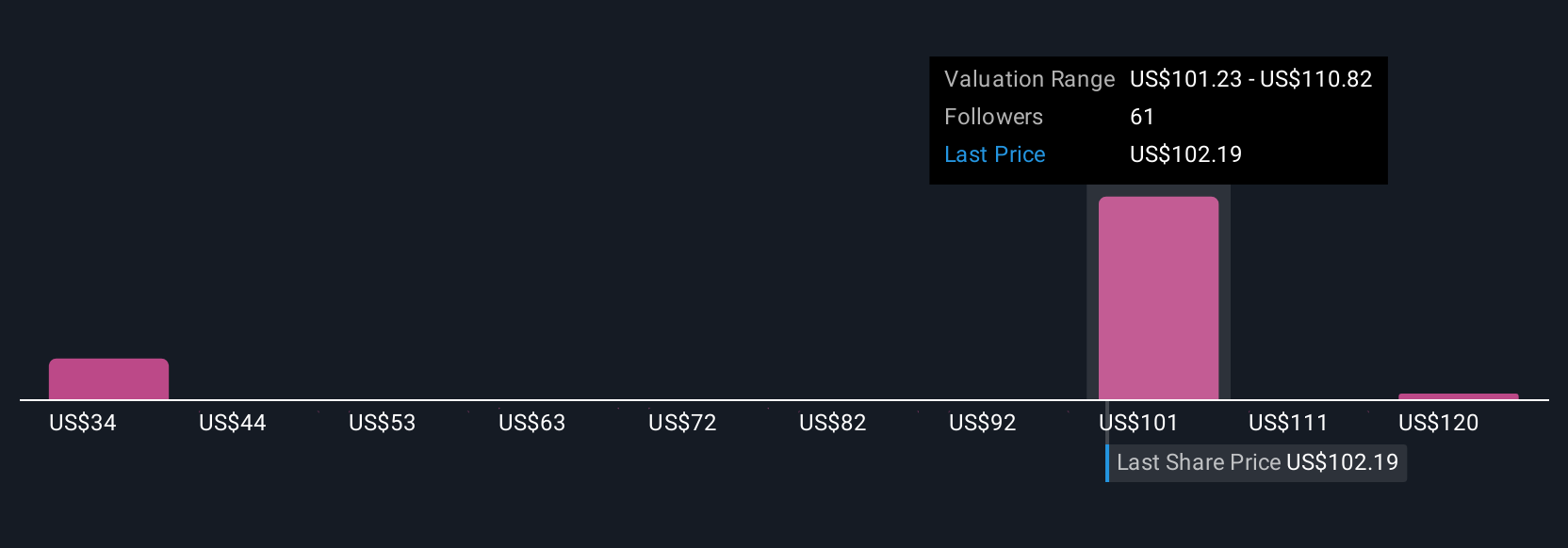

Uncover how United Airlines Holdings' forecasts yield a $107.55 fair value, a 7% upside to its current price.

Exploring Other Perspectives

Seven fair value estimates from the Simply Wall St Community range from US$33.90 to US$130, reflecting highly varied market outlooks. While some see substantial upside, persistent risks around United’s reliance on debt-funded growth could affect future performance and are worth reading more about.

Explore 7 other fair value estimates on United Airlines Holdings - why the stock might be worth as much as 29% more than the current price!

Build Your Own United Airlines Holdings Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your United Airlines Holdings research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free United Airlines Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate United Airlines Holdings' overall financial health at a glance.

Contemplating Other Strategies?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- AI is about to change healthcare. These 27 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com