- LIVE QUOTES

- LEARN

- HELP

Wall Street Journal

Wall Street JournalEN

Is Omnicom’s Strong Q2 Earnings and Institutional Buying Reshaping the OMC Investment Case?

- In August 2025, Omnicom Group Inc. announced a fixed-income exchange offer involving several corporate bond notes and also presented at the Morgan Stanley Media & Communications Corporate Access Day in New York.

- Institutional investor HOTCHKIS & WILEY made a very large increase in their Omnicom holdings during Q2 2025, reflecting renewed confidence following Omnicom’s strong second-quarter earnings that surpassed expectations and drove analyst estimate revisions.

- We’ll examine how Omnicom’s impressive quarterly performance and institutional buying may influence its expected earnings trajectory and sector positioning.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Omnicom Group Investment Narrative Recap

To own Omnicom Group, an investor must believe in the company's ability to deliver integrated, data-rich marketing solutions at a global scale, especially as it integrates Interpublic and seeks digital leadership. While the recently announced fixed-income exchange offer and institutional buying reflect underlying confidence, these moves are unlikely to materially change the biggest short-term catalyst, the Interpublic merger integration, or address the most pressing risk, which is the rising threat from AI-driven client insourcing and digital ad platforms.

The most relevant recent announcement is Omnicom’s August 2025 fixed-income exchange offer, which is directly tied to financing its Interpublic acquisition. This action highlights management’s clear focus on funding and executing the merger, a process expected to shape Omnicom’s competitive position and near-term growth prospects, while putting a spotlight on execution and integration risks that could impact outcomes.

On the other hand, investors should pay close attention to the rapid adoption of AI content creation and digital ad tools, since...

Read the full narrative on Omnicom Group (it's free!)

Omnicom Group's outlook projects $17.3 billion in revenue and $1.7 billion in earnings by 2028. This reflects 2.8% annual revenue growth and a $0.3 billion increase in earnings from $1.4 billion today.

Uncover how Omnicom Group's forecasts yield a $96.33 fair value, a 26% upside to its current price.

Exploring Other Perspectives

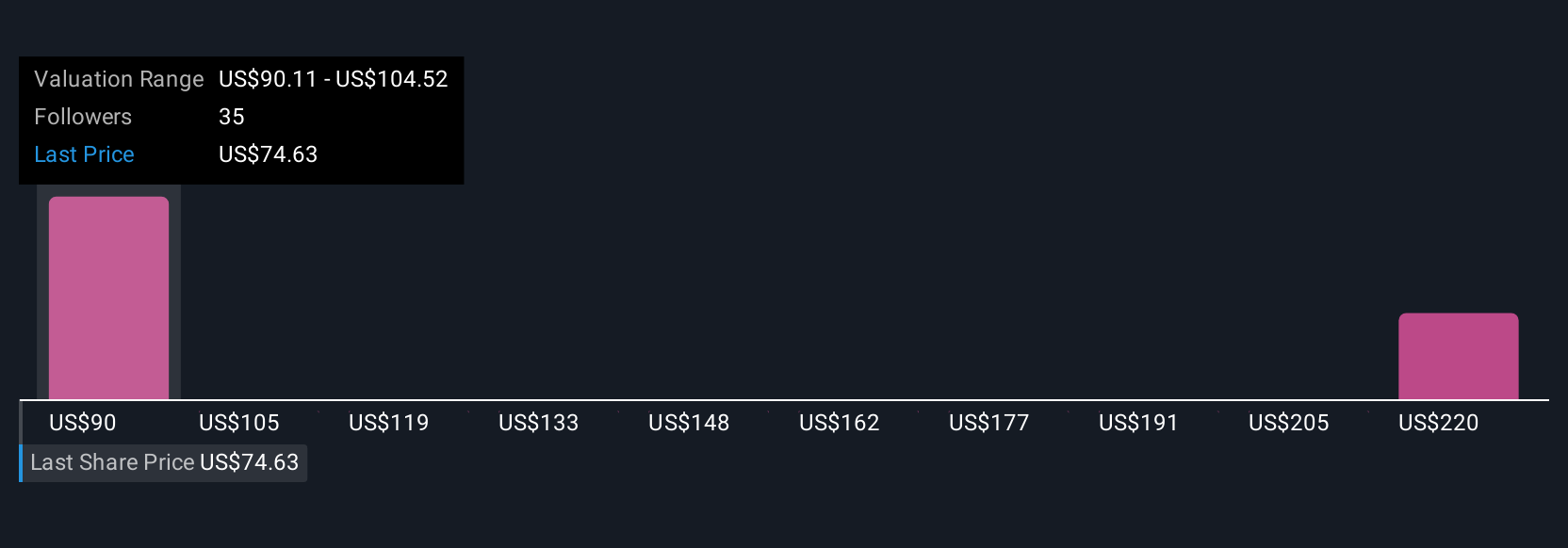

Four members of the Simply Wall St Community estimate fair value for Omnicom from US$78 to US$225.81 per share. While investors debate valuation, the merger with Interpublic stands as a pivotal catalyst that could reshape Omnicom’s future earnings capacity, highlighting the importance of considering a range of viewpoints before making any decisions.

Explore 4 other fair value estimates on Omnicom Group - why the stock might be worth just $78.00!

Build Your Own Omnicom Group Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Omnicom Group research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Omnicom Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Omnicom Group's overall financial health at a glance.

Looking For Alternative Opportunities?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Find companies with promising cash flow potential yet trading below their fair value.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 28 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com