- LIVE QUOTES

- LEARN

- HELP

Wall Street Journal

Wall Street JournalEN

Accelerating Buybacks and Strong Earnings Might Change the Case for Investing in JLL

- Jones Lang LaSalle (JLL) recently reported strong second-quarter results, including year-over-year sales and net income gains, and updated investors on completing the repurchase of 12.7% of its shares since 2019 for US$1.25 billion.

- Management highlighted an intention to further accelerate share buybacks and pursue selective acquisitions, while maintaining a high threshold for potential M&A in the context of current share valuations.

- We’ll examine how the combination of accelerating share buybacks and robust financial results could influence JLL’s investment narrative.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Jones Lang LaSalle Investment Narrative Recap

To be a JLL shareholder, you need to believe in the company’s ability to drive recurring revenue growth from workplace and project management contracts while capturing value from cyclical market recoveries in capital markets and leasing. The Q2 results and increased share buybacks reinforce confidence in management’s disciplined capital allocation, but do not fundamentally shift short-term catalysts or mitigate the main risk of subdued leasing activity and revenue exposure to challenging transactional markets.

One of the most relevant recent announcements is management’s commitment to accelerate share repurchases through the second half of 2025, alongside their high standards for potential acquisitions. This move, combined with robust financial performance, spotlights JLL’s focus on shareholder returns, though conditions in office leasing and capital markets remain key drivers for future performance. Despite recent momentum, investors should also be mindful that recurring loan losses tied to operational or credit events in the Fannie Mae fee loan portfolio can still add unexpected expense pressures...

Read the full narrative on Jones Lang LaSalle (it's free!)

Jones Lang LaSalle's narrative projects $27.7 billion revenue and $1.0 billion earnings by 2028. This requires 3.9% yearly revenue growth and a $436 million earnings increase from $563.9 million today.

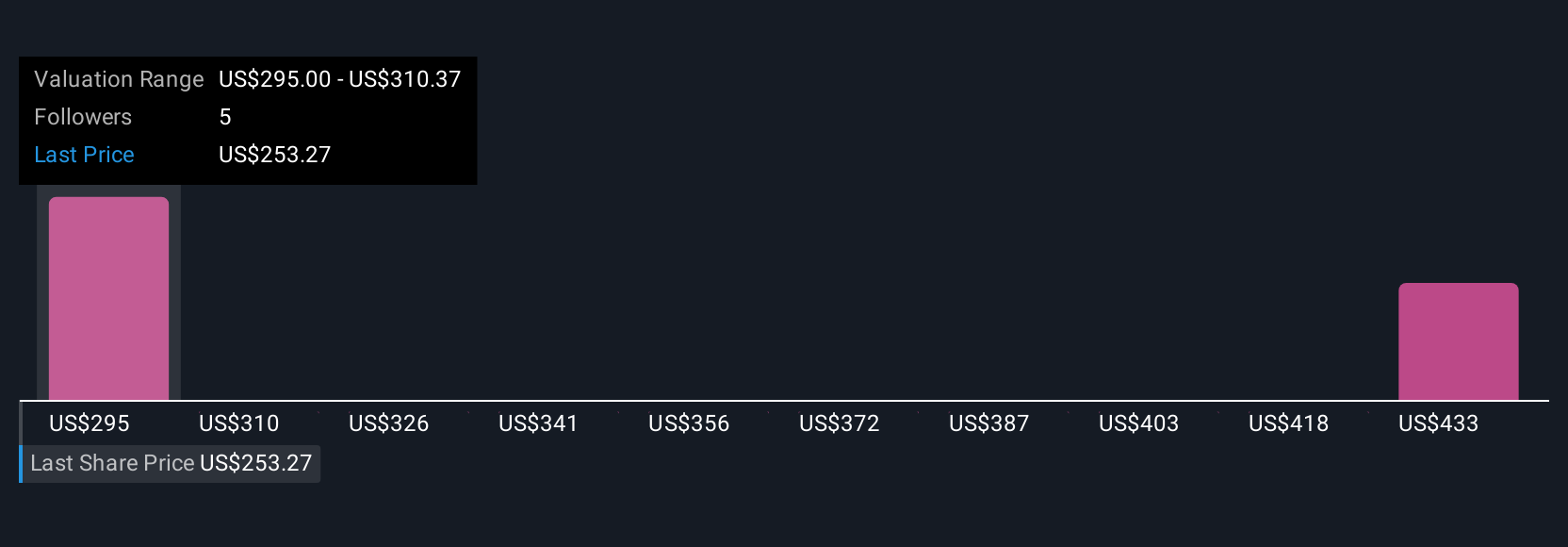

Uncover how Jones Lang LaSalle's forecasts yield a $306.56 fair value, a 10% upside to its current price.

Exploring Other Perspectives

Two community members from Simply Wall St estimate JLL’s fair value between US$306.56 and US$416.90 per share. While some see strong recurring revenue growth as a key strength, viewpoints differ widely so be sure to review alternative assessments before making any investment decisions.

Explore 2 other fair value estimates on Jones Lang LaSalle - why the stock might be worth as much as 50% more than the current price!

Build Your Own Jones Lang LaSalle Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Jones Lang LaSalle research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Jones Lang LaSalle research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Jones Lang LaSalle's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 20 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com