- LIVE QUOTES

- LEARN

- HELP

Wall Street Journal

Wall Street JournalEN

Does Chemed's (CHE) Dividend Hike Signal Steadfast Confidence Amid VITAS Transition and Lower Guidance?

- Chemed Corporation recently announced lower quarterly earnings, revised its annual earnings guidance downward, and shared that the CEO of its key subsidiary, VITAS Healthcare, will depart later this year.

- These announcements were accompanied by a 20% dividend increase and a US$300 million boost to Chemed's share buyback authorization, highlighting the company's efforts to return capital to shareholders amid operational headwinds.

- To assess Chemed's investment outlook, we'll explore how the reduced guidance and VITAS leadership transition may reshape future prospects.

Find companies with promising cash flow potential yet trading below their fair value.

Chemed Investment Narrative Recap

Chemed shareholders need confidence in the company’s ability to expand VITAS's hospice footprint while restoring margins and addressing ongoing Medicare reimbursement risks. The recent downward earnings revision and planned VITAS leadership change are important, but the biggest catalyst, scaling new service locations, remains the key to near-term sentiment. While the CEO transition could affect continuity, the impact on this primary growth lever does not appear material at present.

Among the latest announcements, the 20% increase in Chemed’s quarterly dividend stands out. This move signals a commitment to returning capital to shareholders even as short-term earnings guidance is reduced, offering some reassurance for those focused on income and cash flow stability. However, for investors, the most pressing issue remains the sustainability of VITAS’s margins given ongoing reimbursement pressures and patient mix adjustments...

Read the full narrative on Chemed (it's free!)

Chemed's narrative projects $2.9 billion revenue and $347.9 million earnings by 2028. This requires 5.0% yearly revenue growth and a $57.6 million earnings increase from $290.3 million.

Uncover how Chemed's forecasts yield a $567.25 fair value, a 30% upside to its current price.

Exploring Other Perspectives

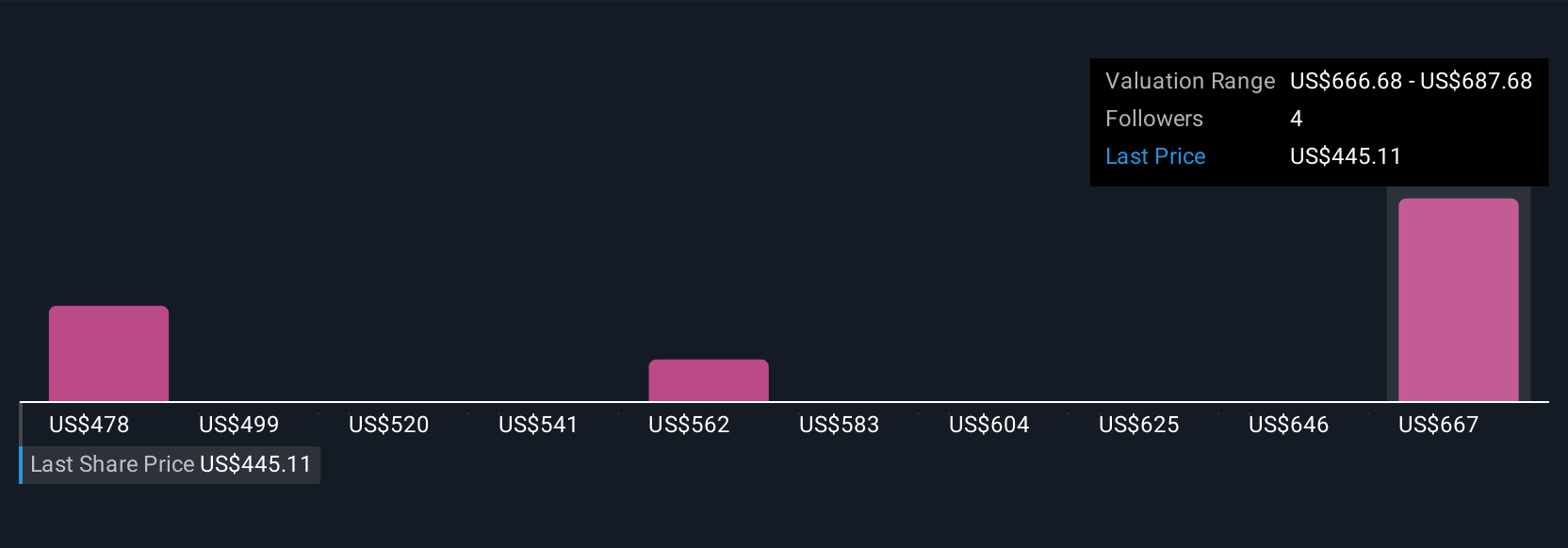

Four fair value estimates from the Simply Wall St Community range between US$477.66 and US$687.68 per share. With reimbursement risk still critical for VITAS, you can explore several alternative viewpoints on Chemed’s future earnings power and market position.

Explore 4 other fair value estimates on Chemed - why the stock might be worth as much as 58% more than the current price!

Build Your Own Chemed Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Chemed research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Chemed research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Chemed's overall financial health at a glance.

Searching For A Fresh Perspective?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- We've found 21 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com