- LIVE QUOTES

- LEARN

- HELP

Wall Street Journal

Wall Street JournalEN

Did Earnings Growth and Completed Buyback Just Shift Universal Health Services' (UHS) Investment Narrative?

- Universal Health Services recently reported strong second-quarter 2025 results, with revenue rising to US$4.28 billion and net income reaching US$353.22 million, alongside raising its full-year net revenue guidance and completing a sizeable share buyback program initiated in 2014.

- This combination of earnings growth, higher guidance, and substantial share repurchases highlights management’s focus on both operational improvement and returning capital to shareholders.

- We’ll examine how the company’s updated earnings guidance and buyback completion might shift its long-term growth assumptions and risk outlook.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 19 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Universal Health Services Investment Narrative Recap

To be a shareholder in Universal Health Services, one generally needs to believe that continued demand for acute and behavioral health services can overcome industry risks like regulatory changes and labor cost pressures. The recent combination of higher second-quarter earnings, a raised revenue outlook, and the completion of a substantial share buyback may improve confidence near term, but do not materially shift the biggest catalyst, outpatient behavioral health growth, or the foremost risk, potential changes to government reimbursement.

Among the latest announcements, the earnings report stands out. UHS delivered robust year-over-year increases in both revenue and net income, pointing to improved operational execution. These results align with ongoing catalysts in outpatient behavioral care and technology, but investors will likely remain focused on whether margin expansion can offset regulatory hurdles expected over the coming years.

Yet, despite these positive signals, investors should be aware that if Medicaid supplemental payments are reduced in coming years…

Read the full narrative on Universal Health Services (it's free!)

Universal Health Services is projected to reach $19.0 billion in revenue and $1.4 billion in earnings by 2028. This outlook assumes a 4.9% annual revenue growth rate and a $0.1 billion increase in earnings from $1.3 billion today.

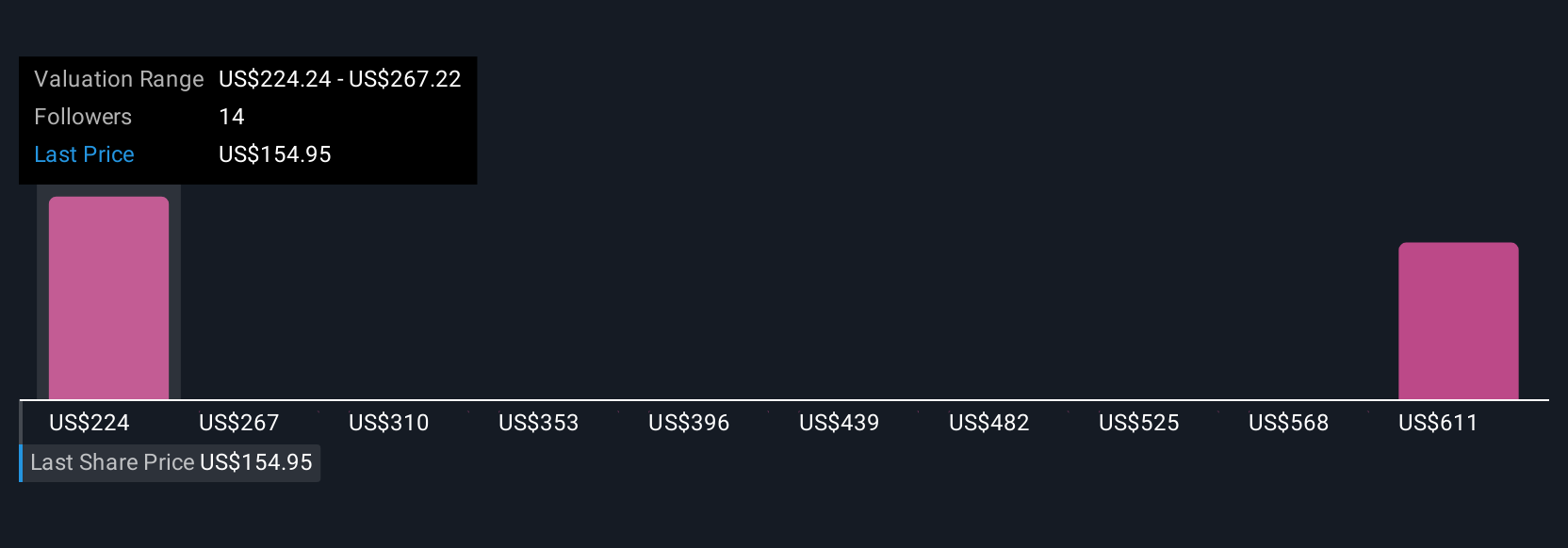

Uncover how Universal Health Services' forecasts yield a $221.75 fair value, a 35% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community fair value estimates for UHS, based on three contributors, range widely from US$221.75 to US$703.64. While profit growth trends have recently accelerated, the lasting impact of regulatory and reimbursement changes remains a central question for anyone assessing the company’s future performance.

Explore 3 other fair value estimates on Universal Health Services - why the stock might be worth just $221.75!

Build Your Own Universal Health Services Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Universal Health Services research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Universal Health Services research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Universal Health Services' overall financial health at a glance.

Looking For Alternative Opportunities?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- The end of cancer? These 25 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Find companies with promising cash flow potential yet trading below their fair value.

- AI is about to change healthcare. These 26 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com