- LIVE QUOTES

- LEARN

- HELP

Wall Street Journal

Wall Street JournalEN

Undiscovered Gems In The US Market August 2025

As the U.S. market rebounds from a recent sell-off, with major indices like the Dow Jones and S&P 500 showing signs of recovery, investors are keenly watching small-cap stocks for potential opportunities amid fluctuating economic indicators. In this dynamic environment, identifying promising stocks often involves looking beyond immediate market trends to uncover companies with strong fundamentals and growth potential that may not yet be widely recognized by the broader investment community.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Sound Financial Bancorp | 34.70% | 2.11% | -11.08% | ★★★★★★ |

| Metalpha Technology Holding | NA | 75.66% | 28.60% | ★★★★★★ |

| FineMark Holdings | 115.14% | 2.22% | -28.34% | ★★★★★★ |

| Preformed Line Products | 7.86% | 6.57% | 8.22% | ★★★★★★ |

| Valhi | 43.01% | 1.55% | -2.64% | ★★★★★☆ |

| Pure Cycle | 5.02% | 4.35% | -2.25% | ★★★★★☆ |

| Gulf Island Fabrication | 19.65% | -2.17% | 42.26% | ★★★★★☆ |

| Rich Sparkle Holdings | 26.73% | -6.13% | 1.75% | ★★★★★☆ |

| Solesence | 91.26% | 23.30% | 4.70% | ★★★★☆☆ |

| Reitar Logtech Holdings | 31.39% | 231.46% | 41.38% | ★★★★☆☆ |

Let's dive into some prime choices out of from the screener.

Legacy Housing (LEGH)

Simply Wall St Value Rating: ★★★★★★

Overview: Legacy Housing Corporation focuses on the construction, sale, and financing of manufactured homes and tiny houses mainly in the southern United States, with a market capitalization of approximately $548.68 million.

Operations: Legacy Housing generates revenue primarily from the manufactured buildings segment, with $176.62 million in sales. The company focuses on the construction and sale of these homes while also offering financing options to customers.

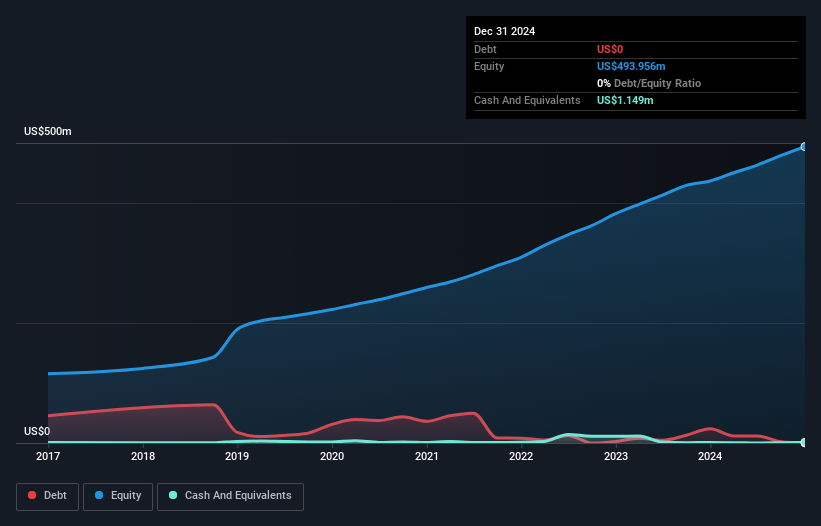

Legacy Housing, a player in the manufactured homes sector, is capitalizing on growth opportunities by expanding production in Texas and Georgia. Despite a dip in first-quarter revenue to US$35.67 million from US$43.24 million last year, the company remains debt-free with high-quality earnings and has repurchased 262,530 shares for US$5.39 million since November 2022. Analysts anticipate profit margins to rise slightly from 32.1% to 32.9%, projecting modest annual revenue growth of 3.3%. However, challenges such as declining sales and market uncertainties could impact future stability despite a consensus price target of US$30.33 per share.

Safety Insurance Group (SAFT)

Simply Wall St Value Rating: ★★★★★☆

Overview: Safety Insurance Group, Inc. offers private passenger and commercial automobile, as well as homeowner insurance in the United States, with a market capitalization of approximately $1.03 billion.

Operations: The primary revenue stream for Safety Insurance Group comes from its Property and Casualty Insurance Operations, generating approximately $1.15 billion.

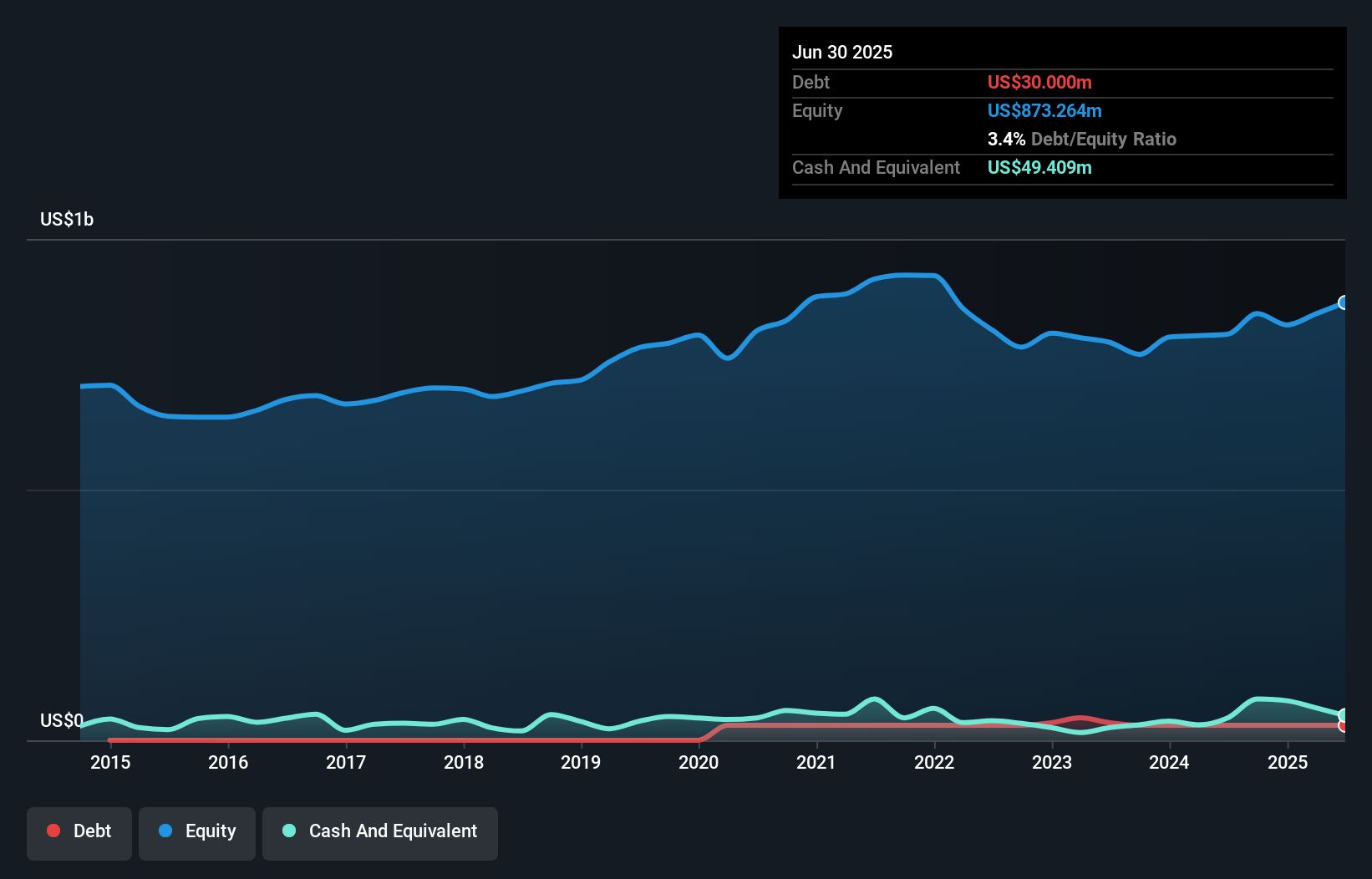

Safety Insurance Group, a notable player in the insurance sector, showcases solid financial health with high-quality earnings and an impressive EBIT coverage of 189.8x for its interest payments. Its price-to-earnings ratio stands attractively at 14.3x, below the broader US market average of 18x, signaling potential value. Over the past year, earnings growth surged by 41.3%, outpacing the industry’s average of 8.7%. Despite a historical decline in earnings by 21.7% annually over five years, recent performance shows promise with net income rising to US$21.9 million from US$20.08 million year-on-year and dividends maintained at $0.90 per share.

- Unlock comprehensive insights into our analysis of Safety Insurance Group stock in this health report.

Explore historical data to track Safety Insurance Group's performance over time in our Past section.

National Presto Industries (NPK)

Simply Wall St Value Rating: ★★★★★★

Overview: National Presto Industries, Inc. operates in North America offering housewares and small appliances, defense, and safety products with a market capitalization of approximately $681.56 million.

Operations: NPK generates revenue primarily from its defense segment at $309.92 million, followed by housewares and small appliances at $103.46 million, and safety products contributing $1.83 million. The company's net profit margin is a key indicator to consider when evaluating financial performance.

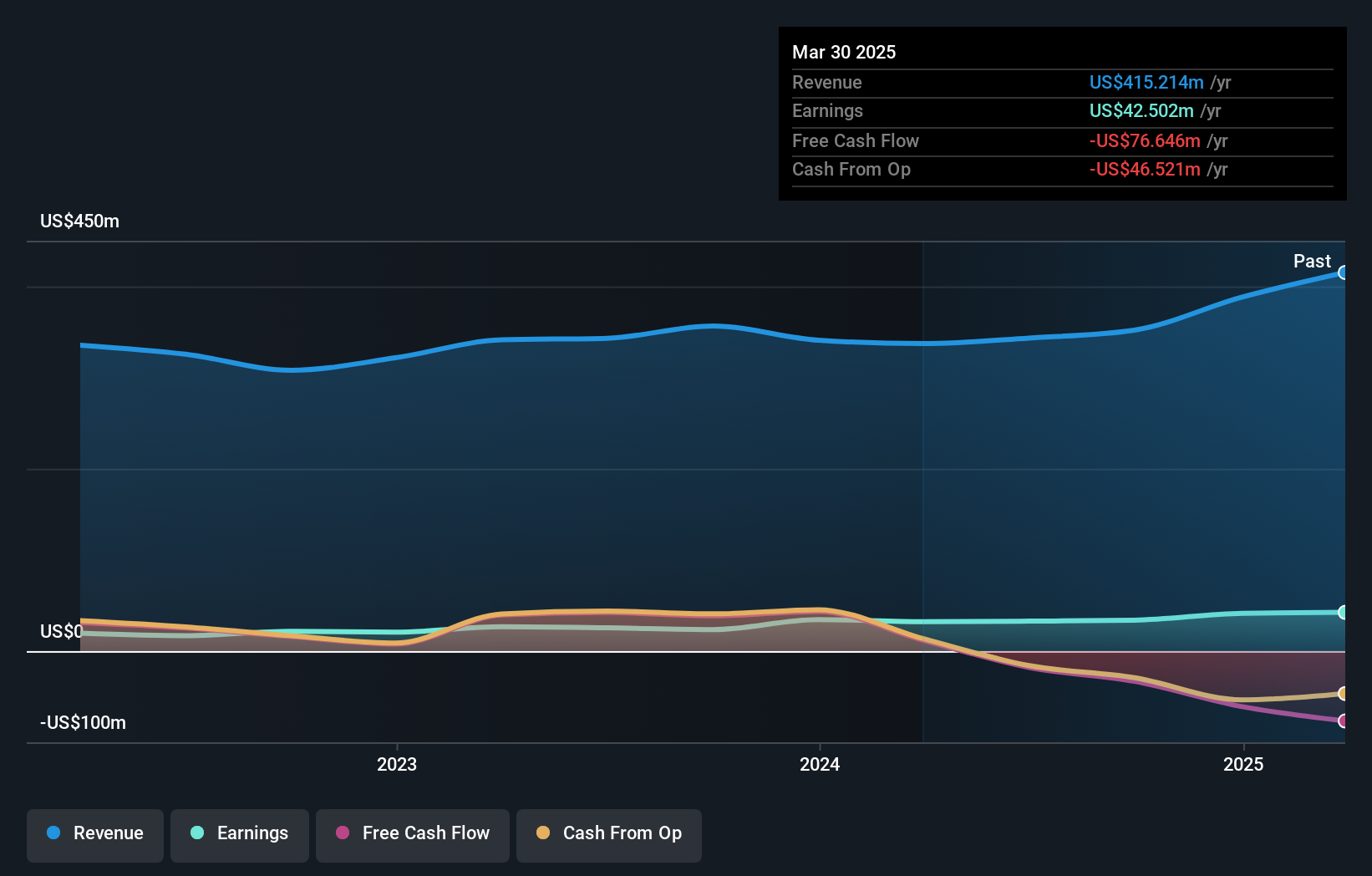

National Presto Industries, a nimble player in the Aerospace & Defense sector, has shown impressive earnings growth of 31.7% over the past year, outpacing the industry's 14.9%. With a price-to-earnings ratio of 16x, it offers better value compared to the US market average of 18x. Despite a challenging five-year period with earnings dropping by an average of 6.4% annually, NPK remains debt-free for five years and boasts high-quality non-cash earnings. Recent first-quarter results revealed sales soaring to US$103.64 million from last year's US$76.65 million and net income rising to US$7.61 million from US$6.57 million, reflecting robust operational performance amidst industry challenges.

Seize The Opportunity

- Unlock more gems! Our US Undiscovered Gems With Strong Fundamentals screener has unearthed 290 more companies for you to explore.Click here to unveil our expertly curated list of 293 US Undiscovered Gems With Strong Fundamentals.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com