- LIVE QUOTES

- LEARN

- HELP

Wall Street Journal

Wall Street JournalEN

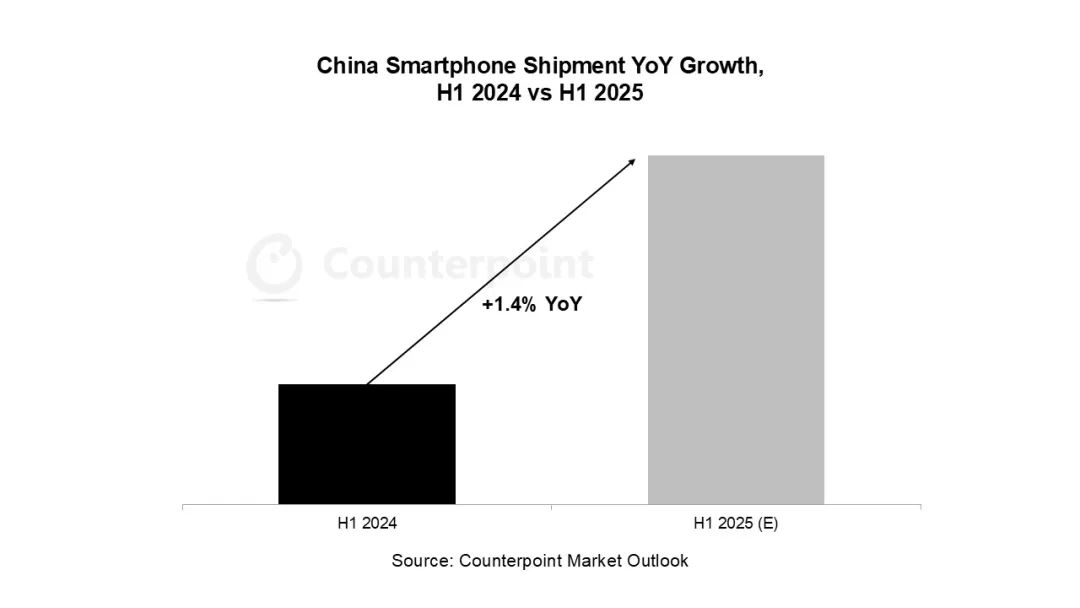

Counterpoint Research: China's smartphone market shipments are expected to increase 1.4% year-on-year in the first half of 2025

The Zhitong Finance App learned that according to Counterpoint Research's quarterly observation report on the Chinese smartphone market, shipments in the Chinese smartphone market are expected to increase by 1.4% year-on-year in the first half of 2025, becoming a stabilizer against the backdrop of increased overall uncertainty in the global market. State subsidies stimulated early demand, but the market faced implementation problems. The pace of subsidy disbursement has recently slowed, but the project is expected to continue throughout 2025, and possibly until 2026. With the iPhone Pro price reduction and inclusion in the subsidy list, Apple performed best during the 618 period. Xiaomi released its self-developed application processor AP-XRing O1, strengthening its high-end market layout. AI is still the core theme, but manufacturers place more emphasis on implementing practical scenarios.

The implementation of the national smartphone subsidy program has been blocked, but it is expected to continue until the second half of 2025

China's central government has launched a subsidy program of about 300 billion yuan (about 41.4 billion US dollars) to stimulate the purchase of consumer electronics products, including smartphones under 6,000 yuan (about 828 US dollars).

The first round of funding significantly boosted sales growth in Q1, but it also revealed a series of difficulties in implementation.

The complicated subsidy process discourages small and medium-sized manufacturers, while large retail channels with sufficient resources are easier to implement, so Huawei and Xiaomi benefit the most from this policy.

Despite challenges on the executive side and the recent slowdown in the pace of subsidy disbursement, the project is expected to continue throughout 2025, and possibly until 2026 (based on supply chain channel research). However, as China's smartphone market matures, the marginal effects of such large-scale incentive policies are gradually weakening.

Apple dominates the 618 promotion with drastic price cuts

In the 2025 “618” promotion season (week 22: May 26 to June 1 to week 25: June 16-22), Apple achieved 8% year-on-year growth by drastically lowering the price of the iPhone 16 series, and regained the top sales list.

This price reduction made the iPhone 16 Pro meet national smartphone subsidy standards, making it the strongest official price reduction in the iPhone Pro series in recent years.

After the subsidy, the price of the iPhone 16 Pro 128GB model was more than 30% lower than the launch price.

Xiaomi releases self-developed application processor (AP)

It took nearly four years and invested more than 1.8 billion US dollars to launch the first self-developed AP, the XRing O1, and was the first to be installed in the Xiaomi 15S Pro and tablet product line.

According to industry channel information, about one-third of the Xring O1 will be used for the 15S Pro, and the rest will be for tablet products. The next generation of Xring chips is already under development, and shipments are expected to double that of O1.

Xiaomi's growth in the smartphone market continues to increase, and its vehicle building (EV) business has also enhanced its overall brand image.

As China's high-end mobile phone consumers gradually become younger, the strong links between Xiaomi and young people may help it further increase its share in the high-end market.

The popularity of AI continues unabated, and manufacturers are turning to a “pragmatic” route

AI is still a hot topic in China, but smartphone makers are becoming more strategically pragmatic. From 2023 to 2024, almost all mainstream manufacturers integrated AI as a flagship highlight.

According to Counterpoint's generative AI consumer research in the first half of 2025, 76% of Chinese smartphone users say they are “familiar,” “very familiar,” or “extremely familiar” with AI.

However, in 2025, manufacturers reduced high-profile promotion of “end-side AI” in new product launches, and realized that AI labels alone were not enough to drive consumer interest.

AI is still at the core of the strategies of major manufacturers, but the focus has shifted to the implementation of “real usage scenarios.” For example, OPPO has introduced the “Small Cloth Memory” function, which allows users to take notes through multimedia to improve memory and usage stickiness.

The addition of internet giants has intensified competition. Tencent announced during the earnings conference call that it will connect AI agents to the WeChat ecosystem, covering services such as payment, taxis, and takeout. Some internet companies have even begun exploring the viability of launching their own phones.

The rise of AI is prompting the industry to rethink how devices can become the core touchpoint for users.

The overall supply chain is stable, but pressure intensified in the second half of the year

Based on our interviews with supply chains and manufacturers, we found that with the exception of memory, the prices of most core components showed a downward trend in the first half of 2025 compared to the fourth quarter of 2024. But memory (especially DRAM) is an exception, and prices are rising.

We expect smartphone manufacturers to face greater cost pressure in the second half of 2025, especially in the middle and low end product lines. Drivers include the release of new components, the continued rise in memory prices, and the temporary shift of some manufacturing to China due to tight global rare earth supply in the second quarter.

China's smartphone shipments are expected to increase by less than 1% year-on-year throughout 2025. The state subsidy policy remains a key supporting force, although economic headwinds persist. The high-end market is expected to continue to be the highlight of the world's largest smartphone market.