- LIVE QUOTES

- LEARN

- HELP

Wall Street Journal

Wall Street JournalEN

Getting In Cheap On NationGate Holdings Berhad (KLSE:NATGATE) Is Unlikely

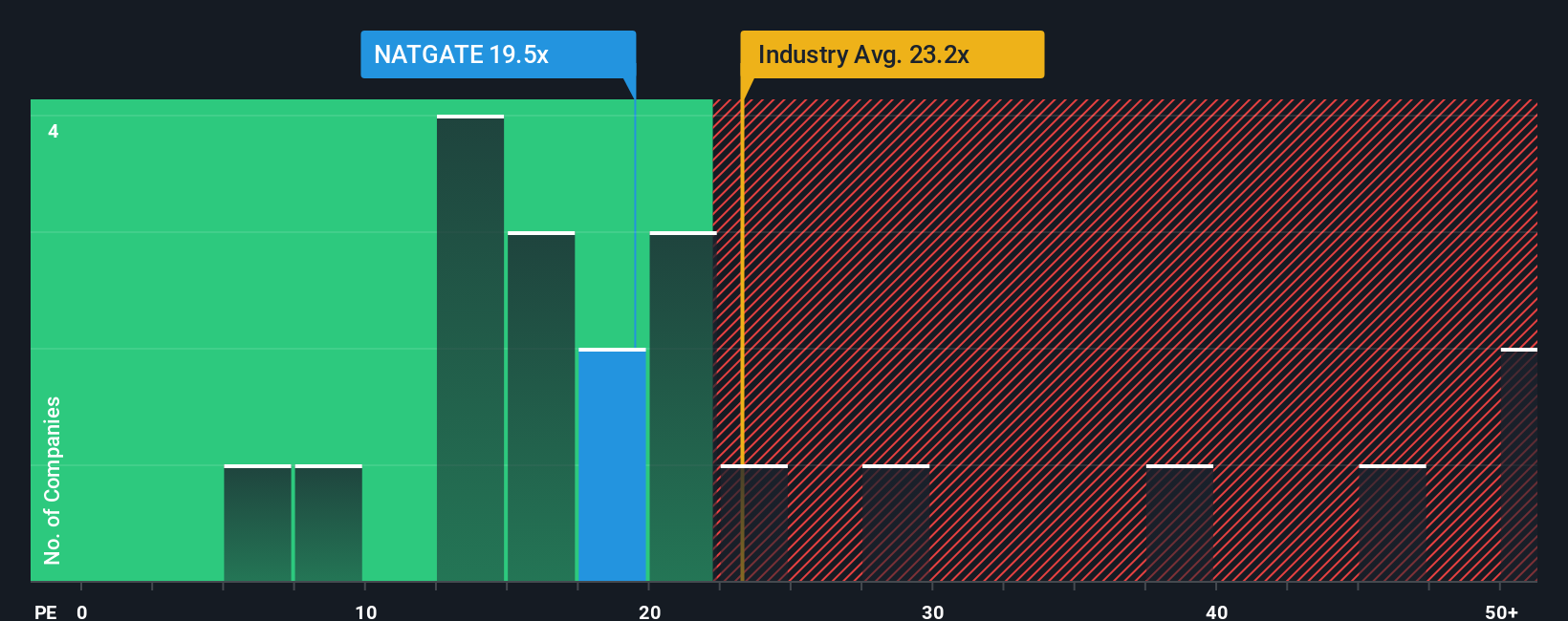

NationGate Holdings Berhad's (KLSE:NATGATE) price-to-earnings (or "P/E") ratio of 19.5x might make it look like a sell right now compared to the market in Malaysia, where around half of the companies have P/E ratios below 13x and even P/E's below 8x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/E.

Recent times have been advantageous for NationGate Holdings Berhad as its earnings have been rising faster than most other companies. The P/E is probably high because investors think this strong earnings performance will continue. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

View our latest analysis for NationGate Holdings Berhad

What Are Growth Metrics Telling Us About The High P/E?

The only time you'd be truly comfortable seeing a P/E as high as NationGate Holdings Berhad's is when the company's growth is on track to outshine the market.

Retrospectively, the last year delivered an exceptional 163% gain to the company's bottom line. Despite this strong recent growth, it's still struggling to catch up as its three-year EPS frustratingly shrank by 99% overall. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Turning to the outlook, the next three years should generate growth of 5.4% per annum as estimated by the five analysts watching the company. That's shaping up to be materially lower than the 12% per annum growth forecast for the broader market.

In light of this, it's alarming that NationGate Holdings Berhad's P/E sits above the majority of other companies. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. There's a good chance these shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with the growth outlook.

The Bottom Line On NationGate Holdings Berhad's P/E

Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

Our examination of NationGate Holdings Berhad's analyst forecasts revealed that its inferior earnings outlook isn't impacting its high P/E anywhere near as much as we would have predicted. When we see a weak earnings outlook with slower than market growth, we suspect the share price is at risk of declining, sending the high P/E lower. Unless these conditions improve markedly, it's very challenging to accept these prices as being reasonable.

It is also worth noting that we have found 3 warning signs for NationGate Holdings Berhad (1 is a bit unpleasant!) that you need to take into consideration.

You might be able to find a better investment than NationGate Holdings Berhad. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.