- LIVE QUOTES

- LEARN

- HELP

Wall Street Journal

Wall Street JournalEN

Orient Cement Limited (NSE:ORIENTCEM) Shares Slammed 29% But Getting In Cheap Might Be Difficult Regardless

The Orient Cement Limited (NSE:ORIENTCEM) share price has fared very poorly over the last month, falling by a substantial 29%. Indeed, the recent drop has reduced its annual gain to a relatively sedate 7.1% over the last twelve months.

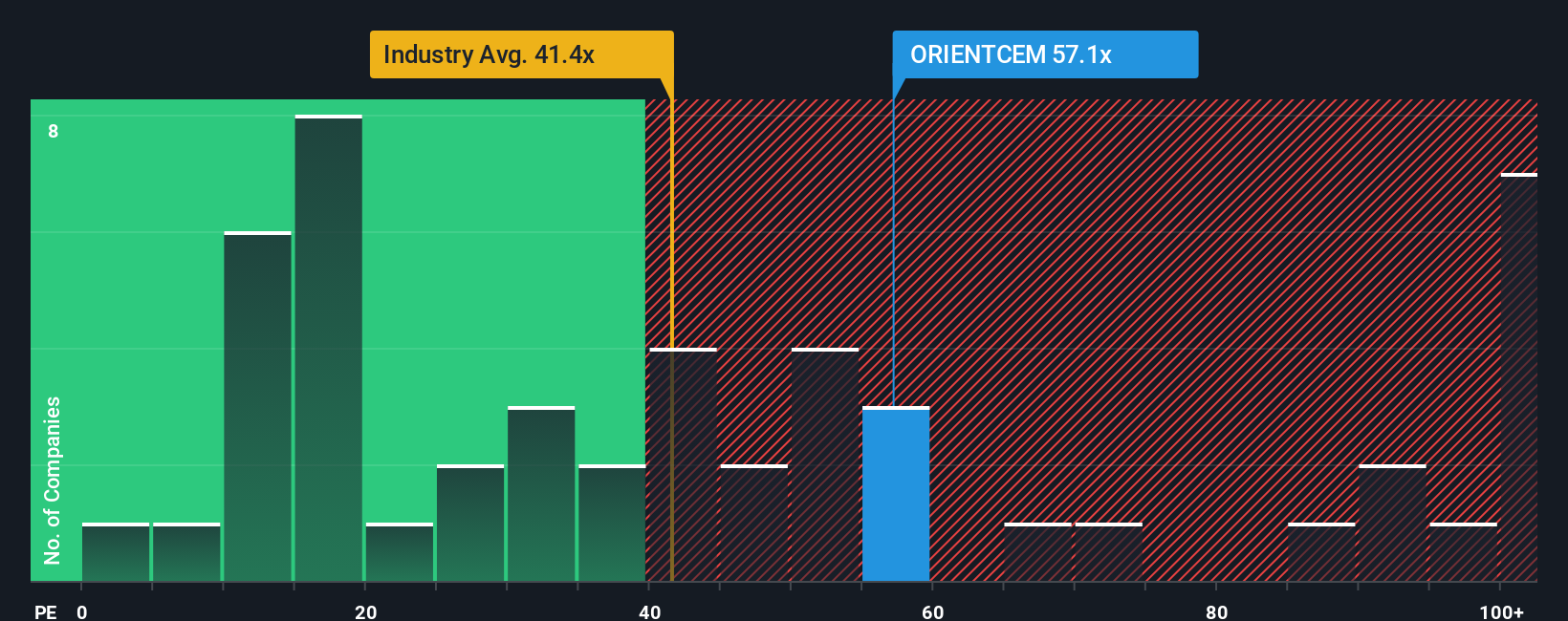

In spite of the heavy fall in price, given close to half the companies in India have price-to-earnings ratios (or "P/E's") below 29x, you may still consider Orient Cement as a stock to avoid entirely with its 57.1x P/E ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

While the market has experienced earnings growth lately, Orient Cement's earnings have gone into reverse gear, which is not great. It might be that many expect the dour earnings performance to recover substantially, which has kept the P/E from collapsing. If not, then existing shareholders may be extremely nervous about the viability of the share price.

View our latest analysis for Orient Cement

How Is Orient Cement's Growth Trending?

Orient Cement's P/E ratio would be typical for a company that's expected to deliver very strong growth, and importantly, perform much better than the market.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 48%. This means it has also seen a slide in earnings over the longer-term as EPS is down 65% in total over the last three years. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Looking ahead now, EPS is anticipated to climb by 212% during the coming year according to the sole analyst following the company. With the market only predicted to deliver 23%, the company is positioned for a stronger earnings result.

In light of this, it's understandable that Orient Cement's P/E sits above the majority of other companies. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Key Takeaway

Orient Cement's shares may have retreated, but its P/E is still flying high. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that Orient Cement maintains its high P/E on the strength of its forecast growth being higher than the wider market, as expected. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. It's hard to see the share price falling strongly in the near future under these circumstances.

Plus, you should also learn about this 1 warning sign we've spotted with Orient Cement.

Of course, you might also be able to find a better stock than Orient Cement. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.