- LIVE QUOTES

- LEARN

- HELP

Wall Street Journal

Wall Street JournalEN

Improved Revenues Required Before Ultra Clean Holdings, Inc. (NASDAQ:UCTT) Shares Find Their Feet

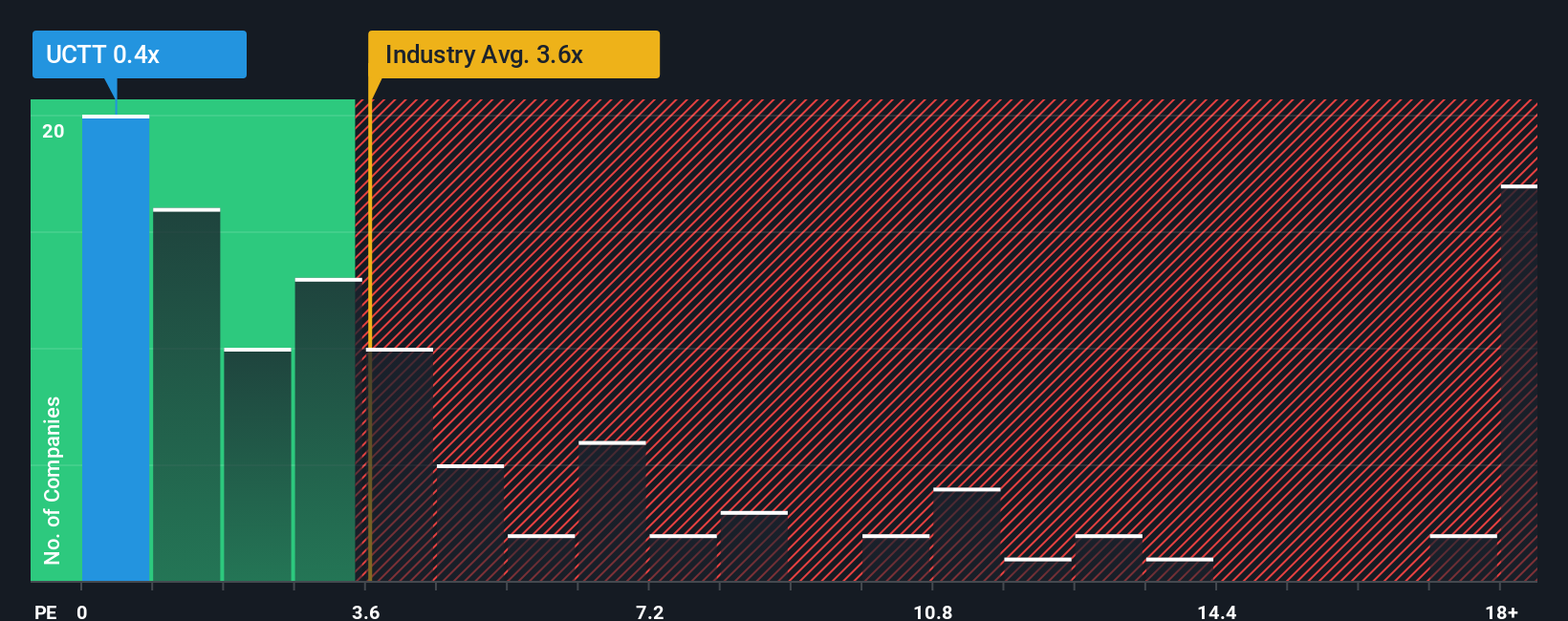

Ultra Clean Holdings, Inc.'s (NASDAQ:UCTT) price-to-sales (or "P/S") ratio of 0.4x might make it look like a strong buy right now compared to the Semiconductor industry in the United States, where around half of the companies have P/S ratios above 3.6x and even P/S above 10x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/S.

See our latest analysis for Ultra Clean Holdings

What Does Ultra Clean Holdings' P/S Mean For Shareholders?

With revenue growth that's inferior to most other companies of late, Ultra Clean Holdings has been relatively sluggish. Perhaps the market is expecting the current trend of poor revenue growth to continue, which has kept the P/S suppressed. If this is the case, then existing shareholders will probably struggle to get excited about the future direction of the share price.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Ultra Clean Holdings.Is There Any Revenue Growth Forecasted For Ultra Clean Holdings?

Ultra Clean Holdings' P/S ratio would be typical for a company that's expected to deliver very poor growth or even falling revenue, and importantly, perform much worse than the industry.

Retrospectively, the last year delivered an exceptional 20% gain to the company's top line. Despite this strong recent growth, it's still struggling to catch up as its three-year revenue frustratingly shrank by 4.9% overall. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

Turning to the outlook, the next three years should generate growth of 3.2% per year as estimated by the four analysts watching the company. With the industry predicted to deliver 21% growth per annum, the company is positioned for a weaker revenue result.

With this in consideration, its clear as to why Ultra Clean Holdings' P/S is falling short industry peers. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

The Final Word

Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

We've established that Ultra Clean Holdings maintains its low P/S on the weakness of its forecast growth being lower than the wider industry, as expected. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises. The company will need a change of fortune to justify the P/S rising higher in the future.

Plus, you should also learn about these 3 warning signs we've spotted with Ultra Clean Holdings.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.