- LIVE QUOTES

- LEARN

- HELP

Wall Street Journal

Wall Street JournalEN

Telefónica (BME:TEF) Has Announced A Dividend Of €0.1215

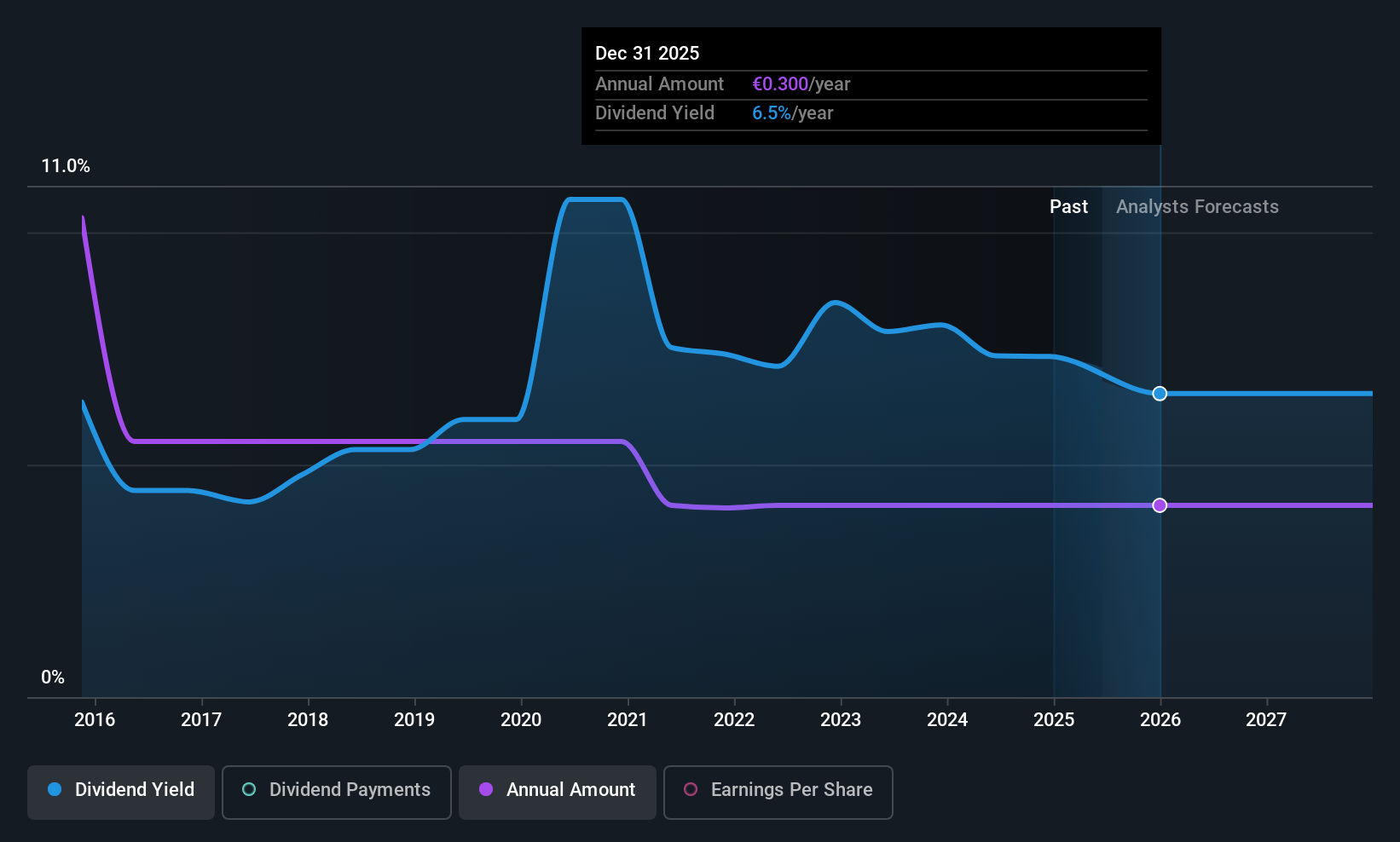

Telefónica, S.A. (BME:TEF) will pay a dividend of €0.1215 on the 19th of June. This means the annual payment is 6.5% of the current stock price, which is above the average for the industry.

Telefónica's Projections Indicate Future Payments May Be Unsustainable

Estimates Indicate Telefónica's Could Struggle to Maintain Dividend Payments In The Future

Telefónica's Future Dividends May Potentially Be At Risk

Impressive dividend yields are good, but this doesn't matter much if the payments can't be sustained. Even though Telefónica isn't generating a profit, it is generating healthy free cash flows that easily cover the dividend. We generally think that cash flow is more important than accounting measures of profit, so we are fairly comfortable with the dividend at this level.

EPS is forecast to rise very quickly over the next 12 months. If recent patterns in the dividend continues, we would start to get a bit worried, with the payout ratio possibly reaching 267%.

Check out our latest analysis for Telefónica

Dividend Volatility

The company has a long dividend track record, but it doesn't look great with cuts in the past. Since 2015, the dividend has gone from €0.75 total annually to €0.30. This works out to be a decline of approximately 8.8% per year over that time. Declining dividends isn't generally what we look for as they can indicate that the company is running into some challenges.

Dividend Growth Potential Is Shaky

Given that the track record hasn't been stellar, we really want to see earnings per share growing over time. Telefónica's earnings per share has shrunk at 37% a year over the past five years. A sharp decline in earnings per share is not great from from a dividend perspective. Even conservative payout ratios can come under pressure if earnings fall far enough. It's not all bad news though, as the earnings are predicted to rise over the next 12 months - we would just be a bit cautious until this becomes a long term trend.

The Dividend Could Prove To Be Unreliable

In summary, while it's good to see that the dividend hasn't been cut, we are a bit cautious about Telefónica's payments, as there could be some issues with sustaining them into the future. The payments haven't been particularly stable and we don't see huge growth potential, but with the dividend well covered by cash flows it could prove to be reliable over the short term. Overall, we don't think this company has the makings of a good income stock.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. However, there are other things to consider for investors when analysing stock performance. For example, we've identified 2 warning signs for Telefónica (1 makes us a bit uncomfortable!) that you should be aware of before investing. Is Telefónica not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.