- LIVE QUOTES

- LEARN

- HELP

Wall Street Journal

Wall Street JournalEN

After Leaping 28% PlaySide Studios Limited (ASX:PLY) Shares Are Not Flying Under The Radar

PlaySide Studios Limited (ASX:PLY) shareholders are no doubt pleased to see that the share price has bounced 28% in the last month, although it is still struggling to make up recently lost ground. But the last month did very little to improve the 77% share price decline over the last year.

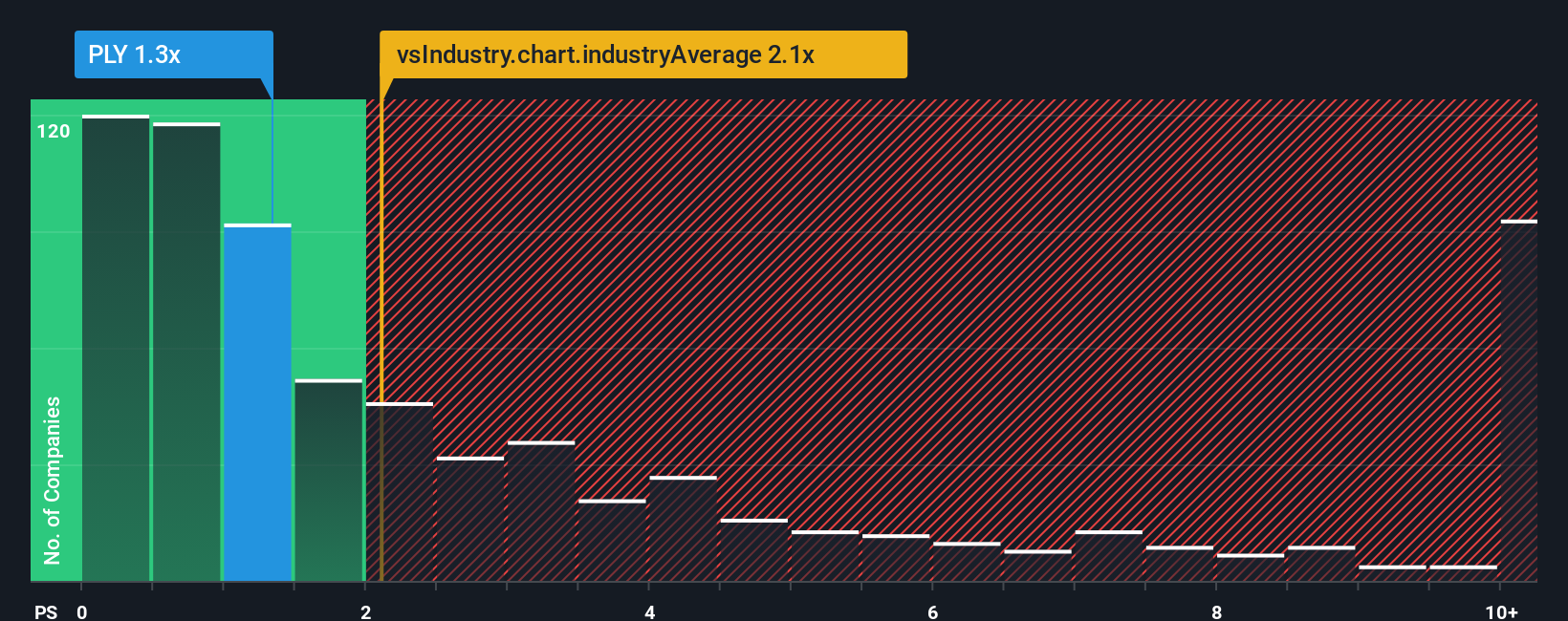

Even after such a large jump in price, you could still be forgiven for feeling indifferent about PlaySide Studios' P/S ratio of 1.3x, since the median price-to-sales (or "P/S") ratio for the Entertainment industry in Australia is also close to 1.5x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

Check out our latest analysis for PlaySide Studios

What Does PlaySide Studios' Recent Performance Look Like?

PlaySide Studios' negative revenue growth of late has neither been better nor worse than most other companies. The P/S ratio is probably moderate because investors think the company's revenue trend will continue to follow the rest of the industry. So while you could say the stock is cheap, investors will be looking for improvement before they see it as good value. In saying that, existing shareholders probably aren't too pessimistic about the share price if the company's revenue continues tracking the industry.

Keen to find out how analysts think PlaySide Studios' future stacks up against the industry? In that case, our free report is a great place to start.Is There Some Revenue Growth Forecasted For PlaySide Studios?

In order to justify its P/S ratio, PlaySide Studios would need to produce growth that's similar to the industry.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 2.1%. Even so, admirably revenue has lifted 273% in aggregate from three years ago, notwithstanding the last 12 months. Accordingly, while they would have preferred to keep the run going, shareholders would definitely welcome the medium-term rates of revenue growth.

Shifting to the future, estimates from the dual analysts covering the company suggest revenue should grow by 13% per year over the next three years. Meanwhile, the rest of the industry is forecast to expand by 13% each year, which is not materially different.

With this information, we can see why PlaySide Studios is trading at a fairly similar P/S to the industry. It seems most investors are expecting to see average future growth and are only willing to pay a moderate amount for the stock.

What We Can Learn From PlaySide Studios' P/S?

PlaySide Studios appears to be back in favour with a solid price jump bringing its P/S back in line with other companies in the industry While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

We've seen that PlaySide Studios maintains an adequate P/S seeing as its revenue growth figures match the rest of the industry. At this stage investors feel the potential for an improvement or deterioration in revenue isn't great enough to push P/S in a higher or lower direction. Unless these conditions change, they will continue to support the share price at these levels.

We don't want to rain on the parade too much, but we did also find 2 warning signs for PlaySide Studios that you need to be mindful of.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.