- LIVE QUOTES

- LEARN

- HELP

Wall Street Journal

Wall Street JournalEN

Jubilant FoodWorks Limited's (NSE:JUBLFOOD) Shares May Have Run Too Fast Too Soon

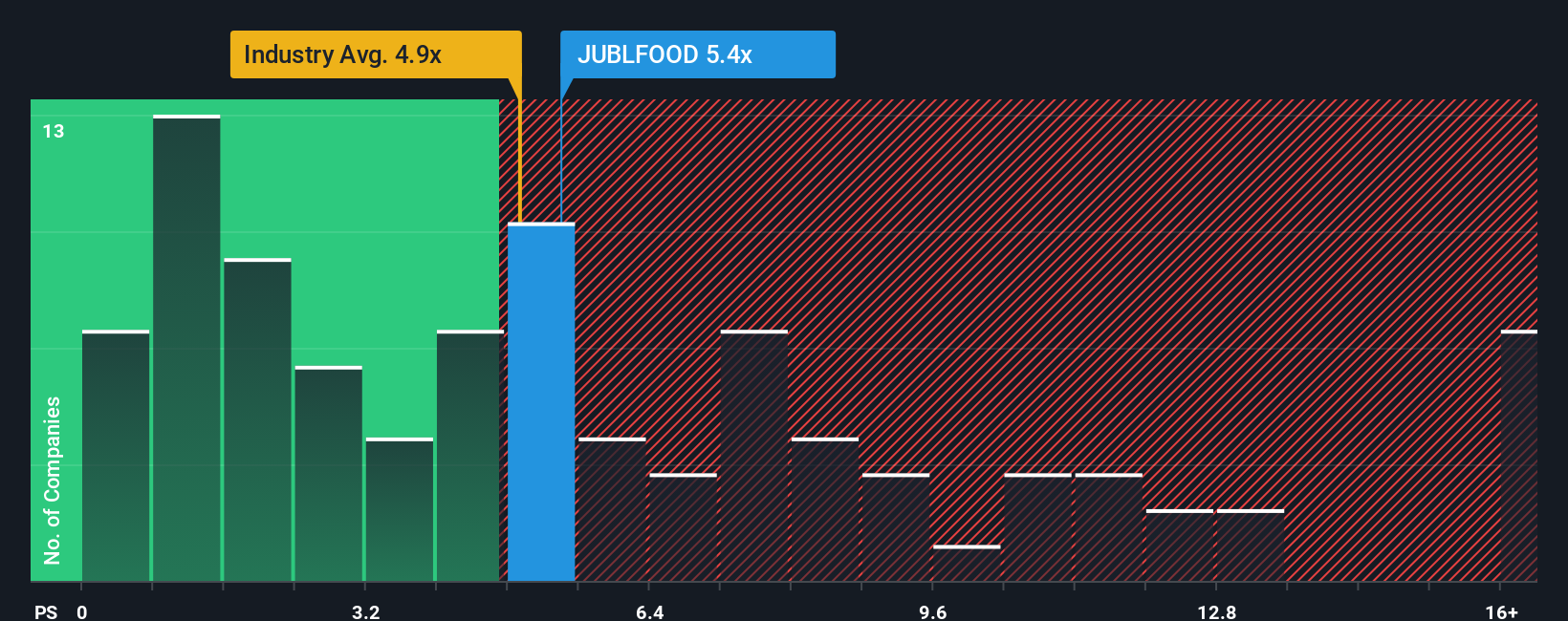

It's not a stretch to say that Jubilant FoodWorks Limited's (NSE:JUBLFOOD) price-to-sales (or "P/S") ratio of 5.4x right now seems quite "middle-of-the-road" for companies in the Hospitality industry in India, where the median P/S ratio is around 4.9x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

Check out our latest analysis for Jubilant FoodWorks

How Jubilant FoodWorks Has Been Performing

There hasn't been much to differentiate Jubilant FoodWorks' and the industry's revenue growth lately. Perhaps the market is expecting future revenue performance to show no drastic signs of changing, justifying the P/S being at current levels. Those who are bullish on Jubilant FoodWorks will be hoping that revenue performance can pick up, so that they can pick up the stock at a slightly lower valuation.

Keen to find out how analysts think Jubilant FoodWorks' future stacks up against the industry? In that case, our free report is a great place to start.How Is Jubilant FoodWorks' Revenue Growth Trending?

The only time you'd be comfortable seeing a P/S like Jubilant FoodWorks' is when the company's growth is tracking the industry closely.

Retrospectively, the last year delivered an exceptional 44% gain to the company's top line. The strong recent performance means it was also able to grow revenue by 85% in total over the last three years. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Turning to the outlook, the next three years should generate growth of 14% per year as estimated by the analysts watching the company. That's shaping up to be materially lower than the 26% per year growth forecast for the broader industry.

In light of this, it's curious that Jubilant FoodWorks' P/S sits in line with the majority of other companies. Apparently many investors in the company are less bearish than analysts indicate and aren't willing to let go of their stock right now. These shareholders may be setting themselves up for future disappointment if the P/S falls to levels more in line with the growth outlook.

The Key Takeaway

Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

Our look at the analysts forecasts of Jubilant FoodWorks' revenue prospects has shown that its inferior revenue outlook isn't negatively impacting its P/S as much as we would have predicted. When we see companies with a relatively weaker revenue outlook compared to the industry, we suspect the share price is at risk of declining, sending the moderate P/S lower. This places shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 2 warning signs with Jubilant FoodWorks (at least 1 which is significant), and understanding these should be part of your investment process.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.