- LIVE QUOTES

- LEARN

- HELP

Wall Street Journal

Wall Street JournalEN

Is Mangalam Global Enterprise (NSE:MGEL) Using Too Much Debt?

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies Mangalam Global Enterprise Limited (NSE:MGEL) makes use of debt. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

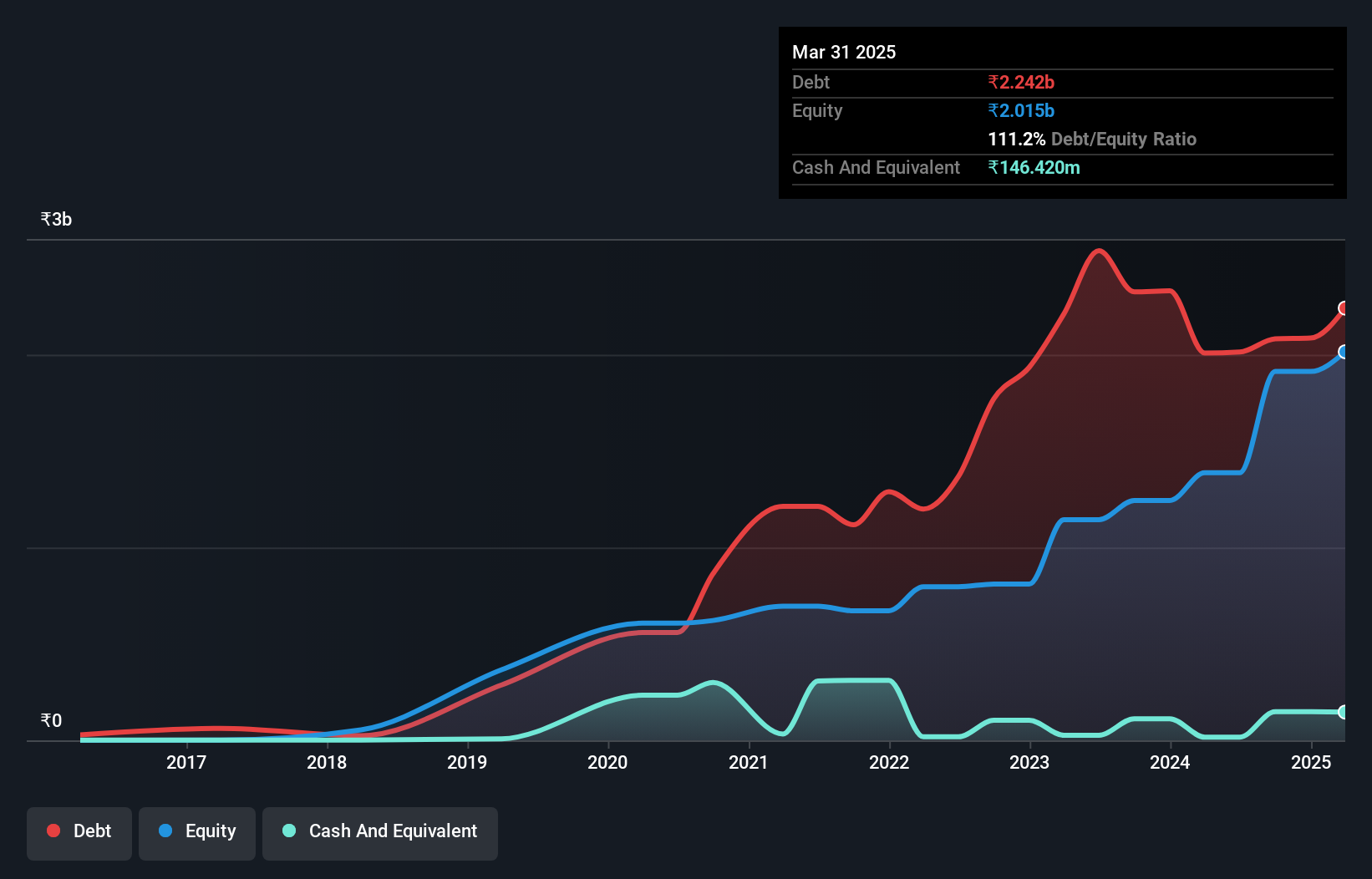

What Is Mangalam Global Enterprise's Debt?

The image below, which you can click on for greater detail, shows that at March 2025 Mangalam Global Enterprise had debt of ₹2.24b, up from ₹2.01b in one year. However, it does have ₹146.4m in cash offsetting this, leading to net debt of about ₹2.10b.

How Healthy Is Mangalam Global Enterprise's Balance Sheet?

The latest balance sheet data shows that Mangalam Global Enterprise had liabilities of ₹3.33b due within a year, and liabilities of ₹213.9m falling due after that. On the other hand, it had cash of ₹146.4m and ₹2.86b worth of receivables due within a year. So it has liabilities totalling ₹537.4m more than its cash and near-term receivables, combined.

Given Mangalam Global Enterprise has a market capitalization of ₹4.46b, it's hard to believe these liabilities pose much threat. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse.

View our latest analysis for Mangalam Global Enterprise

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

While we wouldn't worry about Mangalam Global Enterprise's net debt to EBITDA ratio of 4.7, we think its super-low interest cover of 1.4 times is a sign of high leverage. It seems clear that the cost of borrowing money is negatively impacting returns for shareholders, of late. On the other hand, Mangalam Global Enterprise grew its EBIT by 29% in the last year. If sustained, this growth should make that debt evaporate like a scarce drinking water during an unnaturally hot summer. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Mangalam Global Enterprise will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the last three years, Mangalam Global Enterprise saw substantial negative free cash flow, in total. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

While Mangalam Global Enterprise's interest cover makes us cautious about it, its track record of converting EBIT to free cash flow is no better. But at least its EBIT growth rate is a gleaming silver lining to those clouds. We think that Mangalam Global Enterprise's debt does make it a bit risky, after considering the aforementioned data points together. Not all risk is bad, as it can boost share price returns if it pays off, but this debt risk is worth keeping in mind. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. Be aware that Mangalam Global Enterprise is showing 3 warning signs in our investment analysis , and 1 of those can't be ignored...

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.