- LIVE QUOTES

- LEARN

- HELP

Wall Street Journal

Wall Street JournalEN

Optimistic Investors Push OKG Technology Holdings Limited (HKG:1499) Shares Up 66% But Growth Is Lacking

OKG Technology Holdings Limited (HKG:1499) shares have had a really impressive month, gaining 66% after a shaky period beforehand. Looking further back, the 24% rise over the last twelve months isn't too bad notwithstanding the strength over the last 30 days.

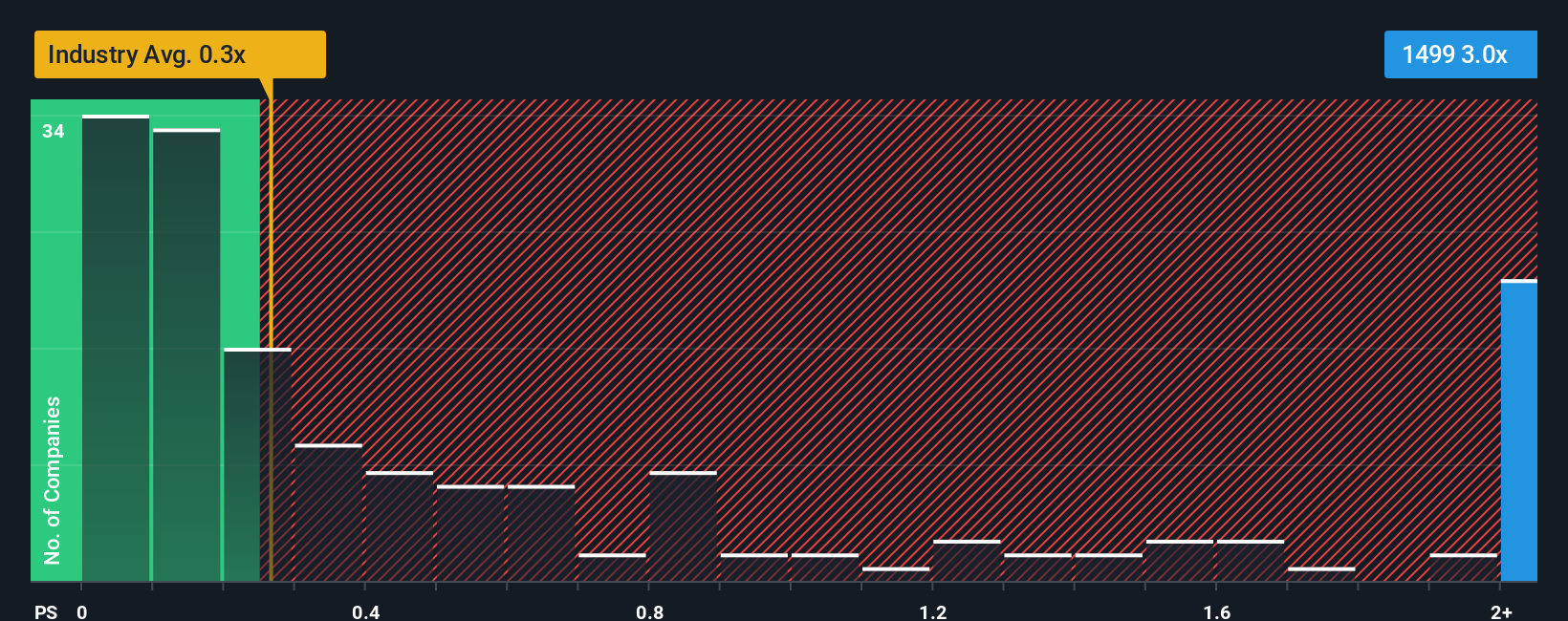

After such a large jump in price, you could be forgiven for thinking OKG Technology Holdings is a stock to steer clear of with a price-to-sales ratios (or "P/S") of 3x, considering almost half the companies in Hong Kong's Construction industry have P/S ratios below 0.3x. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

View our latest analysis for OKG Technology Holdings

How OKG Technology Holdings Has Been Performing

OKG Technology Holdings certainly has been doing a great job lately as it's been growing its revenue at a really rapid pace. It seems that many are expecting the strong revenue performance to beat most other companies over the coming period, which has increased investors’ willingness to pay up for the stock. However, if this isn't the case, investors might get caught out paying too much for the stock.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on OKG Technology Holdings will help you shine a light on its historical performance.How Is OKG Technology Holdings' Revenue Growth Trending?

The only time you'd be truly comfortable seeing a P/S as steep as OKG Technology Holdings' is when the company's growth is on track to outshine the industry decidedly.

Retrospectively, the last year delivered an exceptional 43% gain to the company's top line. Still, revenue has barely risen at all from three years ago in total, which is not ideal. So it appears to us that the company has had a mixed result in terms of growing revenue over that time.

Comparing that to the industry, which is predicted to deliver 16% growth in the next 12 months, the company's momentum is weaker, based on recent medium-term annualised revenue results.

In light of this, it's alarming that OKG Technology Holdings' P/S sits above the majority of other companies. It seems most investors are ignoring the fairly limited recent growth rates and are hoping for a turnaround in the company's business prospects. There's a good chance existing shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with recent growth rates.

The Bottom Line On OKG Technology Holdings' P/S

OKG Technology Holdings' P/S has grown nicely over the last month thanks to a handy boost in the share price. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

The fact that OKG Technology Holdings currently trades on a higher P/S relative to the industry is an oddity, since its recent three-year growth is lower than the wider industry forecast. When we observe slower-than-industry revenue growth alongside a high P/S ratio, we assume there to be a significant risk of the share price decreasing, which would result in a lower P/S ratio. Unless there is a significant improvement in the company's medium-term performance, it will be difficult to prevent the P/S ratio from declining to a more reasonable level.

You should always think about risks. Case in point, we've spotted 1 warning sign for OKG Technology Holdings you should be aware of.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.