- LIVE QUOTES

- LEARN

- HELP

Wall Street Journal

Wall Street JournalEN

TE Connectivity (NYSE:TEL) Announces Regular Quarterly Dividend of US$0.71 Per Share

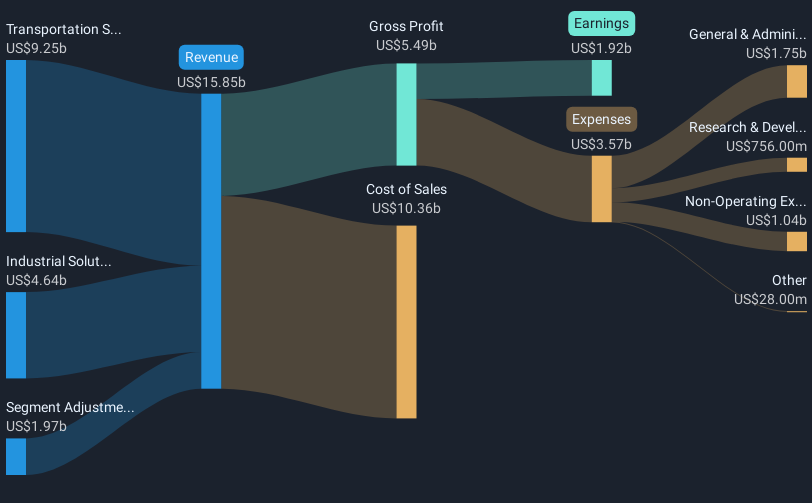

TE Connectivity (NYSE:TEL) recently announced a dividend affirmation, with a regular quarterly cash dividend of $0.71 per share, adding weight to the company's positive performance. Over the last quarter, the company's share price rose by 17%, significantly outpacing the broader market's 1% gain over the same period. Key events that likely contributed to this robust performance include the update to its share buyback program and corporate guidance for increased net sales and earnings per share. Despite a notable drop in net income, these strategic financial maneuvers seem to have reinforced positive investor sentiment.

TE Connectivity's recent dividend affirmation and share buyback program update are likely to have strengthened investor confidence, potentially supporting future earnings and revenue growth expectations. The 17% rise in the company's share price over the last quarter can be seen as part of a broader positive trend, as evidenced by a substantial total shareholder return of 121.35% over the past five years. This five-year performance indicates robust long-term growth compared to a 12.8% return from the US market over the past year, where TE Connectivity underperformed. This suggests that while the company has recently lagged in annual performance versus the US market, its long-term returns remain impressive.

In light of the expected expansion in local manufacturing and artificial intelligence applications, investors might anticipate further improvements in operational efficiency and revenue increases, aligning with the company's focus on manufacturing proximity to customers to reduce tariff exposure. However, any impact of geopolitical tensions or slowdowns in certain segments could temper these forecasts. The recent guidance for increased net sales and earnings per share alongside the price movement brings the current share price of US$162.39 close to the consensus price target of US$162.06, which represents a minor 0.2% variance. This suggests that analysts currently view the company as fairly valued, factoring in the expected growth and potential risks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com