- LIVE QUOTES

- LEARN

- HELP

Wall Street Journal

Wall Street JournalEN

Cyrela Brazil Realty Empreendimentos e Participações' (BVMF:CYRE3) three-year total shareholder returns outpace the underlying earnings growth

The most you can lose on any stock (assuming you don't use leverage) is 100% of your money. But if you buy shares in a really great company, you can more than double your money. To wit, the Cyrela Brazil Realty S.A. Empreendimentos e Participações (BVMF:CYRE3) share price has flown 106% in the last three years. How nice for those who held the stock! On top of that, the share price is up 12% in about a quarter. But this move may well have been assisted by the reasonably buoyant market (up 7.8% in 90 days).

Since the long term performance has been good but there's been a recent pullback of 3.4%, let's check if the fundamentals match the share price.

While markets are a powerful pricing mechanism, share prices reflect investor sentiment, not just underlying business performance. One flawed but reasonable way to assess how sentiment around a company has changed is to compare the earnings per share (EPS) with the share price.

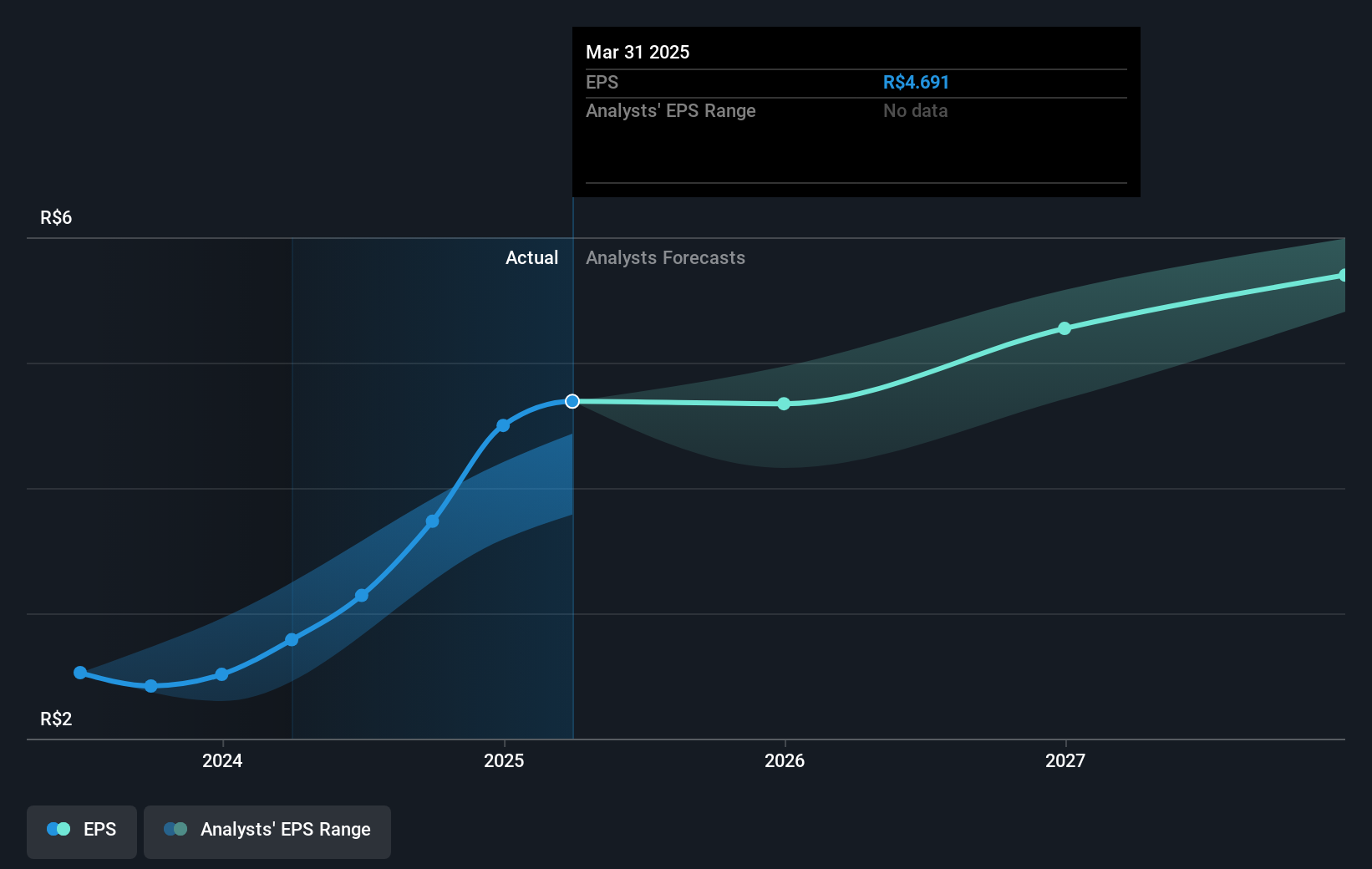

Cyrela Brazil Realty Empreendimentos e Participações was able to grow its EPS at 27% per year over three years, sending the share price higher. Notably, the 27% average annual share price gain matches up nicely with the EPS growth rate. That suggests that the market sentiment around the company hasn't changed much over that time. Rather, the share price has approximately tracked EPS growth.

The image below shows how EPS has tracked over time (if you click on the image you can see greater detail).

We know that Cyrela Brazil Realty Empreendimentos e Participações has improved its bottom line lately, but is it going to grow revenue? Check if analysts think Cyrela Brazil Realty Empreendimentos e Participações will grow revenue in the future.

What About Dividends?

When looking at investment returns, it is important to consider the difference between total shareholder return (TSR) and share price return. The TSR is a return calculation that accounts for the value of cash dividends (assuming that any dividend received was reinvested) and the calculated value of any discounted capital raisings and spin-offs. It's fair to say that the TSR gives a more complete picture for stocks that pay a dividend. In the case of Cyrela Brazil Realty Empreendimentos e Participações, it has a TSR of 132% for the last 3 years. That exceeds its share price return that we previously mentioned. The dividends paid by the company have thusly boosted the total shareholder return.

A Different Perspective

It's nice to see that Cyrela Brazil Realty Empreendimentos e Participações shareholders have received a total shareholder return of 33% over the last year. Of course, that includes the dividend. That's better than the annualised return of 9% over half a decade, implying that the company is doing better recently. Given the share price momentum remains strong, it might be worth taking a closer look at the stock, lest you miss an opportunity. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. For example, we've discovered 1 warning sign for Cyrela Brazil Realty Empreendimentos e Participações that you should be aware of before investing here.

We will like Cyrela Brazil Realty Empreendimentos e Participações better if we see some big insider buys. While we wait, check out this free list of undervalued stocks (mostly small caps) with considerable, recent, insider buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Brazilian exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.