- LIVE QUOTES

- LEARN

- HELP

Wall Street Journal

Wall Street JournalEN

PC Jeweller (NSE:PCJEWELLER) Posted Healthy Earnings But There Are Some Other Factors To Be Aware Of

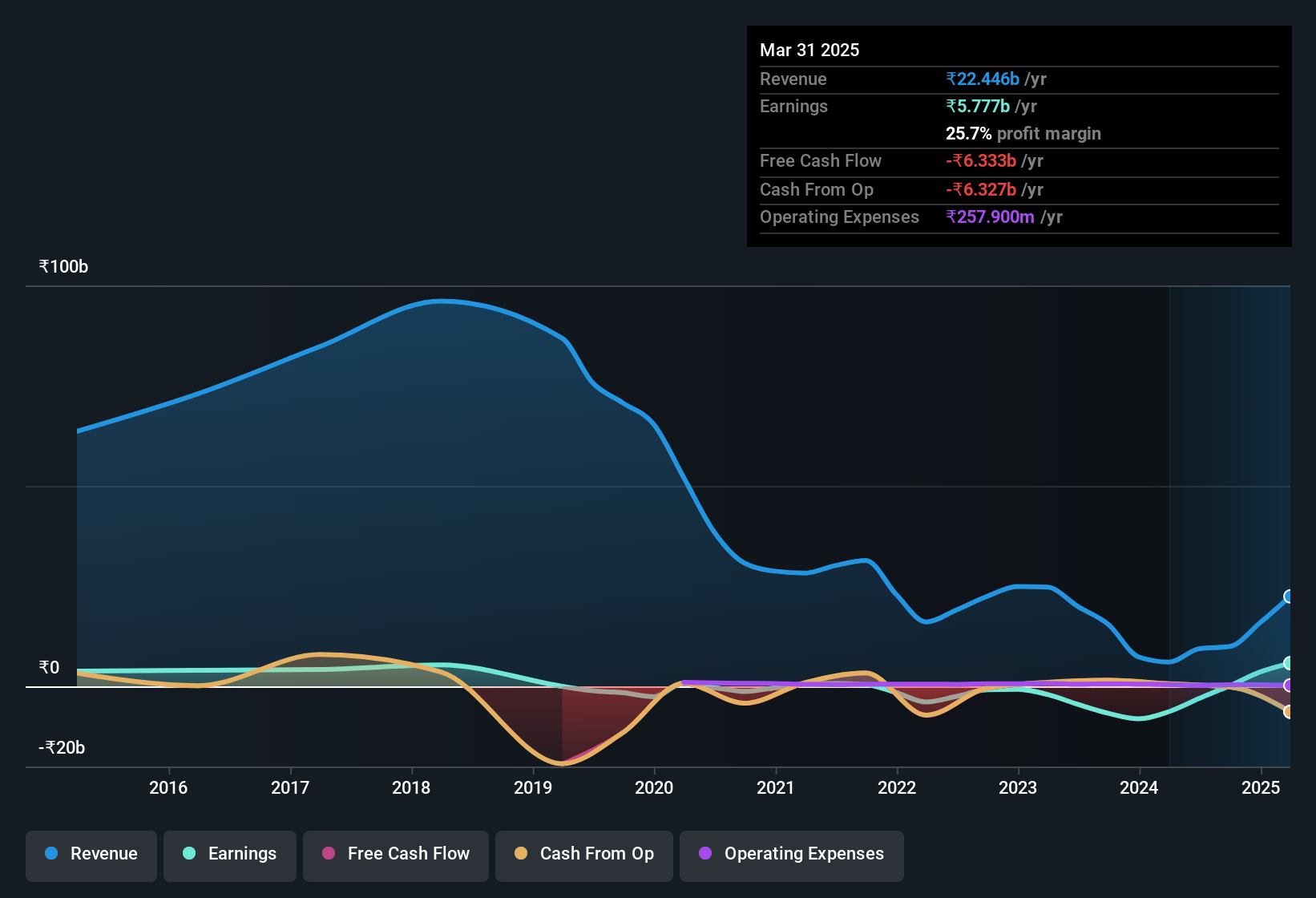

PC Jeweller Limited's (NSE:PCJEWELLER) stock was strong after they recently reported robust earnings. We did some analysis and think that investors are missing some details hidden beneath the profit numbers.

One essential aspect of assessing earnings quality is to look at how much a company is diluting shareholders. In fact, PC Jeweller increased the number of shares on issue by 41% over the last twelve months by issuing new shares. Therefore, each share now receives a smaller portion of profit. Per share metrics like EPS help us understand how much actual shareholders are benefitting from the company's profits, while the net income level gives us a better view of the company's absolute size. Check out PC Jeweller's historical EPS growth by clicking on this link.

How Is Dilution Impacting PC Jeweller's Earnings Per Share (EPS)?

PC Jeweller was losing money three years ago. And even focusing only on the last twelve months, we don't have a meaningful growth rate because it made a loss a year ago, too. What we do know is that while it's great to see a profit over the last twelve months, that profit would have been better, on a per share basis, if the company hadn't needed to issue shares. Therefore, one can observe that the dilution is having a fairly profound effect on shareholder returns.

If PC Jeweller's EPS can grow over time then that drastically improves the chances of the share price moving in the same direction. However, if its profit increases while its earnings per share stay flat (or even fall) then shareholders might not see much benefit. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of PC Jeweller.

Our Take On PC Jeweller's Profit Performance

Over the last year PC Jeweller issued new shares and so, there's a noteworthy divergence between EPS and net income growth. For this reason, we think that PC Jeweller's statutory profits may be a bad guide to its underlying earnings power, and might give investors an overly positive impression of the company. The good news is that it earned a profit in the last twelve months, despite its previous loss. At the end of the day, it's essential to consider more than just the factors above, if you want to understand the company properly. In light of this, if you'd like to do more analysis on the company, it's vital to be informed of the risks involved. For example, we've found that PC Jeweller has 2 warning signs (1 is a bit concerning!) that deserve your attention before going any further with your analysis.

Today we've zoomed in on a single data point to better understand the nature of PC Jeweller's profit. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.