- LIVE QUOTES

- LEARN

- HELP

EN

National Bank of Canada (TSE:NA) Is Increasing Its Dividend To CA$1.18

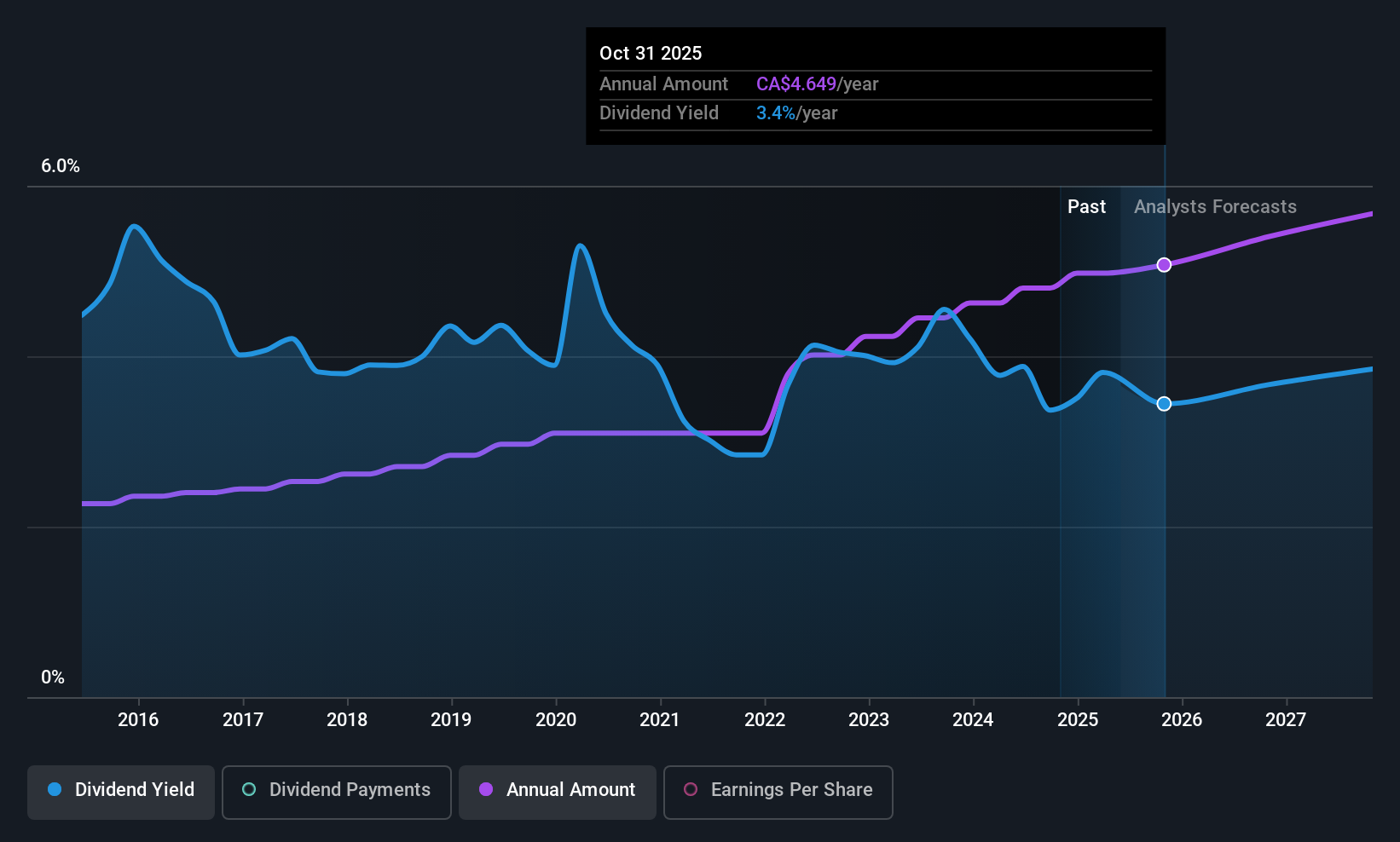

National Bank of Canada (TSE:NA) will increase its dividend from last year's comparable payment on the 1st of August to CA$1.18. Despite this raise, the dividend yield of 3.5% is only a modest boost to shareholder returns.

National Bank of Canada's Earnings Will Easily Cover The Distributions

If it is predictable over a long period, even low dividend yields can be attractive.

National Bank of Canada has a long history of paying out dividends, with its current track record at a minimum of 10 years. Based on National Bank of Canada's last earnings report, the payout ratio is at a decent 42%, meaning that the company is able to pay out its dividend with a bit of room to spare.

Looking forward, EPS is forecast to rise by 9.4% over the next 3 years. Analysts forecast the future payout ratio could be 44% over the same time horizon, which is a number we think the company can maintain.

View our latest analysis for National Bank of Canada

National Bank of Canada Has A Solid Track Record

The company has been paying a dividend for a long time, and it has been quite stable which gives us confidence in the future dividend potential. The dividend has gone from an annual total of CA$1.92 in 2015 to the most recent total annual payment of CA$4.72. This means that it has been growing its distributions at 9.4% per annum over that time. The growth of the dividend has been pretty reliable, so we think this can offer investors some nice additional income in their portfolio.

The Dividend Has Growth Potential

Investors could be attracted to the stock based on the quality of its payment history. We are encouraged to see that National Bank of Canada has grown earnings per share at 9.4% per year over the past five years. Earnings are on the uptrend, and it is only paying a small portion of those earnings to shareholders.

An additional note is that the company has been raising capital by issuing stock equal to 15% of shares outstanding in the last 12 months. Regularly doing this can be detrimental - it's hard to grow dividends per share when new shares are regularly being created.

We Really Like National Bank of Canada's Dividend

Overall, a dividend increase is always good, and we think that National Bank of Canada is a strong income stock thanks to its track record and growing earnings. The company is easily earning enough to cover its dividend payments and it is great to see that these earnings are being translated into cash flow. Taking this all into consideration, this looks like it could be a good dividend opportunity.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. Taking the debate a bit further, we've identified 1 warning sign for National Bank of Canada that investors need to be conscious of moving forward. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.