- LIVE QUOTES

- LEARN

- HELP

Wall Street Journal

Wall Street JournalEN

I-Tech AB's (STO:ITECH) P/E Is Still On The Mark Following 25% Share Price Bounce

I-Tech AB (STO:ITECH) shareholders have had their patience rewarded with a 25% share price jump in the last month. The annual gain comes to 101% following the latest surge, making investors sit up and take notice.

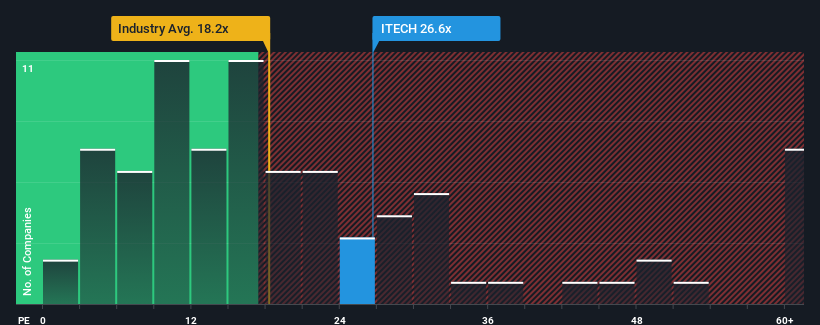

After such a large jump in price, given around half the companies in Sweden have price-to-earnings ratios (or "P/E's") below 22x, you may consider I-Tech as a stock to potentially avoid with its 26.6x P/E ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/E.

Recent times have been advantageous for I-Tech as its earnings have been rising faster than most other companies. It seems that many are expecting the strong earnings performance to persist, which has raised the P/E. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Check out our latest analysis for I-Tech

Does Growth Match The High P/E?

In order to justify its P/E ratio, I-Tech would need to produce impressive growth in excess of the market.

If we review the last year of earnings growth, the company posted a terrific increase of 106%. Although, its longer-term performance hasn't been as strong with three-year EPS growth being relatively non-existent overall. Therefore, it's fair to say that earnings growth has been inconsistent recently for the company.

Shifting to the future, estimates from the dual analysts covering the company suggest earnings should grow by 28% each year over the next three years. With the market only predicted to deliver 19% per annum, the company is positioned for a stronger earnings result.

With this information, we can see why I-Tech is trading at such a high P/E compared to the market. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Bottom Line On I-Tech's P/E

I-Tech's P/E is getting right up there since its shares have risen strongly. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

As we suspected, our examination of I-Tech's analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. It's hard to see the share price falling strongly in the near future under these circumstances.

Many other vital risk factors can be found on the company's balance sheet. Take a look at our free balance sheet analysis for I-Tech with six simple checks on some of these key factors.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with a strong growth track record, trading on a low P/E.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.