- LIVE QUOTES

- LEARN

- HELP

Wall Street Journal

Wall Street JournalEN

Independent Director Of Dorman Products Sold 26% Of Their Shares

Anyone interested in Dorman Products, Inc. (NASDAQ:DORM) should probably be aware that the Independent Director, John Gavin, recently divested US$380k worth of shares in the company, at an average price of US$131 each. That sale was 26% of their holding, so it does make us raise an eyebrow.

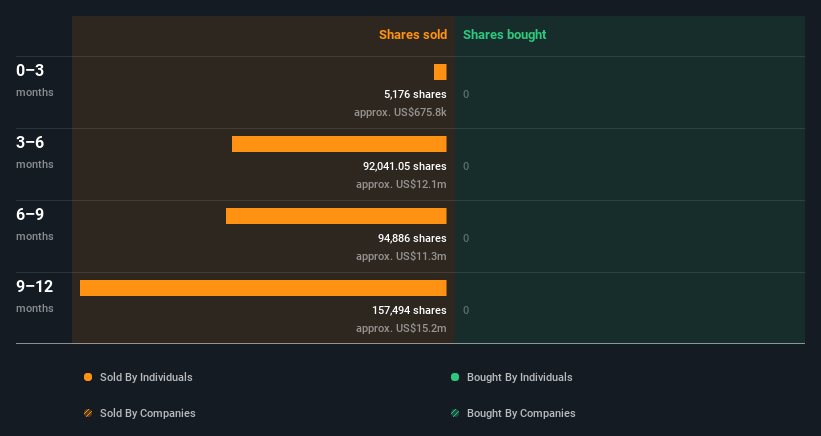

The Last 12 Months Of Insider Transactions At Dorman Products

The Founder & Non-Executive Chairman, Steven Berman, made the biggest insider sale in the last 12 months. That single transaction was for US$7.1m worth of shares at a price of US$94.01 each. That means that an insider was selling shares at slightly below the current price (US$126). As a general rule we consider it to be discouraging when insiders are selling below the current price, because it suggests they were happy with a lower valuation. While insider selling is not a positive sign, we can't be sure if it does mean insiders think the shares are fully valued, so it's only a weak sign. We note that the biggest single sale was only 2.9% of Steven Berman's holding.

Dorman Products insiders didn't buy any shares over the last year. The chart below shows insider transactions (by companies and individuals) over the last year. If you click on the chart, you can see all the individual transactions, including the share price, individual, and the date!

View our latest analysis for Dorman Products

I will like Dorman Products better if I see some big insider buys. While we wait, check out this free list of undervalued and small cap stocks with considerable, recent, insider buying.

Insider Ownership Of Dorman Products

For a common shareholder, it is worth checking how many shares are held by company insiders. Usually, the higher the insider ownership, the more likely it is that insiders will be incentivised to build the company for the long term. Dorman Products insiders own 9.3% of the company, currently worth about US$359m based on the recent share price. Most shareholders would be happy to see this sort of insider ownership, since it suggests that management incentives are well aligned with other shareholders.

What Might The Insider Transactions At Dorman Products Tell Us?

Insiders sold stock recently, but they haven't been buying. And there weren't any purchases to give us comfort, over the last year. But it is good to see that Dorman Products is growing earnings. The company boasts high insider ownership, but we're a little hesitant, given the history of share sales. While it's good to be aware of what's going on with the insider's ownership and transactions, we make sure to also consider what risks are facing a stock before making any investment decision. To assist with this, we've discovered 1 warning sign that you should run your eye over to get a better picture of Dorman Products.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of interesting companies.

For the purposes of this article, insiders are those individuals who report their transactions to the relevant regulatory body. We currently account for open market transactions and private dispositions of direct interests only, but not derivative transactions or indirect interests.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.