- LIVE QUOTES

- LEARN

- HELP

Wall Street Journal

Wall Street JournalEN

JAKKS Pacific And 2 Other Prominent Dividend Stocks

The United States market has experienced a modest climb of 1.3% over the past week and an 8.2% increase in the last year, with earnings expected to grow by 14% annually. In this environment, dividend stocks can offer investors a blend of income and potential appreciation, making them an attractive option for those seeking stability alongside growth prospects in their portfolios.

Top 10 Dividend Stocks In The United States

| Name | Dividend Yield | Dividend Rating |

| Columbia Banking System (NasdaqGS:COLB) | 5.99% | ★★★★★★ |

| Dillard's (NYSE:DDS) | 7.18% | ★★★★★★ |

| First Interstate BancSystem (NasdaqGS:FIBK) | 6.90% | ★★★★★★ |

| Ennis (NYSE:EBF) | 5.22% | ★★★★★★ |

| Chevron (NYSE:CVX) | 4.99% | ★★★★★★ |

| Douglas Dynamics (NYSE:PLOW) | 4.41% | ★★★★★☆ |

| Southside Bancshares (NYSE:SBSI) | 4.98% | ★★★★★☆ |

| Valley National Bancorp (NasdaqGS:VLY) | 4.98% | ★★★★★☆ |

| Huntington Bancshares (NasdaqGS:HBAN) | 4.07% | ★★★★★☆ |

| Carter's (NYSE:CRI) | 9.29% | ★★★★★☆ |

Click here to see the full list of 148 stocks from our Top US Dividend Stocks screener.

Underneath we present a selection of stocks filtered out by our screen.

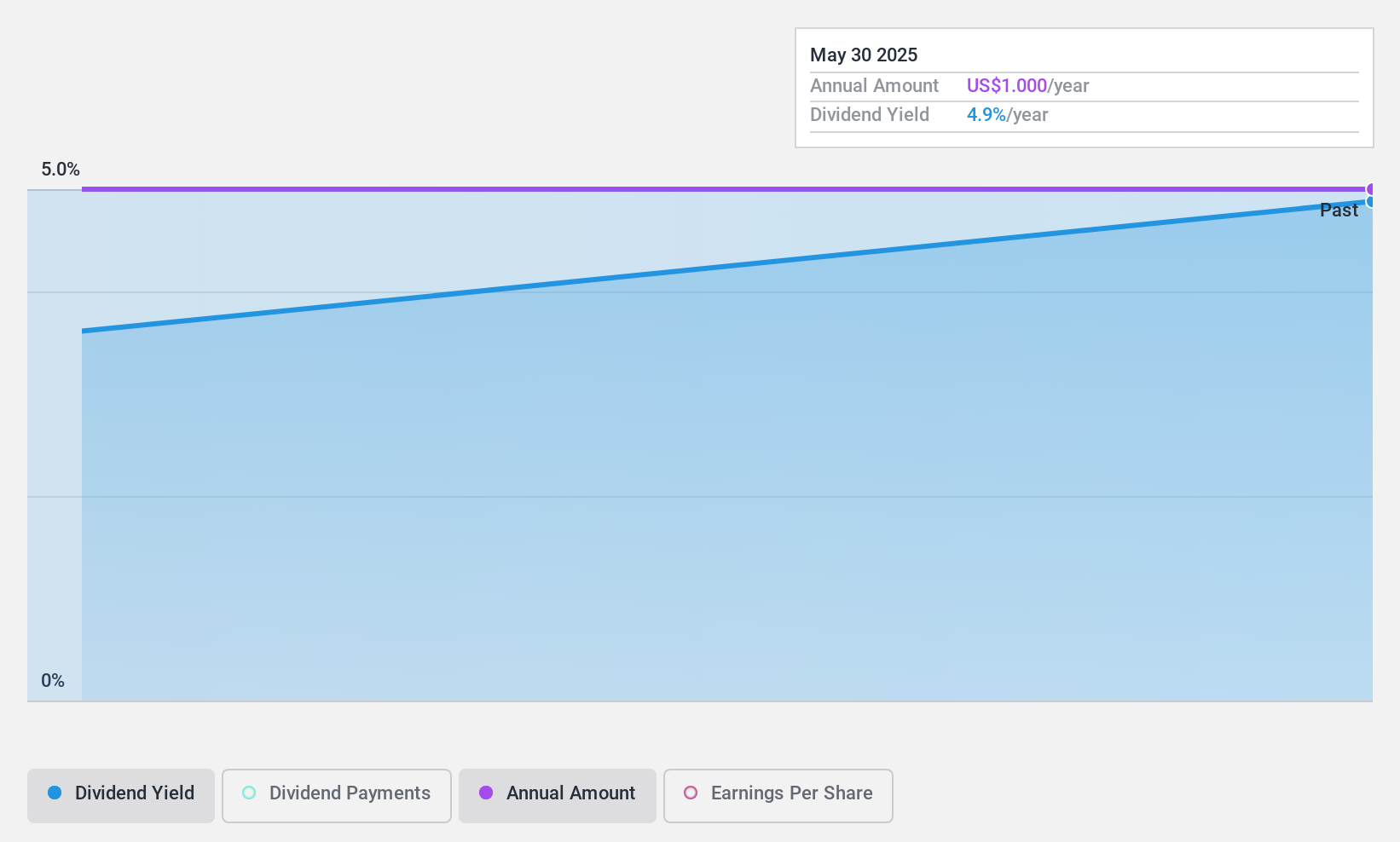

JAKKS Pacific (NasdaqGS:JAKK)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: JAKKS Pacific, Inc. is a global company that designs, produces, markets, sells, and distributes toys and related products, consumer goods including kids' furniture and costumes as well as sporting goods and home furnishings with a market cap of $208.10 million.

Operations: JAKKS Pacific, Inc. generates revenue through two main segments: Costumes, which contribute $119.67 million, and Toys/Consumer Products, which account for $594.55 million.

Dividend Yield: 5.2%

JAKKS Pacific recently initiated a quarterly dividend of $0.25 per share, with payments well-covered by earnings (payout ratio: 6%) and cash flows (cash payout ratio: 28.6%). Although the dividend yield of 5.15% ranks in the top 25% of U.S. payers, its reliability remains uncertain due to its recent inception. The company reported Q1 sales growth to US$113.25 million, narrowing net losses significantly from the previous year, indicating improving financial health amidst strategic licensing partnerships like DC x Sonic the Hedgehog.

- Click to explore a detailed breakdown of our findings in JAKKS Pacific's dividend report.

- In light of our recent valuation report, it seems possible that JAKKS Pacific is trading behind its estimated value.

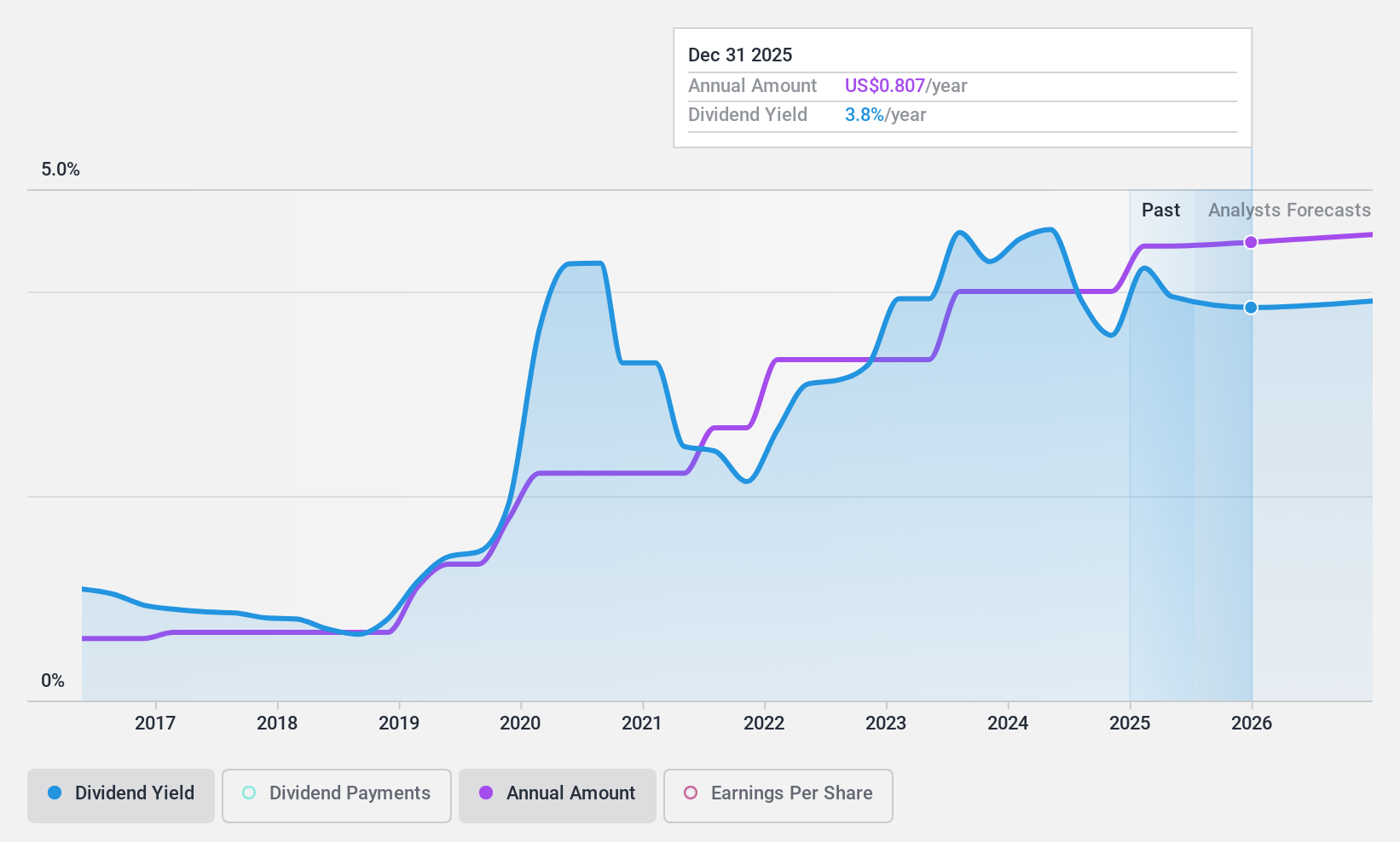

PCB Bancorp (NasdaqGS:PCB)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: PCB Bancorp is the bank holding company for PCB Bank, offering a range of banking products and services to small and middle market businesses and individuals, with a market cap of $280.80 million.

Operations: PCB Bancorp generates its revenue primarily from the banking industry, amounting to $98.72 million.

Dividend Yield: 4%

PCB Bancorp offers a stable dividend yield of 3.97%, though it falls short of the top quartile in the U.S. market. The dividends have been consistently reliable and growing over the past decade, supported by a low payout ratio of 37.7%. Recent earnings growth, with net income rising to US$7.74 million for Q1 2025, underscores financial strength, while a recent $0.20 per share dividend declaration highlights ongoing shareholder returns amidst strategic buybacks worth US$3.16 million since August 2023.

- Take a closer look at PCB Bancorp's potential here in our dividend report.

- According our valuation report, there's an indication that PCB Bancorp's share price might be on the cheaper side.

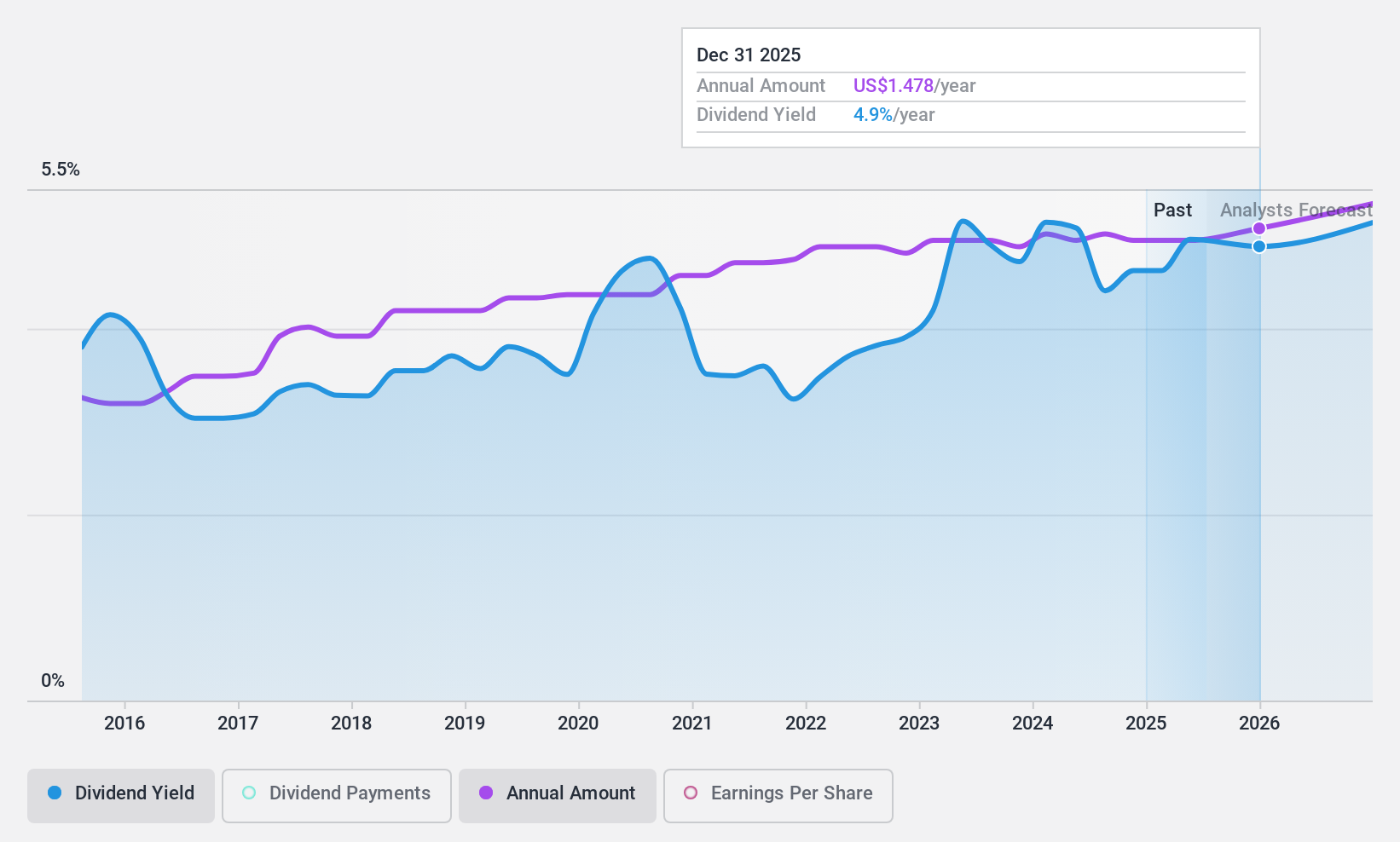

Southside Bancshares (NYSE:SBSI)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Southside Bancshares, Inc. is the bank holding company for Southside Bank, offering a range of financial services to individuals, businesses, municipal entities, and nonprofit organizations with a market cap of $855.66 million.

Operations: Southside Bancshares, Inc. generates revenue primarily through its banking operations, with a total of $254.82 million in this segment.

Dividend Yield: 5%

Southside Bancshares provides a compelling dividend yield of 4.98%, placing it among the top 25% in the U.S. market. The company's dividends have been stable and growing over the past decade, supported by a low payout ratio of 49.4%. Recent earnings results show net income steady at US$21.51 million for Q1 2025, despite net charge-offs decreasing to US$0.3 million, indicating solid financial health amidst upcoming board changes and no recent share buybacks completed this year.

- Click here and access our complete dividend analysis report to understand the dynamics of Southside Bancshares.

- Our valuation report unveils the possibility Southside Bancshares' shares may be trading at a discount.

Where To Now?

- Navigate through the entire inventory of 148 Top US Dividend Stocks here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com