- LIVE QUOTES

- LEARN

- HELP

Wall Street Journal

Wall Street JournalEN

Getting In Cheap On KRAFTON, Inc. (KRX:259960) Is Unlikely

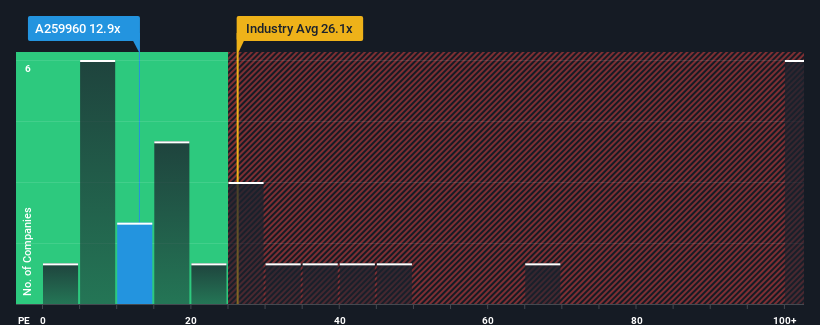

There wouldn't be many who think KRAFTON, Inc.'s (KRX:259960) price-to-earnings (or "P/E") ratio of 12.9x is worth a mention when the median P/E in Korea is similar at about 12x. While this might not raise any eyebrows, if the P/E ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

KRAFTON certainly has been doing a good job lately as it's been growing earnings more than most other companies. One possibility is that the P/E is moderate because investors think this strong earnings performance might be about to tail off. If not, then existing shareholders have reason to be feeling optimistic about the future direction of the share price.

View our latest analysis for KRAFTON

How Is KRAFTON's Growth Trending?

There's an inherent assumption that a company should be matching the market for P/E ratios like KRAFTON's to be considered reasonable.

Retrospectively, the last year delivered an exceptional 123% gain to the company's bottom line. The strong recent performance means it was also able to grow EPS by 134% in total over the last three years. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Turning to the outlook, the next three years should bring diminished returns, with earnings decreasing 2.2% per annum as estimated by the analysts watching the company. With the market predicted to deliver 18% growth per year, that's a disappointing outcome.

With this information, we find it concerning that KRAFTON is trading at a fairly similar P/E to the market. Apparently many investors in the company reject the analyst cohort's pessimism and aren't willing to let go of their stock right now. Only the boldest would assume these prices are sustainable as these declining earnings are likely to weigh on the share price eventually.

The Bottom Line On KRAFTON's P/E

Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

Our examination of KRAFTON's analyst forecasts revealed that its outlook for shrinking earnings isn't impacting its P/E as much as we would have predicted. Right now we are uncomfortable with the P/E as the predicted future earnings are unlikely to support a more positive sentiment for long. Unless these conditions improve, it's challenging to accept these prices as being reasonable.

And what about other risks? Every company has them, and we've spotted 2 warning signs for KRAFTON (of which 1 can't be ignored!) you should know about.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.