- LIVE QUOTES

- LEARN

- HELP

Wall Street Journal

Wall Street JournalEN

Exploring 3 Undervalued Small Caps In Asian Markets With Insider Action

Amid heightened global trade tensions and market volatility driven by recent tariff announcements, Asian markets are experiencing significant pressure, with small-cap stocks particularly affected as investors reassess growth prospects. In this challenging environment, identifying promising small-cap opportunities requires a focus on companies that demonstrate resilience and potential for growth despite broader economic uncertainties.

Top 10 Undervalued Small Caps With Insider Buying In Asia

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Security Bank | 4.7x | 1.1x | 39.99% | ★★★★★★ |

| New Hope | 5.5x | 1.6x | 35.81% | ★★★★★☆ |

| Atturra | 27.9x | 1.2x | 38.04% | ★★★★★☆ |

| Viva Energy Group | NA | 0.1x | 39.61% | ★★★★★☆ |

| Puregold Price Club | 8.9x | 0.4x | 9.55% | ★★★★☆☆ |

| Sing Investments & Finance | 7.2x | 3.7x | 42.37% | ★★★★☆☆ |

| Dicker Data | 18.9x | 0.7x | -35.10% | ★★★☆☆☆ |

| Hansen Technologies | 297.4x | 2.9x | 22.40% | ★★★☆☆☆ |

| Integral Diagnostics | 149.0x | 1.7x | 43.82% | ★★★☆☆☆ |

| Manawa Energy | NA | 2.6x | 42.78% | ★★★☆☆☆ |

Here's a peek at a few of the choices from the screener.

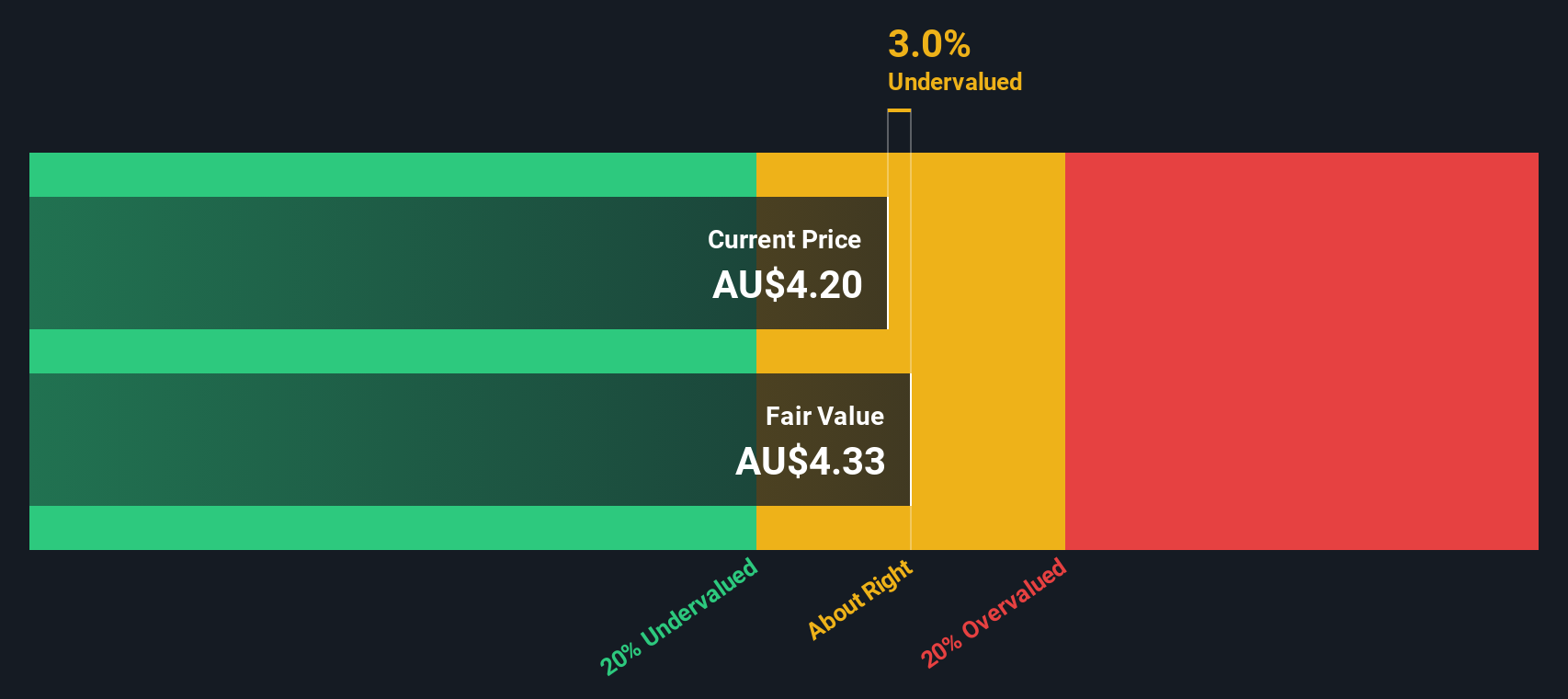

MyState (ASX:MYS)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: MyState is a financial services company operating primarily in banking and wealth management, with a market capitalization of A$0.57 billion.

Operations: Revenue is primarily generated through Banking and Wealth Management, with Banking contributing A$137.91 million and Wealth Management A$16.11 million. Operating expenses are a significant cost factor, with General & Administrative Expenses being the largest component at A$95.44 million in the latest period. The net income margin has shown variability, reaching 24% as of the most recent data point, reflecting changes in profitability over time.

PE: 12.1x

MyState's recent merger with Auswide Bank, forming a multi-brand group, positions it for expanded reach across Australia's eastern seaboard. Despite a modest decline in net income to A$15.92 million for the half-year ending December 2024, earnings are projected to grow by 18.55% annually. The company's low allowance for bad loans at 10% suggests prudent risk management. Insider confidence is evident through share purchases over the past year, indicating potential growth opportunities within its niche market segment.

- Click here to discover the nuances of MyState with our detailed analytical valuation report.

Gain insights into MyState's past trends and performance with our Past report.

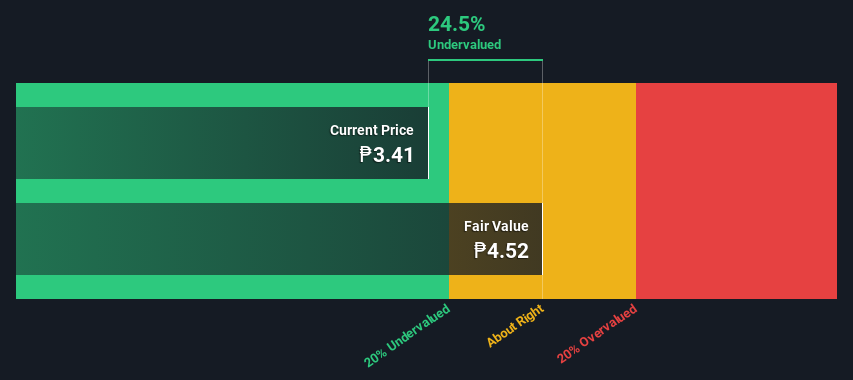

Bloomberry Resorts (PSE:BLOOM)

Simply Wall St Value Rating: ★★★★★☆

Overview: Bloomberry Resorts operates integrated resort facilities, primarily in the Philippines, with a market capitalization of ₱116.58 billion.

Operations: The company generates revenue primarily from its integrated resort facility, with recent figures showing a gross profit margin of 72.72%. Operating expenses are significant, impacting net income margins, which have shown variability over time.

PE: 12.0x

Bloomberry Resorts, a notable player in the Asian hospitality sector, has seen insider confidence with 9 million shares purchased by Cyrus Sherafat for approximately PHP 69.93 million. Despite recent volatility and a net loss of PHP 920 million in Q4 2024, revenue grew to PHP 52.76 billion annually from PHP 47.89 billion previously. The company declared a cash dividend and secured a favorable refinancing deal to ease debt burdens, positioning itself for potential growth amidst anticipated interest rate cuts.

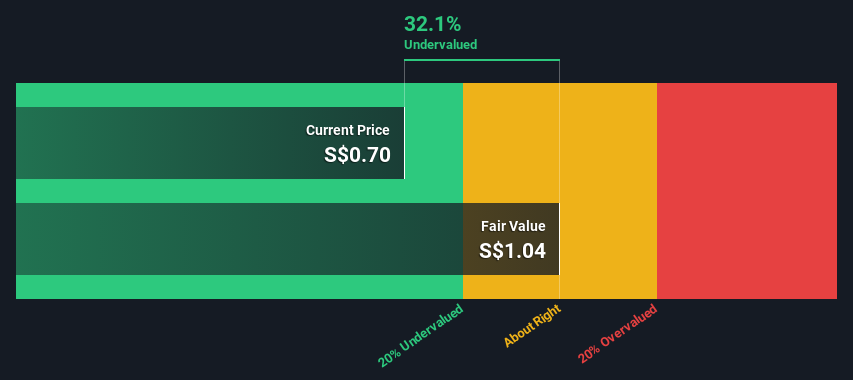

HRnetGroup (SGX:CHZ)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: HRnetGroup is a recruitment and staffing company specializing in flexible staffing and professional recruitment services, with a market cap of S$1.08 billion.

Operations: Flexible Staffing generates the majority of revenue at SGD 507.96 million, followed by Professional Recruitment at SGD 54.94 million. The gross profit margin has seen a decline from 39.64% in December 2014 to 21.55% in April 2025, indicating changes in cost efficiency or pricing strategies over time. Operating expenses include significant General & Administrative costs, which were SGD 75.35 million as of April 2025, affecting overall profitability alongside other non-operating expenses and sales & marketing expenditures.

PE: 14.3x

HRnetGroup, a smaller player in Asia's market, recently reported full-year 2024 sales of S$567 million, slightly down from the previous year. Despite a dip in net income to S$44.52 million, insider confidence is evident with share purchases over recent months. The company announced a final dividend of 2.13 cents per share for 2024, pending shareholder approval. Leadership changes are underway as Madeline Wan steps down from her role by February's end. Earnings growth is projected at 12% annually, suggesting potential future value amidst current challenges.

- Click here and access our complete valuation analysis report to understand the dynamics of HRnetGroup.

Understand HRnetGroup's track record by examining our Past report.

Taking Advantage

- Click through to start exploring the rest of the 57 Undervalued Asian Small Caps With Insider Buying now.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com