- LIVE QUOTES

- LEARN

- HELP

Wall Street Journal

Wall Street JournalEN

Serviceware SE (ETR:SJJ) CEO Dirk Martin, the company's largest shareholder sees 13% reduction in holdings value

Key Insights

- Significant insider control over Serviceware implies vested interests in company growth

- A total of 2 investors have a majority stake in the company with 63% ownership

- 23% of Serviceware is held by Institutions

Every investor in Serviceware SE (ETR:SJJ) should be aware of the most powerful shareholder groups. The group holding the most number of shares in the company, around 63% to be precise, is individual insiders. In other words, the group stands to gain the most (or lose the most) from their investment into the company.

And following last week's 13% decline in share price, insiders suffered the most losses.

Let's delve deeper into each type of owner of Serviceware, beginning with the chart below.

See our latest analysis for Serviceware

What Does The Institutional Ownership Tell Us About Serviceware?

Many institutions measure their performance against an index that approximates the local market. So they usually pay more attention to companies that are included in major indices.

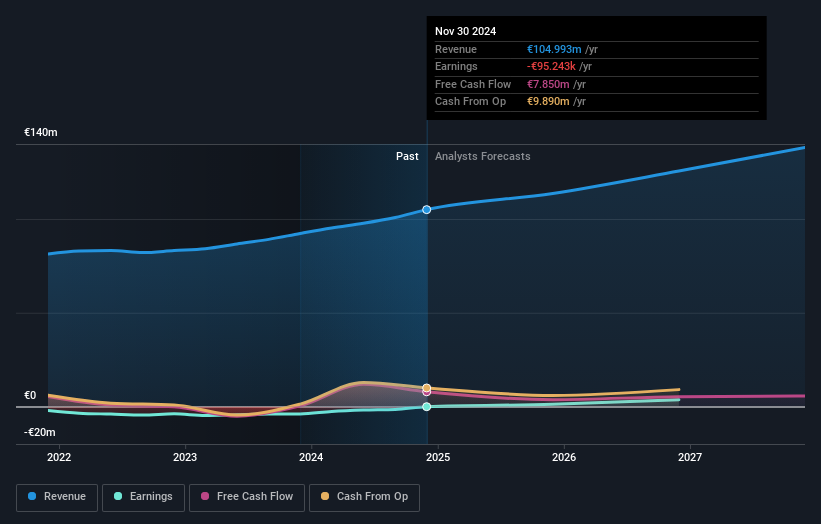

As you can see, institutional investors have a fair amount of stake in Serviceware. This implies the analysts working for those institutions have looked at the stock and they like it. But just like anyone else, they could be wrong. When multiple institutions own a stock, there's always a risk that they are in a 'crowded trade'. When such a trade goes wrong, multiple parties may compete to sell stock fast. This risk is higher in a company without a history of growth. You can see Serviceware's historic earnings and revenue below, but keep in mind there's always more to the story.

Hedge funds don't have many shares in Serviceware. The company's CEO Dirk Martin is the largest shareholder with 31% of shares outstanding. In comparison, the second and third largest shareholders hold about 31% and 5.1% of the stock. Interestingly, the second-largest shareholder, Harald Popp is also Chief Financial Officer, again, pointing towards strong insider ownership amongst the company's top shareholders.

A more detailed study of the shareholder registry showed us that 2 of the top shareholders have a considerable amount of ownership in the company, via their 63% stake.

While it makes sense to study institutional ownership data for a company, it also makes sense to study analyst sentiments to know which way the wind is blowing. While there is some analyst coverage, the company is probably not widely covered. So it could gain more attention, down the track.

Insider Ownership Of Serviceware

While the precise definition of an insider can be subjective, almost everyone considers board members to be insiders. Management ultimately answers to the board. However, it is not uncommon for managers to be executive board members, especially if they are a founder or the CEO.

Insider ownership is positive when it signals leadership are thinking like the true owners of the company. However, high insider ownership can also give immense power to a small group within the company. This can be negative in some circumstances.

Our information suggests that insiders own more than half of Serviceware SE. This gives them effective control of the company. Given it has a market cap of €131m, that means they have €82m worth of shares. Most would argue this is a positive, showing strong alignment with shareholders. You can click here to see if those insiders have been buying or selling.

General Public Ownership

With a 15% ownership, the general public, mostly comprising of individual investors, have some degree of sway over Serviceware. This size of ownership, while considerable, may not be enough to change company policy if the decision is not in sync with other large shareholders.

Next Steps:

I find it very interesting to look at who exactly owns a company. But to truly gain insight, we need to consider other information, too.

I like to dive deeper into how a company has performed in the past. You can access this interactive graph of past earnings, revenue and cash flow, for free .

But ultimately it is the future, not the past, that will determine how well the owners of this business will do. Therefore we think it advisable to take a look at this free report showing whether analysts are predicting a brighter future .

NB: Figures in this article are calculated using data from the last twelve months, which refer to the 12-month period ending on the last date of the month the financial statement is dated. This may not be consistent with full year annual report figures.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.