Is Gilead Sciences (GILD) Fully Valued Following Mixed Earnings And A Full Year EPS Miss?

Gilead Sciences (GILD) is back in focus after its latest earnings report, with revenue of $6.96b up 4.4% year on year, but a significant miss on full year EPS estimates weighing on sentiment.

See our latest analysis for Gilead Sciences.

At a share price of $136.30, Gilead Sciences has seen a 7.13% 1 month share price return and a small decline of 0.97% over 3 months. Its 1 year total shareholder return of 28.54% and 5 year total shareholder return of 138.29% point to momentum that has built over a longer horizon.

If Gilead’s recent move has you reassessing your watchlist, this is a good moment to see what else is setting up in the market with 39 healthcare AI stocks

Bulls point to Gilead Sciences’ revenue growth and long term returns, while bears focus on the EPS miss and recent wobble in sentiment. As you weigh the stock today, which side does the current valuation appear to support?

Most Popular Narrative: 6.2% Overvalued

Compared with the last close at $136.30, the most followed narrative for Gilead Sciences points to a fair value of $128.38, placing the stock slightly above that level in this framework.

Gilead is transitioning from a “single-franchise HIV company” into a multi-platform biopharma with high-probability growth drivers in lenacapavir and Trodelvy, plus meaningful upside from cell therapy and immunology. Near-term earnings headwinds from heavy investment and acquisitions sit in front of what the narrative views as a catalyst rich, medium term compounding story.

Curious how a medium term compounder case is built on steady revenue growth, expanding margins and a future earnings multiple usually reserved for faster growth sectors? The narrative leans on a detailed view of Gilead’s pipeline, expected cash generation and reinvestment, and then layers in a specific profit profile that supports its fair value. Want to see which revenue mix shifts and profitability assumptions are doing the heavy lifting in that model, and how much of the oncology and immunology opportunity it actually bakes in?

Result: Fair Value of $128.38 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this Gilead Sciences narrative can be knocked off course if key trials disappoint, or if acquisition integration goes poorly and drags on profitability.

Find out about the key risks to this Gilead Sciences narrative.

Another View: SWS DCF Says Gilead Sciences Looks Cheap

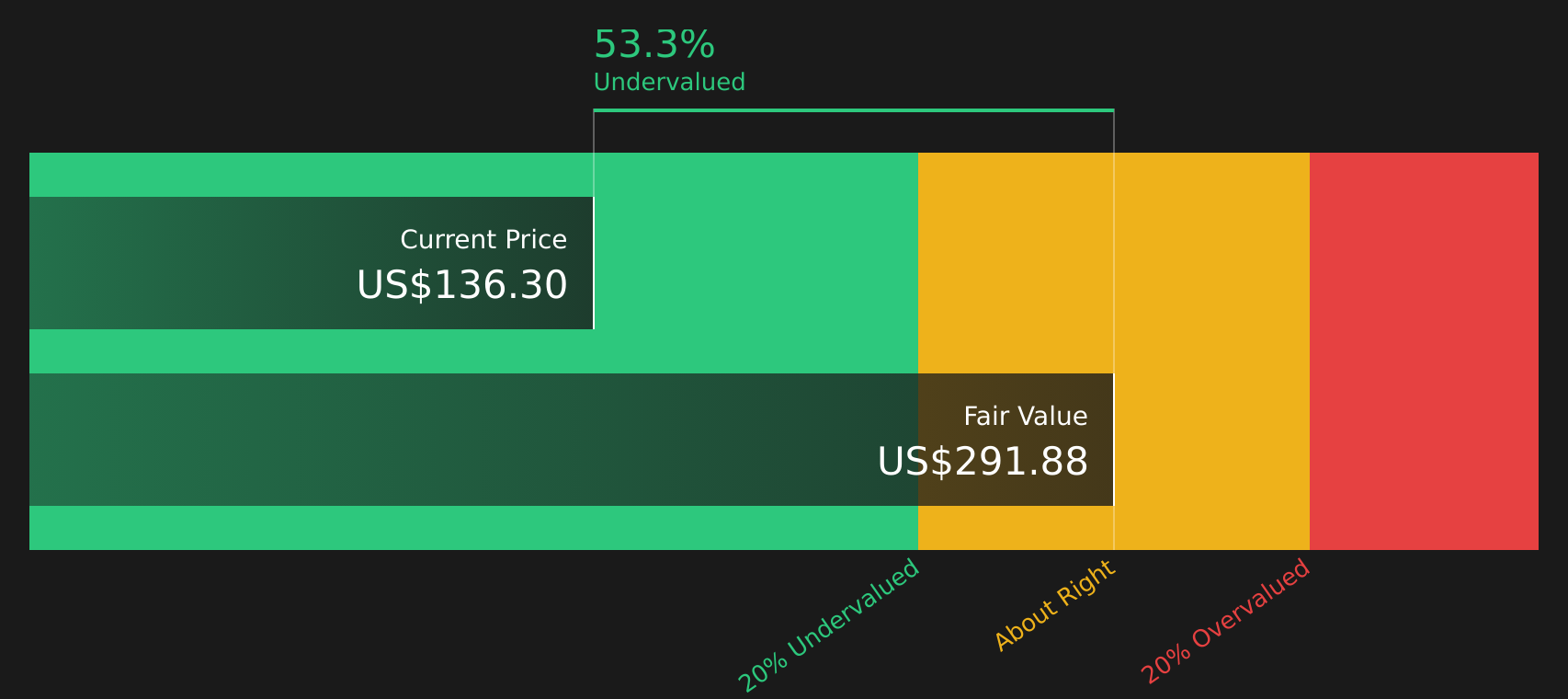

That 6.2% premium to a $128.38 fair value is only one side of the story. Our DCF model, using Gilead Sciences’ projected cash flows, points to a value of $291.88 per share, which is 53.3% above the current $136.30 price. Is the market underestimating this cash engine, or is the model too generous?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Gilead Sciences for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 50 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With Gilead Sciences pulling in both cautious and optimistic views, this is a useful moment to move quickly, review the data, and weigh the 4 key rewards and 1 important warning sign.

Looking for more investment ideas beyond Gilead Sciences?

If Gilead Sciences has sharpened your interest in new opportunities, this is a smart time to scan for other stocks that might deserve a spot on your radar.

- Target steady compounding potential by reviewing companies with strong cash flows and pricing that looks appealing through the 50 high quality undervalued stocks.

- Strengthen your income stream by checking out stocks with higher yields and resilient payout records in the 8 dividend fortresses.

- Prioritise resilience by focusing on companies with robust finances using the solid balance sheet and fundamentals stocks screener (48 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com