Arista Networks (ANET) Is Down 5.0% After Record AI Demand Meets Supply Chain Strains – What’s Changed

- In recent weeks, Arista Networks reported record demand for its AI-focused networking gear, raised its full-year revenue outlook to about US$11.50 billion, and cautioned that persistent supply chain bottlenecks and a US$6.20 billion deferred revenue balance could constrain how quickly orders convert into sales.

- The launch of Arista’s new 1.6-terabit 7060XE7 platforms and expanded Etherlink architecture underscores how AI data center buildouts are reshaping the company’s growth profile while increasing operational complexity and execution risk.

- Next, we’ll examine how this combination of record AI demand and supply chain strain could influence Arista Networks’ investment narrative.

Find 47 companies with promising cash flow potential yet trading below their fair value.

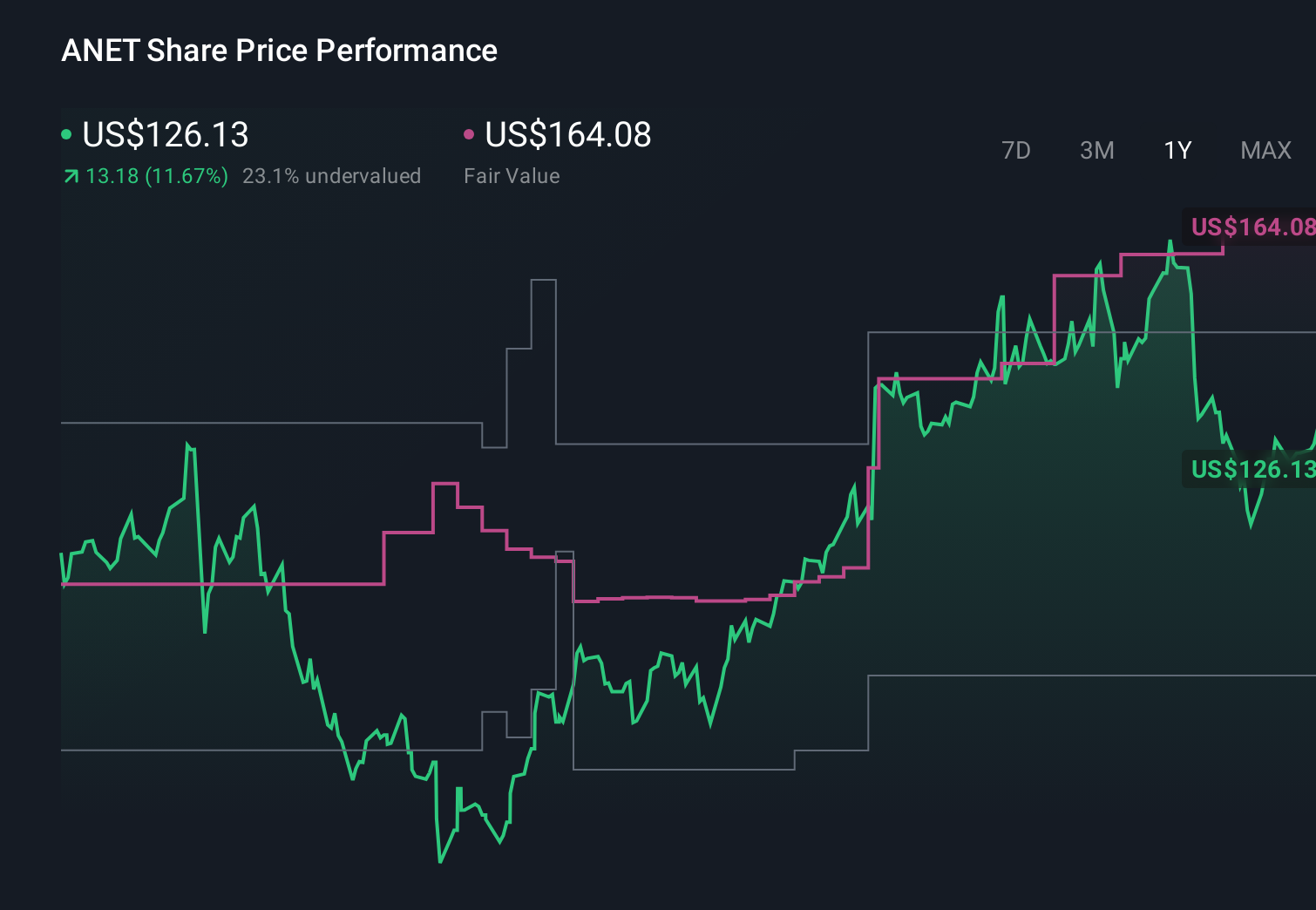

Arista Networks Investment Narrative Recap

To own Arista Networks, you need to believe that AI data center buildouts will keep requiring its high performance Ethernet and software platform, and that management can handle growing complexity without sacrificing profitability. The latest update reinforces that near term AI demand remains the key share price catalyst, while persistent supply bottlenecks and the US$6.20 billion deferred revenue pile are still the most immediate risks to how quickly that demand shows up in reported results.

Among recent announcements, the launch of Arista’s 1.6 terabit 7060XE7 platforms and expanded Etherlink AI architecture is especially relevant. It shows how deeply the company is tying its roadmap to large scale AI clusters, which supports the bullish AI networking thesis but also raises the execution bar around supply chain, product transitions, and integration with customers’ existing cloud operations.

Yet, despite all the excitement around AI orders, investors should be aware that supply ceilings and deferred revenue uncertainty could still...

Read the full narrative on Arista Networks (it's free!)

Arista Networks' narrative projects $18.2 billion revenue and $6.6 billion earnings by 2029.

Uncover how Arista Networks' forecasts yield a $190.09 fair value, a 11% upside to its current price.

Exploring Other Perspectives

The most bearish analysts were already baking in slower margin erosion, even while assuming revenue could still reach about US$16.3 billion and earnings US$6.0 billion by 2029, which shows how sharply views can differ and why this latest AI demand and supply chain news could shift those expectations again.

Explore 11 other fair value estimates on Arista Networks - why the stock might be worth 6% less than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Arista Networks research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Arista Networks research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Arista Networks' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 16 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com