Asian Market Value Picks Featuring Three Stocks With Estimated Intrinsic Discounts

Amidst the backdrop of geopolitical tensions and energy market volatility, Asian markets have shown mixed performance, with some indices experiencing declines while others have seen gains driven by technology sectors. In this environment, identifying undervalued stocks becomes crucial as investors seek opportunities that offer intrinsic value discounts relative to their current market prices.

Top 10 Undervalued Stocks Based On Cash Flows In Asia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Zhongji Innolight (SZSE:300308) | CN¥1169.31 | CN¥2333.85 | 49.9% |

| Xi'an Sinofuse Electric (SZSE:301031) | CN¥95.10 | CN¥190.06 | 50% |

| Softcare (SEHK:2698) | HK$27.04 | HK$53.46 | 49.4% |

| Shanghai Shengjian Technology (SHSE:603324) | CN¥34.93 | CN¥68.18 | 48.8% |

| Rakus (TSE:3923) | ¥1014.50 | ¥2024.40 | 49.9% |

| Moshi Moshi Retail Corporation (SET:MOSHI) | THB38.50 | THB75.10 | 48.7% |

| Laopu Gold (SEHK:6181) | HK$375.00 | HK$747.12 | 49.8% |

| Huatu Cendes (SZSE:300492) | CN¥23.15 | CN¥45.70 | 49.3% |

| China XLX Fertiliser (SEHK:1866) | HK$8.14 | HK$16.07 | 49.3% |

| BEAUTY GARAGE (TSE:3180) | ¥1466.00 | ¥2881.64 | 49.1% |

Here we highlight a subset of our preferred stocks from the screener.

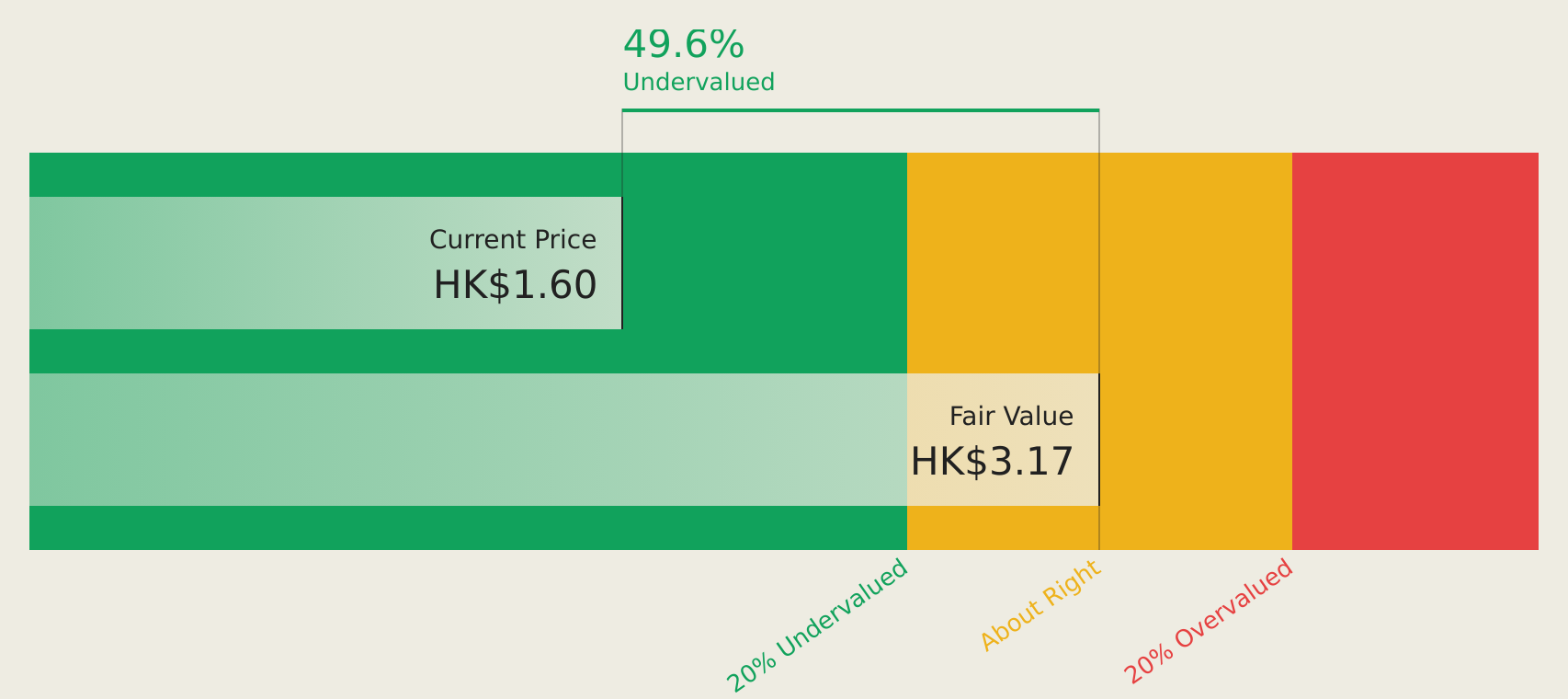

Shoucheng Holdings (SEHK:697)

Overview: Shoucheng Holdings Limited is an investment holding company focused on infrastructure asset management, with a market capitalization of approximately HK$13.51 billion.

Operations: The company generates revenue primarily from its infrastructure asset management business, totaling approximately HK$1.44 billion.

Estimated Discount To Fair Value: 48.2%

Shoucheng Holdings is trading at HK$1.66, significantly below its estimated future cash flow value of HK$3.2, indicating potential undervaluation based on cash flows. The company's earnings are forecast to grow at 37.3% annually over the next three years, outpacing the Hong Kong market's 12.5%. Despite lower profit margins this year compared to last, Shoucheng's share repurchase program aims to enhance net assets and earnings per share, potentially benefiting shareholders in the long term.

- Our comprehensive growth report raises the possibility that Shoucheng Holdings is poised for substantial financial growth.

- Unlock comprehensive insights into our analysis of Shoucheng Holdings stock in this financial health report.

Round One (TSE:4680)

Overview: Round One Corporation operates indoor leisure complex facilities and has a market cap of ¥341.34 billion.

Operations: The company's revenue segments include amusement facilities generating ¥75,000 million, bowling alleys contributing ¥40,000 million, and karaoke services bringing in ¥25,000 million.

Estimated Discount To Fair Value: 16.1%

Round One Corporation, trading at ¥1,298.50, is valued below its estimated future cash flow value of ¥1,548.57, suggesting it may be undervalued based on cash flows. Recent sales data shows a steady increase in revenue with June 2026 sales reaching JPY 8.84 billion and year-to-date sales at JPY 28.55 billion. Earnings have grown significantly over the past five years and are forecast to continue outpacing the Japanese market's growth rate.

- Our expertly prepared growth report on Round One implies its future financial outlook may be stronger than recent results.

- Get an in-depth perspective on Round One's balance sheet by reading our health report here.

C Sun Mfg (TWSE:2467)

Overview: C Sun Mfg Ltd., along with its subsidiaries, supplies diverse processing equipment in Taiwan, China, and internationally, with a market cap of NT$87.15 billion.

Operations: The company's revenue is primarily derived from Csun Industrial (NT$4.18 billion), Suzhou Top Creation Machines Co Ltd. (NT$2.19 billion), and C Sun Manufacturing LTD (NT$1.17 billion).

Estimated Discount To Fair Value: 24.8%

C Sun Mfg, trading at NT$589, is priced below its estimated future cash flow value of NT$783.29, indicating potential undervaluation. The company reported strong first-quarter results with sales of TWD 2.26 billion and net income of TWD 466.17 million, significantly higher than the previous year. Earnings are forecast to grow by over 40% annually, outpacing the Taiwan market's growth rate and supporting its undervaluation based on cash flows despite recent share price volatility.

- The growth report we've compiled suggests that C Sun Mfg's future prospects could be on the up.

- Delve into the full analysis health report here for a deeper understanding of C Sun Mfg.

Key Takeaways

- Reveal the 190 hidden gems among our Undervalued Asian Stocks Based On Cash Flows screener with a single click here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com