Top Middle Eastern Dividend Stocks For July 2026

As geopolitical tensions between the U.S. and Iran escalate, most Gulf markets have remained subdued, with investors closely monitoring developments that affect regional stability and economic prospects. Amidst this backdrop, dividend stocks can offer a measure of stability and income for investors seeking to navigate uncertain market conditions.

Top 10 Dividend Stocks In The Middle East

| Name | Dividend Yield | Dividend Rating |

| Yeni Gimat Gayrimenkul Yatirim Ortakligi (IBSE:YGGYO) | 3.19% | ★★★★★★ |

| Turkiye Garanti Bankasi (IBSE:GARAN) | 3.41% | ★★★★★☆ |

| Saudi Awwal Bank (SASE:1060) | 6.24% | ★★★★★☆ |

| National General Insurance (P.J.S.C.) (DFM:NGI) | 7.92% | ★★★★★☆ |

| Matrix IT (TASE:MTRX) | 3.98% | ★★★★★☆ |

| Emirates Insurance Company P.J.S.C (ADX:EIC) | 7.41% | ★★★★★★ |

| Emaar Properties PJSC (DFM:EMAAR) | 8.67% | ★★★★★☆ |

| Dubai Insurance Company (P.S.C.) (DFM:DIN) | 5.88% | ★★★★★☆ |

| Arab National Bank (SASE:1080) | 6.32% | ★★★★★☆ |

| Anadolu Hayat Emeklilik Anonim Sirketi (IBSE:ANHYT) | 8.33% | ★★★★★☆ |

Click here to see the full list of 68 stocks from our Top Middle Eastern Dividend Stocks screener.

Underneath we present a selection of stocks filtered out by our screen.

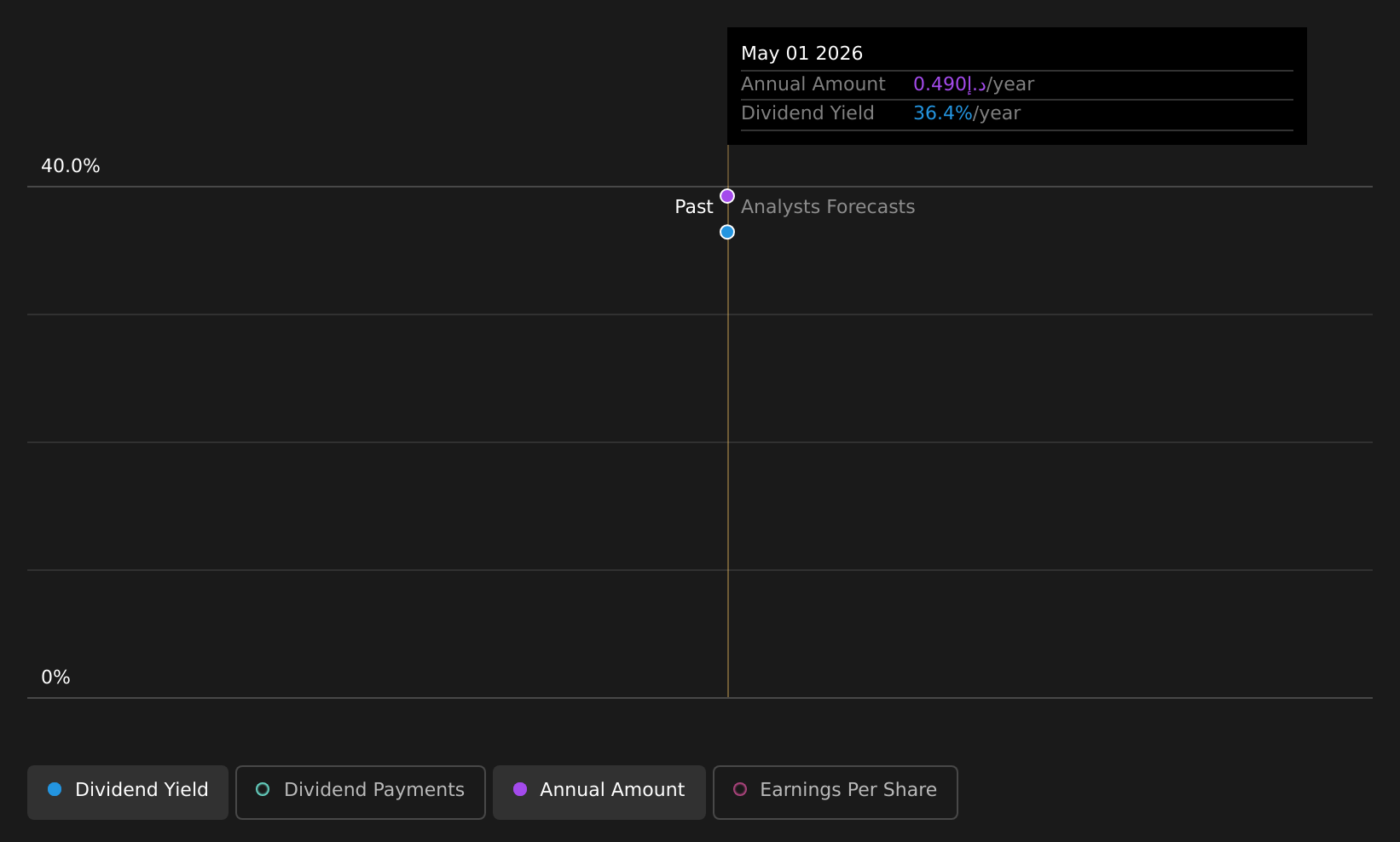

Amlak Finance PJSC (DFM:AMLAK)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Amlak Finance PJSC, along with its subsidiaries, operates in real estate financing and investment activities across the Middle East, with a market capitalization of AED1.82 billion.

Operations: Amlak Finance PJSC generates revenue through its segments, with AED82.95 million from Real Estate Finance, AED3.03 billion from Real Estate Investment, and AED0.73 million from Corporate Finance Investment.

Dividend Yield: 40.5%

Amlak Finance PJSC recently started paying dividends, with a high yield of 40.5%, placing it in the top 25% of dividend payers in the AE market. The company's dividends are well covered by earnings and cash flows, with payout ratios of 49.9% and 25.3%, respectively. Despite its volatile share price, Amlak's profitability has improved significantly this year, supporting its dividend sustainability amid strategic discussions for future growth.

- Get an in-depth perspective on Amlak Finance PJSC's performance by reading our dividend report here.

- In light of our recent valuation report, it seems possible that Amlak Finance PJSC is trading beyond its estimated value.

Çelebi Hava Servisi (IBSE:CLEBI)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Çelebi Hava Servisi A.S. offers ground handling and cargo warehouse services to both domestic and international airlines, as well as private air cargo companies in Turkey, with a market cap of TRY37.30 billion.

Operations: Çelebi Hava Servisi A.S. generates revenue primarily through its Airport Ground Services, including ground handling services, amounting to TRY14.54 billion, and Cargo and Warehouse Services, contributing TRY6.41 billion.

Dividend Yield: 6.7%

Çelebi Hava Servisi's dividend yield of 6.71% ranks it among the top 25% in Turkey, yet its sustainability is questionable due to a high cash payout ratio of 269.4%, indicating dividends aren't well covered by free cash flow despite a reasonable earnings payout ratio of 71.1%. The company's dividends have been volatile over the past decade, though they have shown growth. Recent earnings reports revealed significant sales growth but a sharp decline in net income and EPS.

- Dive into the specifics of Çelebi Hava Servisi here with our thorough dividend report.

- According our valuation report, there's an indication that Çelebi Hava Servisi's share price might be on the expensive side.

Tofas Türk Otomobil Fabrikasi Anonim Sirketi (IBSE:TOASO)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Tofas Türk Otomobil Fabrikasi Anonim Sirketi manufactures, exports, and sells passenger cars and light commercial vehicles in Turkey, with a market cap of TRY147.50 billion.

Operations: Tofas Türk Otomobil Fabrikasi Anonim Sirketi generates revenue through two main segments: Consumer Financing, which accounts for TRY14.97 billion, and Trading of Spare Parts and Automobile, contributing TRY382.85 billion.

Dividend Yield: 6.8%

Tofas Türk Otomobil Fabrikasi's dividend yield of 6.78% places it in the top 25% of Turkish dividend payers, but sustainability concerns arise as dividends aren't covered by free cash flows and exhibit volatility over the past decade. Despite a reasonable payout ratio of 86.8%, earnings have grown significantly, with recent results showing TRY 2.99 billion net income for Q1 2026 after a previous loss, indicating potential for improved financial stability.

- Click here and access our complete dividend analysis report to understand the dynamics of Tofas Türk Otomobil Fabrikasi Anonim Sirketi.

- The valuation report we've compiled suggests that Tofas Türk Otomobil Fabrikasi Anonim Sirketi's current price could be quite moderate.

Make It Happen

- Gain an insight into the universe of 68 Top Middle Eastern Dividend Stocks by clicking here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com