Norfolk Southern (NSC) Could Be 2% Undervalued On Q2 Earnings Watch

Investors Brace For Q2 Earnings And Fuel Cost Headwinds

Norfolk Southern (NSC) is back in focus as investors look ahead to its second quarter 2026 earnings report on July 23, following earlier warnings that higher fuel costs could continue to pressure profitability.

See our latest analysis for Norfolk Southern.

Norfolk Southern shares last closed at US$326.83, with a 30 day share price return of 4.12% and a 90 day share price return of 9.78%. The 1 year total shareholder return of 28.29% and 3 year total shareholder return of 48.39% point to momentum that has been building ahead of the upcoming earnings update and earlier commentary on fuel related cost pressure.

If the upcoming results have you thinking more broadly about transport exposed opportunities, this could be a good moment to widen your search with the 34 power grid technology and infrastructure stocks

With Norfolk Southern stock up solidly over the past year yet still trading close to analyst targets and facing fuel cost pressure, should you be patient for a better entry or lean in at today’s valuation starting point?

Most Popular Narrative: 2% Undervalued

The most followed narrative puts Norfolk Southern's fair value at about $333 per share, only slightly above the recent $326.83 close, which keeps expectations grounded ahead of earnings.

The analysts have a consensus price target of $333.35 for Norfolk Southern based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $378.0, and the most bearish reporting a price target of $297.0.

Want to see what sits underneath that fair value call? Revenue projections, margin recovery and a future earnings multiple all have to line up in a specific way. The interesting part is how those pieces interact over time.

Result: Fair Value of $333 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Norfolk Southern's story can change quickly if storm restoration costs rise or if weaker export coal pricing starts to weigh more heavily on revenue and margins.

Find out about the key risks to this Norfolk Southern narrative.

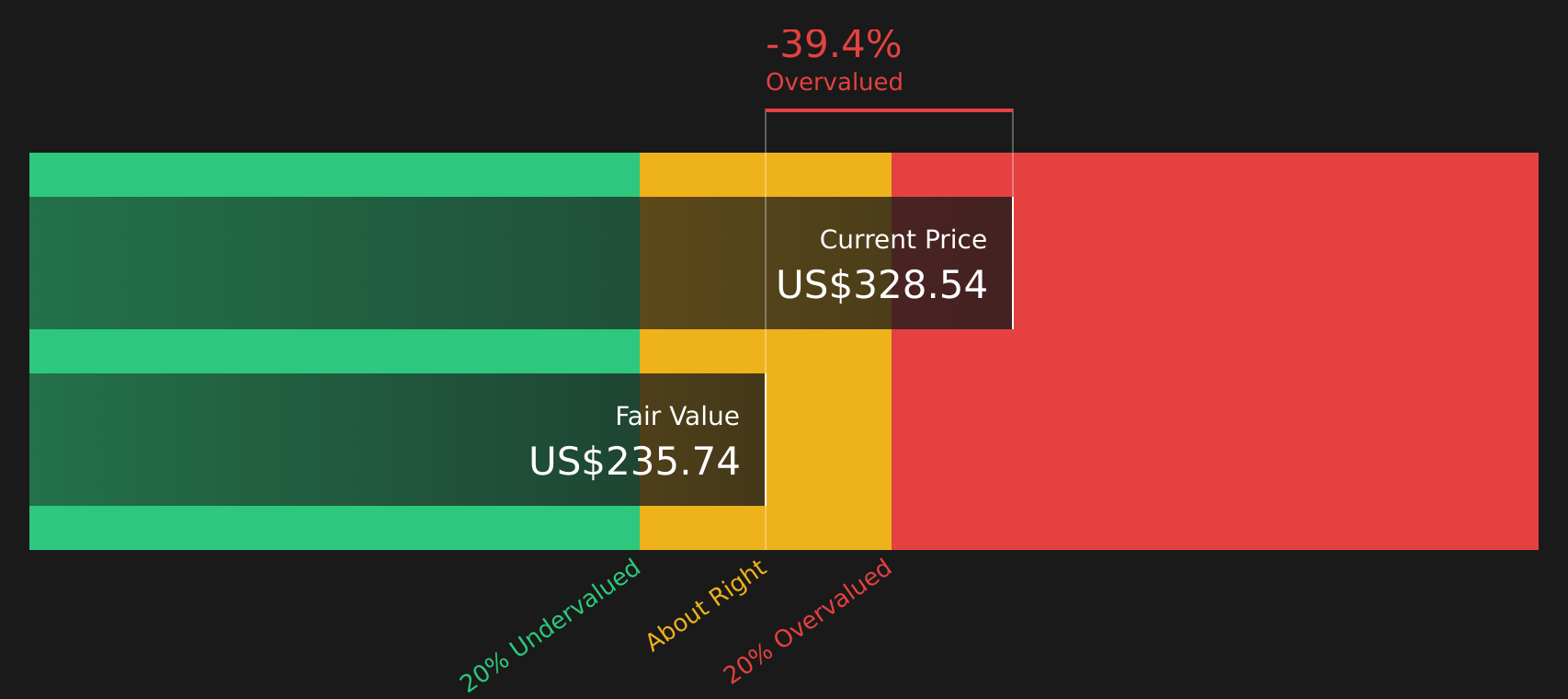

Another View On Norfolk Southern’s Valuation

While the analyst narrative suggests Norfolk Southern is about 2% undervalued around a fair value of roughly $333 per share, the SWS DCF model presents a different perspective. On that view, NSC at $326.83 is above an estimated future cash flow value of $235.77, indicating the stock may be overvalued on this metric. Which perspective do you think aligns better with your expectations for cash generation and risk?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Norfolk Southern for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the mix of fuel cost risks and valuation debates around Norfolk Southern leaves you undecided, this is the time to weigh the trade offs yourself with the 3 key rewards and 1 important warning sign

Looking For More Investment Ideas Beyond Norfolk Southern?

If the Norfolk Southern story has you thinking bigger about your portfolio, do not stop here. Fresh ideas can quickly reshape how you see the rest of your watchlist.

- Expand your hunt for quality by scanning a curated set of companies with strong finances using the solid balance sheet and fundamentals stocks screener (48 results)

- Target potential value opportunities by reviewing the 44 high quality undervalued stocks that currently pass strict quality and pricing filters.

- Uncover lesser known opportunities before they go mainstream by checking the screener containing 20 high quality undiscovered gems that already show solid fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com