Sun Life Financial (TSX:SLF) Joins AI Consortium As Valuation Debate Heats Up

Sun Life Financial (TSX:SLF) joined Lightworks, The Bank of Nova Scotia and TELUS in forming the AI Consortium, a cross industry group focused on shared artificial intelligence infrastructure and governance for heavily regulated sectors.

See our latest analysis for Sun Life Financial.

Sun Life Financial's share price has moved to CA$111.9, with a 1-month share price return of 4.54% and a 90-day share price return of 19.18%, alongside a 1-year total shareholder return of 37.10%. This suggests momentum has been building as the AI Consortium launch and the recent CAD 261.1m shelf registration keep the stock in focus.

If you want to see how other companies are approaching AI infrastructure, it could be a good time to scan the market using our screener for 52 AI infrastructure stocks

After a sharp move to CA$111.9 and a sizable modeled discount to intrinsic value, alongside a premium to analyst targets, is the market being too cautious on Sun Life Financial or already paying up for its AI and growth ambitions?

Most Popular Narrative: 9.9% Overvalued

With Sun Life Financial closing at CA$111.90 compared to a narrative fair value of CA$101.79, the widely followed view sees the stock trading ahead of modeled fundamentals, anchored on detailed assumptions about growth, margins and a required return of 6.35%.

Strong growth across Asian markets, particularly in Individual Protection and wealth products, is expanding Sun Life's addressable market and creating significant new revenue sources; this is reinforced by double-digit sales and CSM growth in the region year-over-year.

Want to see what kind of revenue runway and margin lift justify that fair value gap, and how earnings, share count and future P/E all fit together? The full narrative lays out a tight set of growth, profitability and discount rate assumptions that investors can test against their own expectations.

Result: Fair Value of CA$101.79 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Sun Life Financial's reliance on U.S. Dental earnings and MFS asset management flows means regulatory shifts or prolonged fee pressure could quickly challenge this overvaluation story.

Find out about the key risks to this Sun Life Financial narrative.

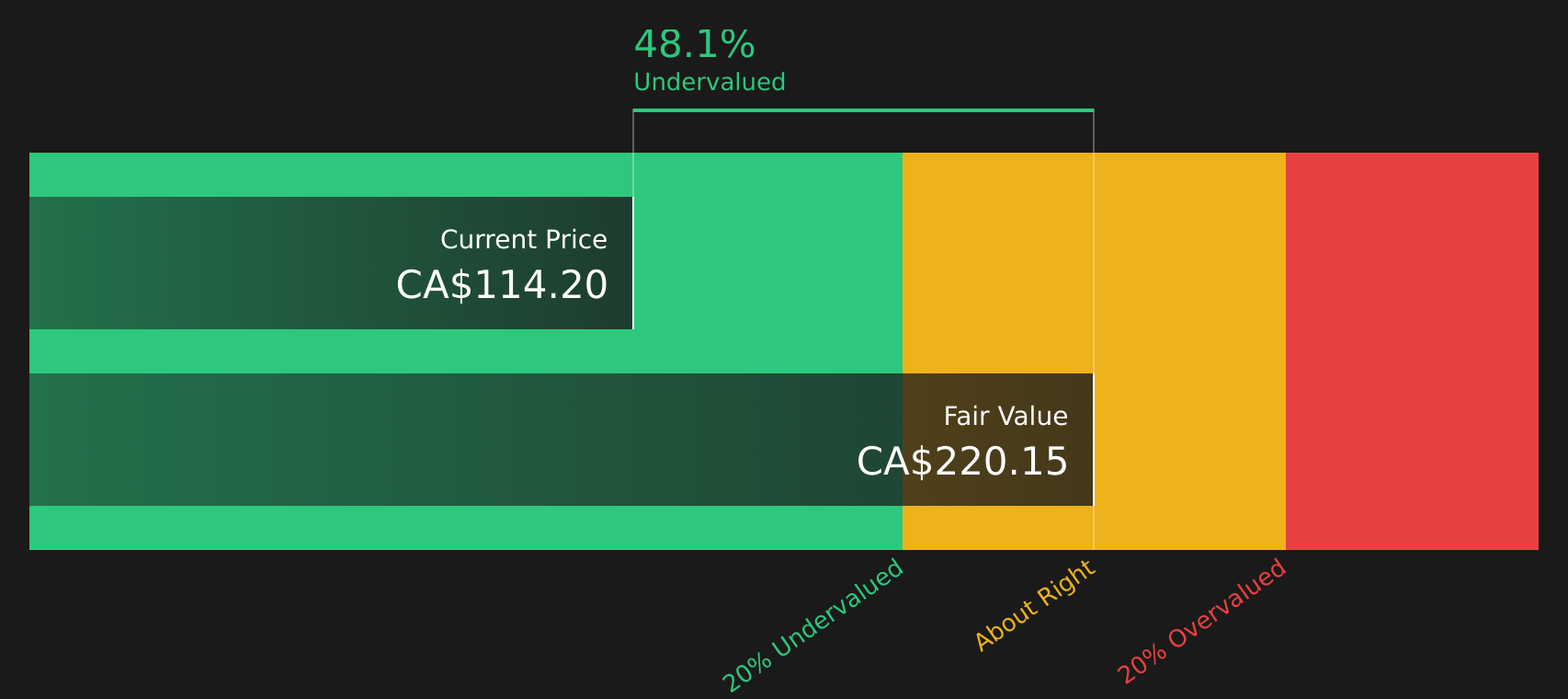

Another View: Cash Flows Tell a Different Story

While the analyst narrative sees Sun Life Financial as about 9.9% overvalued relative to a CA$101.79 fair value, the SWS DCF model points the other way, with an estimate of CA$218.11 per share that frames the current CA$111.90 price as trading at a substantial discount. Which story do you think better fits your own expectations for the business?

To see how the SWS DCF model ties Sun Life Financial's current price to its modeled cash flows, take a closer look at the full calculation and its assumptions in our valuation breakdown, then decide how comfortable you are with those inputs yourself. Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Sun Life Financial for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 5 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With all this mixed sentiment around Sun Life Financial, do you feel the market is too optimistic or too cautious? Act while the data is fresh and form your own view by checking the 3 key rewards.

Looking for more investment ideas beyond Sun Life Financial?

If Sun Life Financial has sharpened your focus, do not stop here. Broaden your watchlist now or you risk missing opportunities sitting in plain sight.

- Spot potential bargains early by scanning companies that look mispriced on quality and value metrics through the 5 high quality undervalued stocks.

- Strengthen your income stream by reviewing stocks that offer robust yields and resilience using the 6 dividend fortresses.

- Prioritise stability by checking companies that score well on balance sheet strength and fundamentals with the solid balance sheet and fundamentals stocks screener (12 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com