HNI (HNI) Stock May Still Be Below Fair Value On Sales

HNI stock has delivered a solid 54.9% gain over the past three years, yet the current valuation checks and recent share price at US$39.69 still point to a company that screens as undervalued rather than fully priced in.

- HNI is up 54.9% over three years, which suggests the stock has already rewarded patient holders while still leaving the question of how much value is left on the table.

- Future revenue and cash flow expectations can support the current share price, but any pressure on margins or balance sheet flexibility may cap how much investors are willing to pay for that growth.

- HNI scores highly on the broader valuation checks, with the stock looking undervalued on 6 of 6 measures according to our valuation framework, which suggests the current market price may not fully reflect its fundamentals.

The stock's next move may depend on whether that high valuation score and past three year return are already fully reflected in HNI's share price or still leave room for further upside.

Find out why HNI's -18.6% return over the last year is lagging behind its peers.

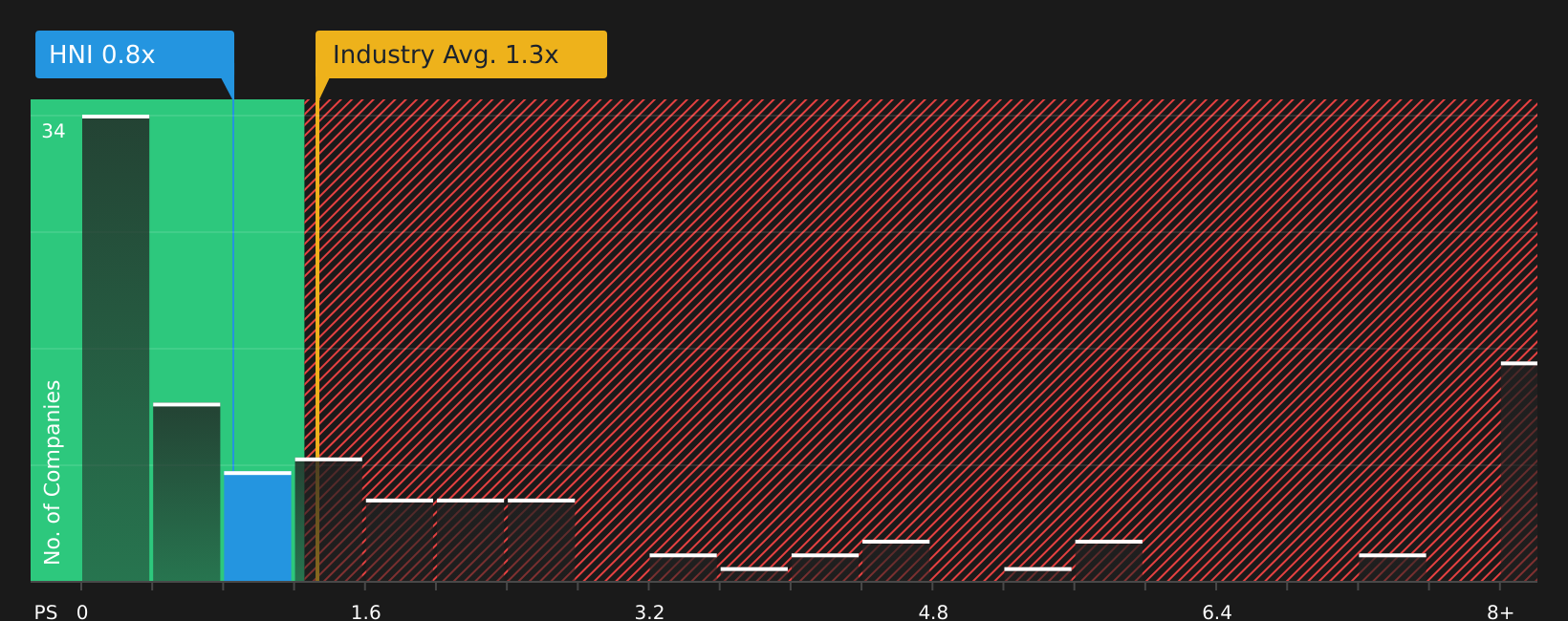

Is HNI Still Cheap on Sales?

P/S is a useful check for HNI because it links the current share price directly to the revenue the business is already generating. On this measure, HNI trades on a P/S of about 0.8x, which is below both the Commercial Services industry average of 1.3x and the peer average of around 1.6x.

The valuation framework also suggests a fair P/S ratio of roughly 3.1x for HNI, based on its characteristics and risk profile. Set against the current 0.8x, this indicates the stock is pricing in much less value per dollar of sales than the model would expect, even after the solid share price performance over the past three years.

On the P/S multiple, HNI currently appears undervalued, with the market assigning a lower value to its revenue base than both peers and the tailored fair ratio indicate.

See what the numbers say about this price — find out in our valuation breakdown.

The HNI Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for HNI pick up where this valuation puzzle leaves off by spelling out what would need to be true about HNI's future growth, margins and earnings for the stock to end up worth meaningfully more or less than today's price. Each one treats HNI's fair value as a thesis about the business that can be revisited over time rather than a one off snapshot, and they sit on Simply Wall St's Community page.

You can add your voice to the Simply Wall St community by sharing a Narrative on HNI that lays out a number driven view of where its growth, margins and execution go from here. Set out your thesis, track how it holds up as new results come through, and see how other investors respond to your case on HNI's stock.

Do you think there's more to the story for HNI? Head over to our Community to see what others are saying!

The Bottom Line

For HNI, the key takeaway is that market multiples still point to an undervalued stock, even after a meaningful three year return. The main question is whether that discount reflects lingering caution about margins and balance sheet flexibility, or simply a lag in how the market is pricing its revenue base. The central consideration for investors from here is whether HNI can sustain and convert its revenue into resilient profitability, which could support a higher multiple, or whether the current discount proves to be a fair reflection of ongoing risks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com