3 Japanese Tech Stocks With Strong Earnings That May Still Be Undervalued

With inflation pressures, higher bond yields and geopolitical tension pulling markets in different directions, many investors are looking for solid businesses that can handle shocks without relying on rosy growth stories. That is where the High Quality Undervalued Stocks screener comes in. It focuses on companies with healthy cash flows and robust balance sheets that the market has not fully priced, providing exposure to what can be described as hidden engines of wealth. In this article, you will see 3 of the stocks from this screener that stand out in the current macro backdrop.

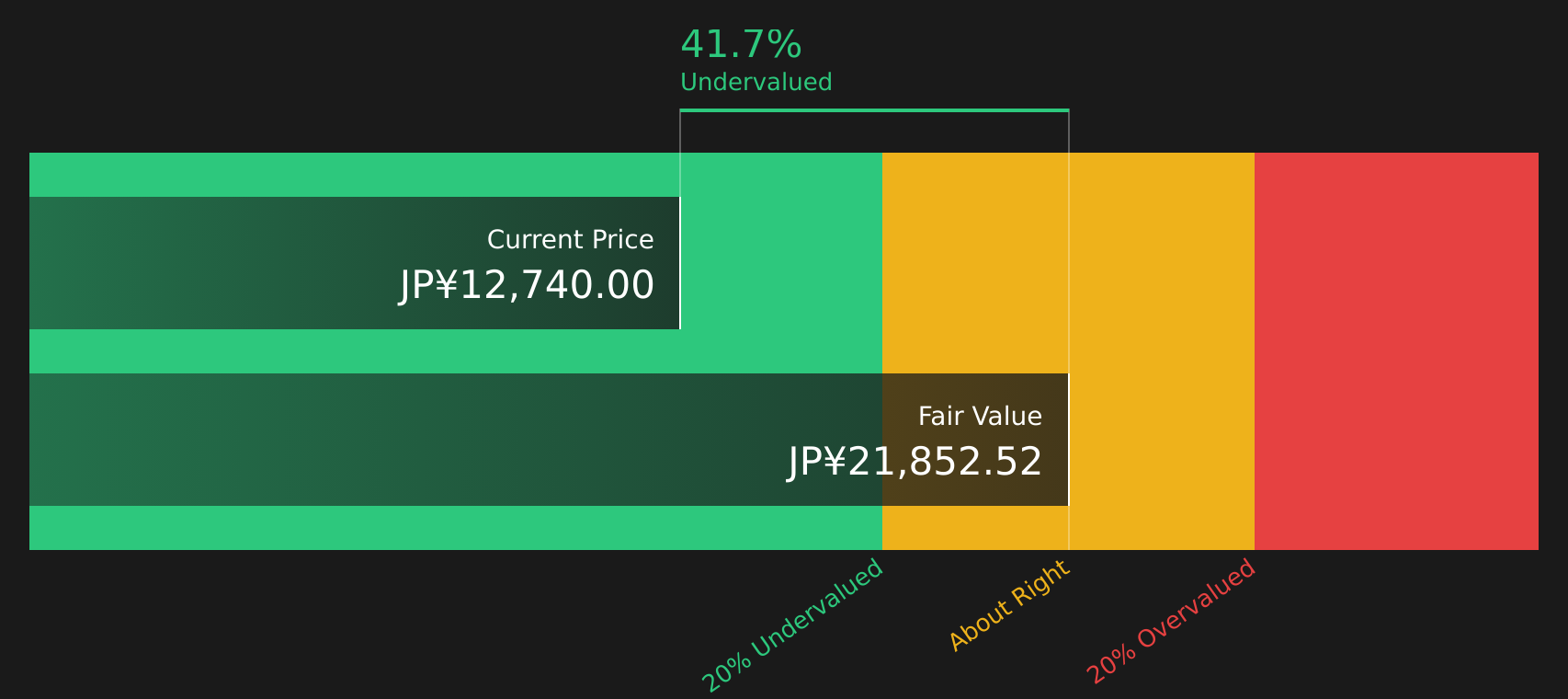

Recruit Holdings (TSE:6098)

Overview: Recruit Holdings is a Tokyo based HR and marketing solutions group that connects job seekers, employers and consumers through platforms such as online hiring tools, global staffing services and lifestyle and real estate marketplaces.

Operations: Recruit Holdings generates most of its revenue from Staffing at ¥1.70t and HR Technology at ¥1.46t, with Marketing Matching Technologies contributing ¥564.7b and a small unallocated adjustment.

Market Cap: ¥17.59t

Recruit Holdings stands out on this screener because it combines earnings quality, high profitability and investment in automation and AI services with a share price that is estimated to trade well below fair value. The business is leaning into higher margin HR technology and data led platforms, while its global staffing footprint and marketing marketplaces help diversify cash flows. At the same time, investors need to weigh weaker labor demand in key markets, reliance on external funding and a relatively high P/E against the broader outlook and active buybacks. The full story here, including how analysts are framing the potential upside versus these pressures, is one area of focus for long term holders.

Recruit Holdings’ push into higher margin HR technology and AI services could be masking a bigger story about how the market is pricing its cash flows and risk profile, so it is worth reading the 3 key rewards and 1 important warning sign

Simplex Holdings (TSE:4373)

Overview: Simplex Holdings is a Tokyo based IT solutions company that helps Japanese businesses plan and execute digital transformation, from high level management and business strategy through to system design, development, and long term operation, often delivered via software as a service.

Operations: Simplex Holdings generates all of its revenue from IT Solutions in Japan, with ¥58.7b in sales.

Market Cap: ¥233.71b

Simplex Holdings combines high quality earnings with solid growth in a single focused IT platform. This may appeal if you want exposure to Japan’s digital transformation trend without a sprawling conglomerate structure. Earnings grew faster than both the wider IT industry and the broader market, profit margins sit at 18%, and return on equity is already strong. At the same time, reliance on external borrowing and a reduced year end dividend remind investors to watch the balance between growth ambitions and capital returns.

Simplex Holdings’ earnings growth, 18% margins and focused Japan IT platform may hint at a bigger story hiding in plain sight, so it is worth reading the analyst forecasts for Simplex Holdings to see what could change next.

Shibaura Mechatronics (TSE:6590)

Overview: Shibaura Mechatronics is a Yokohama based manufacturer of production equipment used in flat panel displays, semiconductors and electronic components, alongside vending machines and a smaller real estate leasing business, serving customers in Japan, Northeastern Asia and globally.

Operations: Shibaura Mechatronics generates most of its revenue from Fine Mechatronics at ¥52,246m and Mechatronics Systems at ¥32,270m, with smaller contributions from Distribution Equipment Systems at ¥2,595m and Real Estate Rental at ¥1,952m, partly offset by ¥1,026m of internal segment eliminations.

Market Cap: ¥355.76b

Shibaura Mechatronics may be relevant if you are looking for exposure to the semiconductor and display equipment supply chain supported by the company’s reported fundamentals. Reported earnings growth has been strong over 5 years, analysts currently expect earnings and revenue to grow at double digit rates, and the latest reported ROE of 20.1% reflects the company’s use of shareholder capital. At the same time, third party assessments indicate the stock is trading below some estimates of fair value even with a relatively high P/E, and the board is signaling a focus on shareholder returns with a year end dividend and a payout ratio around 35%. On the risk side, investors should be aware of higher share price volatility and reliance on external borrowing, which may make the overall balance between risk and potential reward worth closer individual consideration.

Shibaura Mechatronics’ double digit growth outlook and 20.1% ROE suggest a story that may not be fully reflected in the share price. However, the real twist sits inside the analyst forecasts for Shibaura Mechatronics

The three stocks covered here are just a preview of what this idea can offer, with the full High Quality Undervalued Stocks screener surfacing 16 more companies that pair strong cash flows and solid balance sheets with equally compelling narratives. To identify the highest conviction setups, use Simply Wall St to filter the High Quality Undervalued Stocks screener by the specific catalysts and storylines that matter to you. Then analyze which combinations of quality, valuation and potential breakout triggers best fit your own playbook.

Take Control of Your Investment Journey

If Recruit Holdings or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond These Picks?

Fresh ideas are often spotted early, before momentum builds and prices start rising. Use these under the radar lists while it matters, before the crowd arrives.

- Spot potential breakout miners by scanning the 33 elite gold producer stocks and see which producers still trade as if the last commodity cycle never happened.

- Track the AI build out from a different angle by reviewing the 52 AI infrastructure stocks fueling data centers, power demand and next generation computing capacity.

- Zero in on power grid upgrades using the curated 34 power grid technology and infrastructure stocks to find companies positioned around aging infrastructure and rising electrification needs.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com