Exploring 3 Undervalued Small Caps In The European Market With Insider Activity

The European market has recently faced challenges, with the pan-European STOXX Europe 600 Index declining by 1.79% amid geopolitical tensions and concerns over inflation and monetary policy adjustments. Despite these headwinds, small-cap stocks in Europe present intriguing opportunities for investors, particularly those with notable insider activity that may signal potential value. Identifying promising small-cap stocks often involves looking at companies with strong fundamentals and growth prospects that can navigate the current economic landscape effectively.

Top 10 Undervalued Small Caps With Insider Buying In Europe

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| CellaVision | 23.9x | 4.4x | 45.13% | ★★★★★★ |

| Ratos | NA | 0.6x | 38.88% | ★★★★★★ |

| Eurocell | 11.3x | 0.3x | 48.87% | ★★★★★☆ |

| Nederman Holding | 17.2x | 0.8x | 36.05% | ★★★★★☆ |

| Stelrad Group | 233.9x | 0.7x | 32.33% | ★★★★☆☆ |

| Bilia | 16.2x | 0.3x | 40.57% | ★★★★☆☆ |

| NoHo Partners Oyj | 16.7x | 0.4x | 34.43% | ★★★★☆☆ |

| Troax Group | 52.8x | 2.0x | 48.72% | ★★★☆☆☆ |

| Kempower Oyj | NA | 2.4x | 39.85% | ★★★☆☆☆ |

| CVS Group | 52.7x | 1.3x | 47.11% | ★★★☆☆☆ |

Let's uncover some gems from our specialized screener.

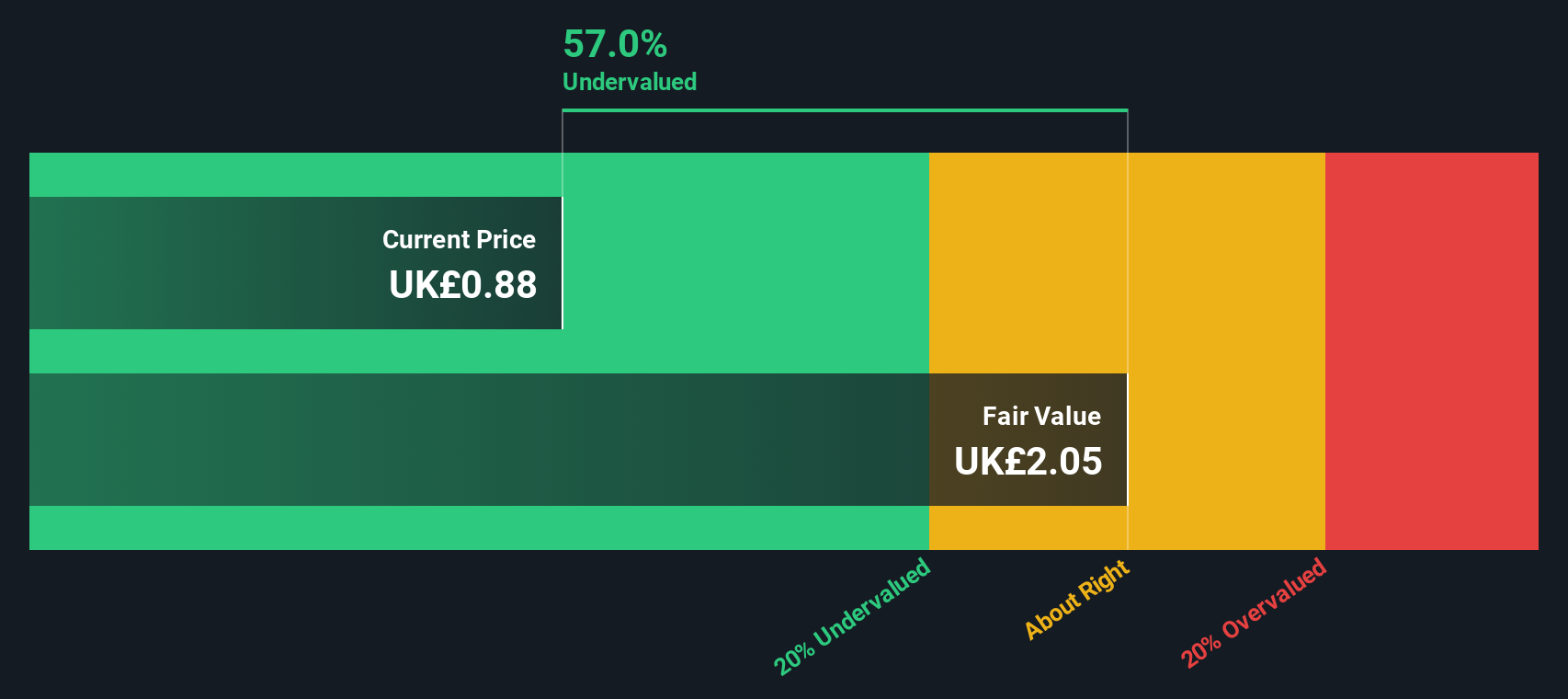

Card Factory (LSE:CARD)

Simply Wall St Value Rating: ★★★★★☆

Overview: Card Factory is a retailer specializing in greeting cards, gifts, and party supplies with operations including physical stores, digital sales, and wholesale partnerships; it has a market capitalization of approximately £0.84 billion.

Operations: Cardfactory generates revenue primarily from its stores, which contribute significantly to its total income, followed by wholesale partnerships and digital sales. The company's gross profit margin has shown variability over the years, with a recent figure of 36.24%. Operating expenses have been a substantial component of costs, impacting net income outcomes.

PE: 7.6x

Card Factory, a smaller player in Europe's market, reported sales of £582.7 million for the year ending January 31, 2026, up from £542.5 million previously. Despite this growth, net income dipped to £31.2 million from last year's £47.8 million due to slimmer profit margins at 5.4%. Insider confidence is evident with recent share purchases by executives within the past six months. The company relies entirely on external borrowing for funding, which carries higher risk but suggests potential growth opportunities as earnings are projected to rise by 11% annually.

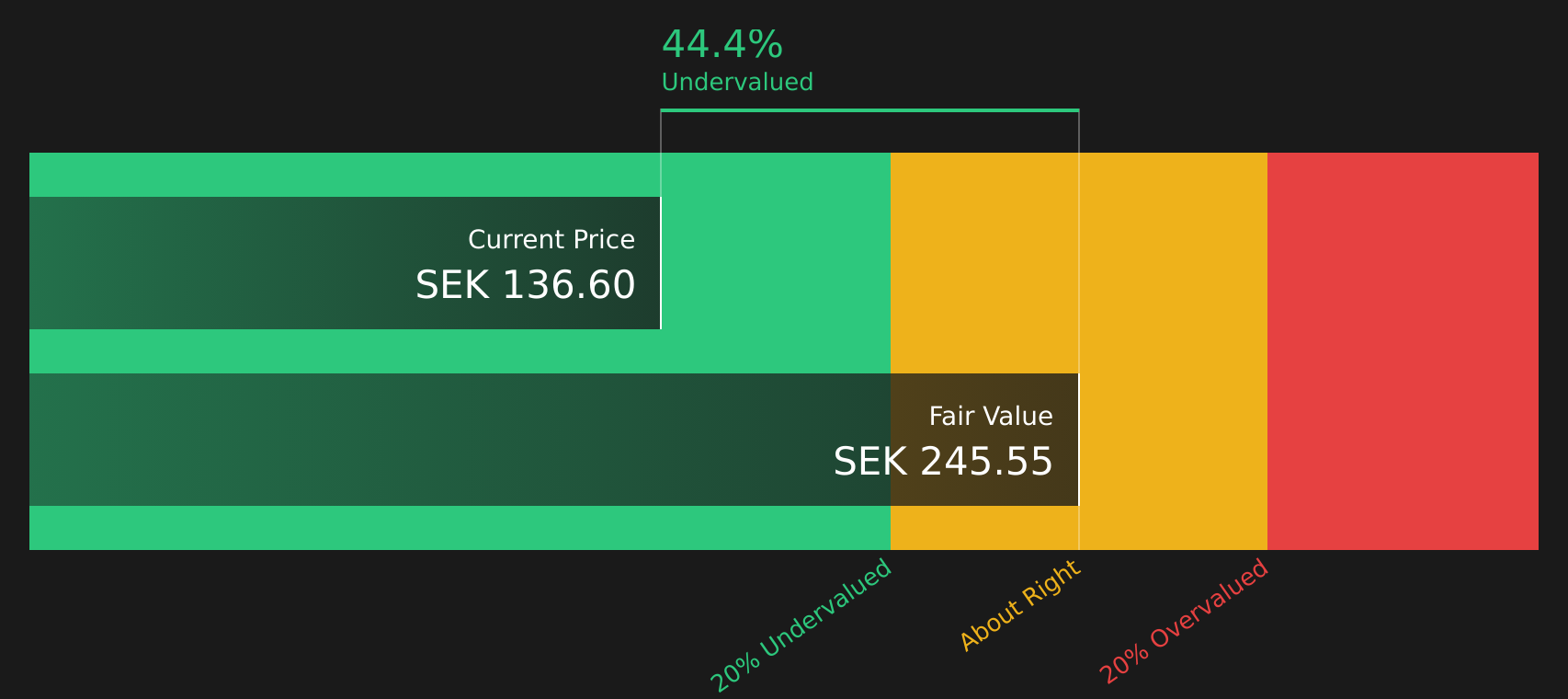

CellaVision (OM:CEVI)

Simply Wall St Value Rating: ★★★★★★

Overview: CellaVision specializes in developing and selling automated microscopy systems and reagents for hematology, with a market cap of approximately SEK 8.54 billion.

Operations: The company generates revenue primarily from its Automated Microscopy Systems and Reagents in the field of hematology, with a recent quarterly revenue of SEK 730.59 million. Over the periods analyzed, the gross profit margin fluctuated between approximately 66% and 75%. Operating expenses are significant, including sales & marketing and R&D expenses, impacting net income margins which have varied from around 16% to over 25%.

PE: 23.9x

CellaVision, a player in the medical technology sector, recently appointed Steve Ferguson as CEO. Ferguson's extensive biotech background could steer growth amidst challenges like declining Q1 2026 earnings, with sales dropping to SEK 166.43 million from SEK 194.8 million year-over-year. Despite this, insider confidence is evident; Christer Fahraeus acquired 250,000 shares worth approximately SEK 31.5 million in April 2026, boosting their stake by over 15%. While reliant on external borrowing for funding, projected annual earnings growth of over 17% suggests potential upside.

- Click here and access our complete valuation analysis report to understand the dynamics of CellaVision.

Assess CellaVision's past performance with our detailed historical performance reports.

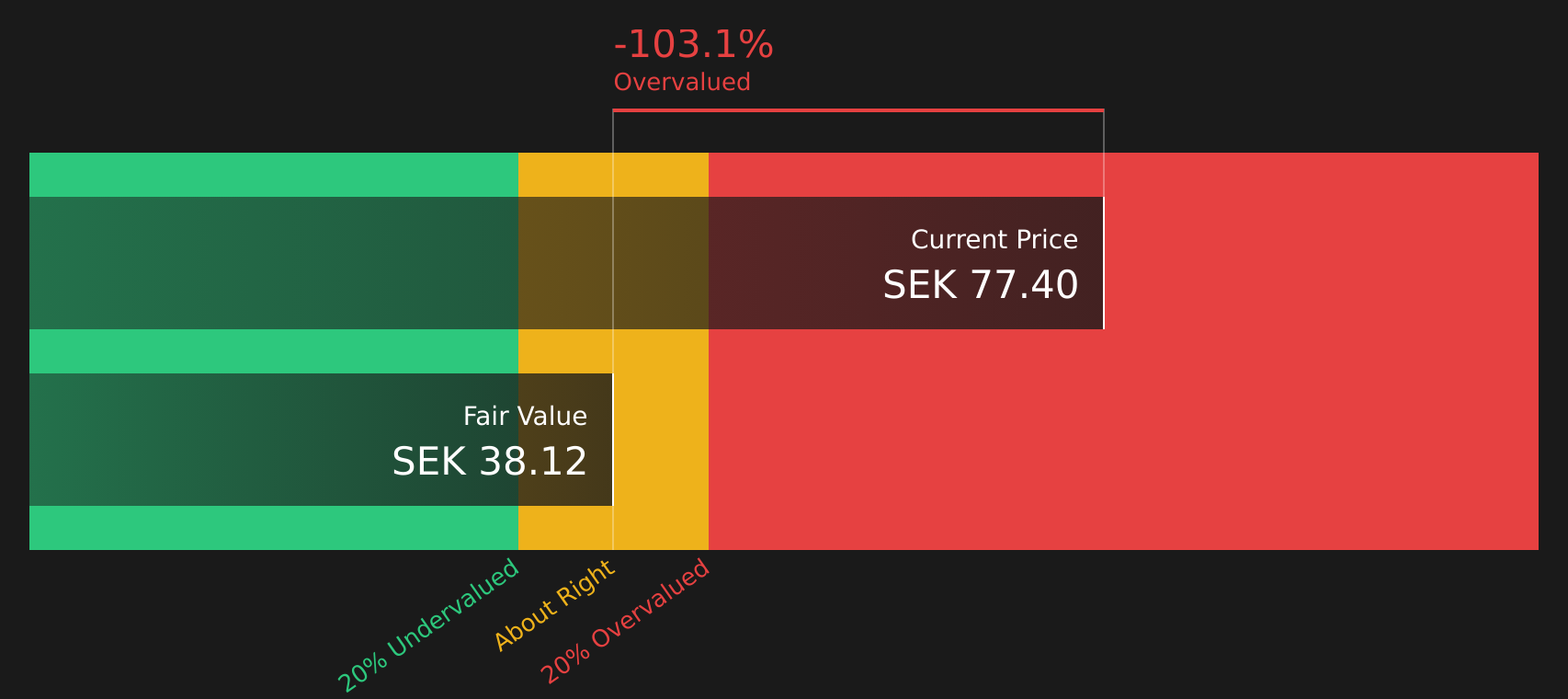

Duni (OM:DUNI)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Duni is a company that designs, produces, and sells sustainable table setting and take-away solutions primarily for the restaurant and catering industries, with a market capitalization of approximately SEK 4.79 billion.

Operations: Duni's revenue streams have shown growth over the years, reaching SEK 7.78 billion by September 2025. The company's cost of goods sold (COGS) has also increased, amounting to SEK 5.89 billion in the same period. Operating expenses are significant, with sales and marketing being a major component at SEK 790 million in September 2025. Notably, the gross profit margin has seen fluctuations but was at 24.24% by September 2025.

PE: 12.8x

Duni, a European player in sustainable packaging and hospitality solutions, is navigating challenges with logistics disruptions impacting Q2 2026 earnings. Sales dipped to SEK 1,823 million from SEK 1,884 million the previous year, with a net loss of SEK 21 million. Despite these setbacks, insider confidence remains strong as insiders purchased shares in early July 2026. The company is enhancing its eco-friendly product line-up and aims for revenue growth of around 3.53% annually amidst evolving regulatory landscapes.

- Unlock comprehensive insights into our analysis of Duni stock in this valuation report.

Review our historical performance report to gain insights into Duni's's past performance.

Where To Now?

- Click through to start exploring the rest of the 53 Undervalued European Small Caps With Insider Buying now.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com