How Investors Are Reacting To PVH (PVH) Hiring Ex-Sephora Executive Alexis Rollier as CFO

- PVH Corp. has appointed former Sephora executive Alexis Rollier as its new chief financial officer, bringing three decades of global finance and retail experience to oversee its Calvin Klein and Tommy Hilfiger brands from early September 2026.

- This leadership change reshapes the company’s financial leadership bench, with prior CFO Melissa Stone returning to head global financial planning and analysis, potentially sharpening PVH’s focus on execution and long-term capital discipline.

- We’ll now examine how Alexis Rollier’s Sephora and LVMH experience could influence PVH’s investment narrative and future execution priorities.

The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

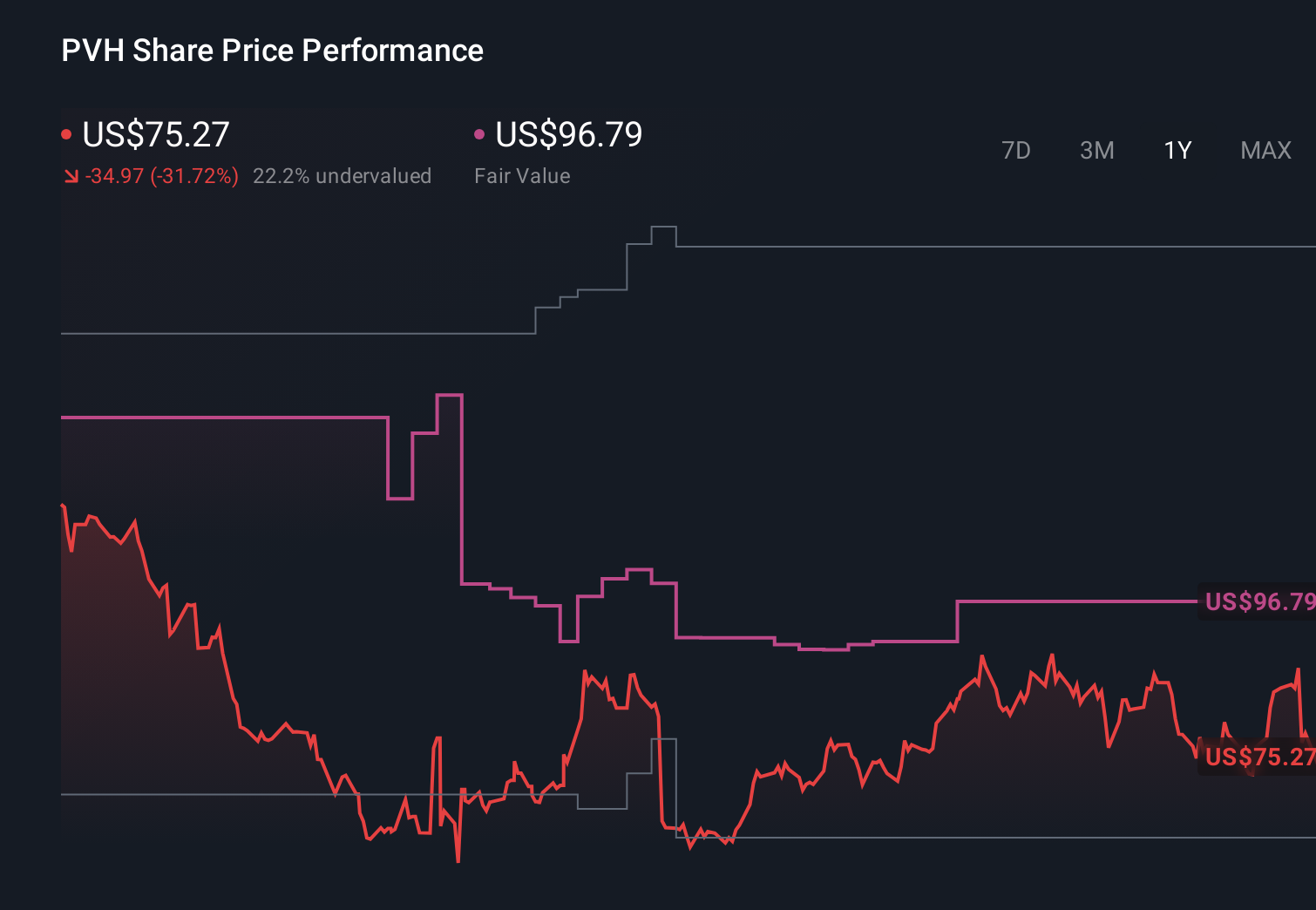

PVH Investment Narrative Recap

To own PVH, you have to believe its PVH+ plan can keep Calvin Klein and Tommy Hilfiger relevant while slowly improving profitability despite flat revenue guidance and tariff headwinds. The CFO change looks incremental in the near term: Alexis Rollier’s background in global retail and beauty may help execution on cost, capital allocation, and digital initiatives, but it does not fundamentally alter the key catalyst of margin improvement or the main risk around trade and geopolitical pressures.

Among recent developments, the June 2026 refinancing stands out alongside the CFO appointment. The new Euro Term Loan A and multicurrency revolving credit facility extend PVH’s debt maturities to 2031 and add flexibility around currencies and leverage covenants. In the context of margin and execution catalysts, this refreshed capital structure, combined with a finance leader steeped in LVMH and Sephora, gives PVH more room to manage through tariff costs, supply chain complexity, and uneven regional demand without near term balance sheet pressure.

Yet, against this refinancing backdrop, the risk that tariff changes and trade policy uncertainty could still weigh on PVH’s margins is something investors should be aware of...

Read the full narrative on PVH (it's free!)

PVH's narrative projects $9.6 billion revenue and $734.4 million earnings by 2029. This requires 2.1% yearly revenue growth and a $576.3 million earnings increase from $158.1 million today.

Uncover how PVH's forecasts yield a $93.08 fair value, a 21% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were expecting PVH to lift earnings to about US$771.1 million by 2029, but this new CFO hire could prompt them to revisit how realistic that margin expansion story really is, so you may want to compare those bullish views with more cautious takes before you decide how much weight to put on them.

Explore 3 other fair value estimates on PVH - why the stock might be worth just $93.08!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your PVH research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free PVH research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate PVH's overall financial health at a glance.

Contemplating Other Strategies?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

- Outshine the giants: these 16 early-stage AI stocks could fund your retirement.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com