Is FactSet’s AI Pact With Google Cloud and Buybacks Altering The Investment Case For FDS?

- In July 2026, FactSet Research Systems Inc. reported third‑quarter fiscal 2026 results showing higher sales of US$622.92 million but lower net income of US$126.72 million versus a year earlier, reaffirmed full‑year revenue and earnings guidance, and completed a US$505.96 million share repurchase program covering 5.55% of its stock.

- FactSet also announced a multi‑faceted AI partnership with Google Cloud aimed at embedding Gemini‑powered agents into its Workstation and expanding cloud infrastructure options for financial‑industry clients.

- We’ll now examine how FactSet’s new Google Cloud AI collaboration could reshape its investment narrative and longer‑term growth drivers.

This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

FactSet Research Systems Investment Narrative Recap

To own FactSet, you need to believe it can keep deepening its role in core investment workflows while managing rising technology spend and pressure on client budgets. The latest quarter showed higher sales but lower earnings, and the Google Cloud AI deal does not materially change the near term risk that elevated cloud and software costs could weigh on margins, even as AI products remain a key short term catalyst.

The most relevant update here is FactSet’s reaffirmed fiscal 2026 guidance, with GAAP revenue still expected between US$2,450 million and US$2,470 million and diluted EPS between US$14.85 and US$15.35. Holding guidance steady after a quarter of softer net income suggests management is prepared to absorb higher tech and AI related spending as it ramps partnerships like Google Cloud, while still aiming to preserve its targeted operating margin range.

Yet beneath the AI opportunity, investors should still be aware of rising cloud and software costs that could...

Read the full narrative on FactSet Research Systems (it's free!)

FactSet Research Systems' narrative projects $2.8 billion revenue and $703.8 million earnings by 2029. This requires 5.4% yearly revenue growth and about a $116 million earnings increase from $587.8 million today.

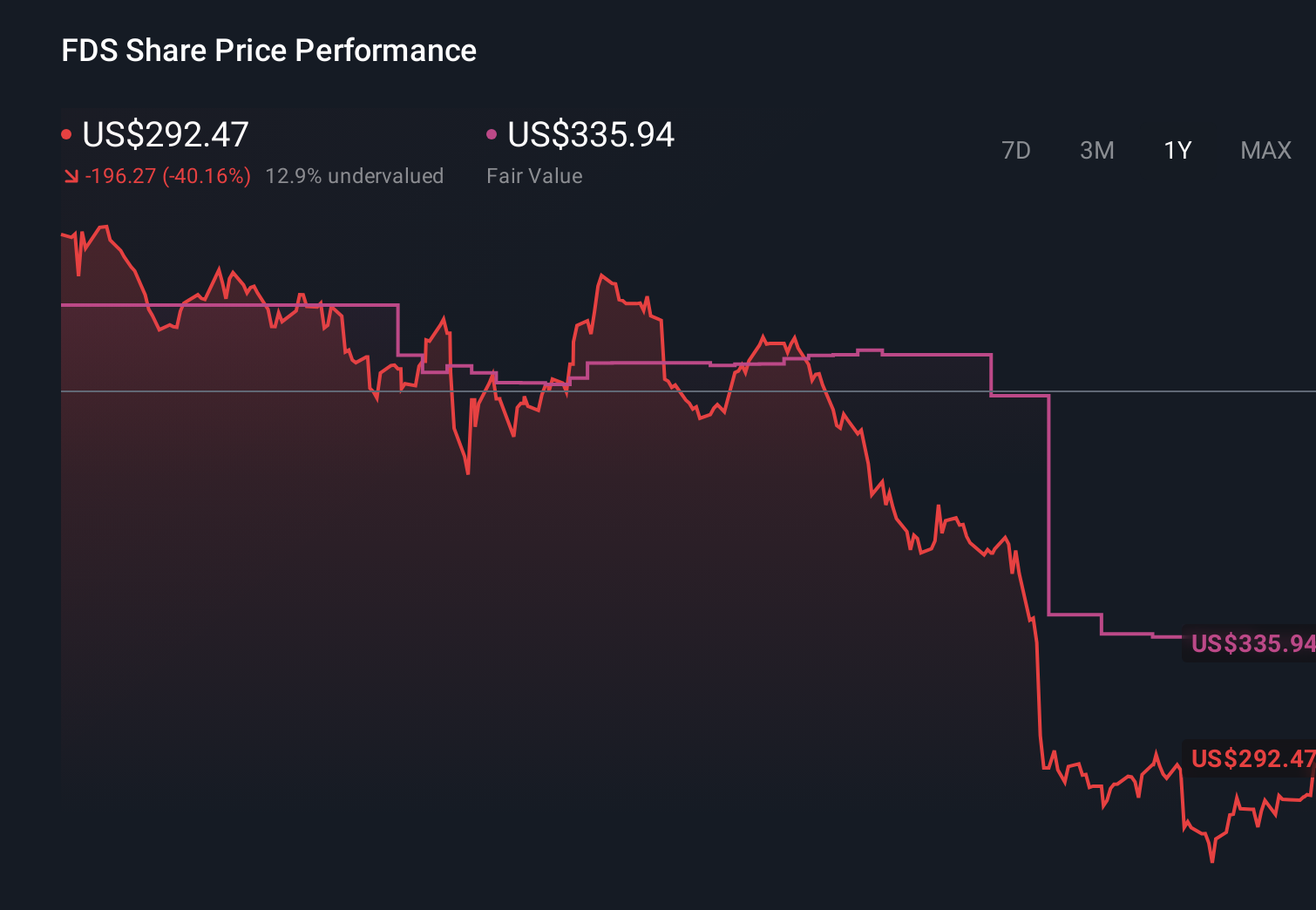

Uncover how FactSet Research Systems' forecasts yield a $247.50 fair value, in line with its current price.

Exploring Other Perspectives

Before this news, the most pessimistic analysts were assuming revenue growth of about 4.5% and earnings of roughly US$666 million by 2028, highlighting how concerns about longer, slower AI infused enterprise sales cycles can differ sharply from the more constructive consensus view on FactSet’s AI rollout.

Explore 6 other fair value estimates on FactSet Research Systems - why the stock might be worth just $247.50!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your FactSet Research Systems research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free FactSet Research Systems research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate FactSet Research Systems' overall financial health at a glance.

Ready For A Different Approach?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 30 companies in the world exploring or producing it. Find the list for free.

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com