Will Atlantic Union (AUB) Q2 2026 Earnings Clarify Its Long-Term Capital Allocation Priorities?

- Atlantic Union Bankshares Corporation is preparing to release its Q2 2026 earnings results on July 21 after the market close, with consensus estimates pointing to US$389.06 million in revenue and earnings per share of US$0.92.

- This earnings update will give investors a fresh read on the bank’s operating performance and capital flexibility as it pursues expansion, digital investments, and balance-sheet repositioning.

- We’ll now examine how the upcoming Q2 earnings release might influence Atlantic Union’s longer-term growth, efficiency, and capital allocation narrative.

Find 46 companies with promising cash flow potential yet trading below their fair value.

Atlantic Union Bankshares Investment Narrative Recap

To own Atlantic Union Bankshares, you have to believe in its ability to turn a Mid Atlantic and Southeast focused branch network, recent acquisitions, and digital upgrades into steady, high quality earnings and dividend support. The upcoming Q2 2026 report, with revenue and EPS expectations of US$389.06 million and US$0.92, looks more like a check in on margin trends and credit costs than a major turning point, so it may not materially change the near term risk that integration and regional concentration could pressure results.

One of the most relevant recent announcements is the new US$250 million share repurchase authorization, which sits alongside a maintained US$0.37 quarterly dividend and gives fresh context for the Q2 earnings release as investors watch how capital is balanced between buybacks, acquisitions, and ongoing investments in digital banking.

Yet for investors, the bigger question is how much integration and regional concentration risk they are really taking on...

Read the full narrative on Atlantic Union Bankshares (it's free!)

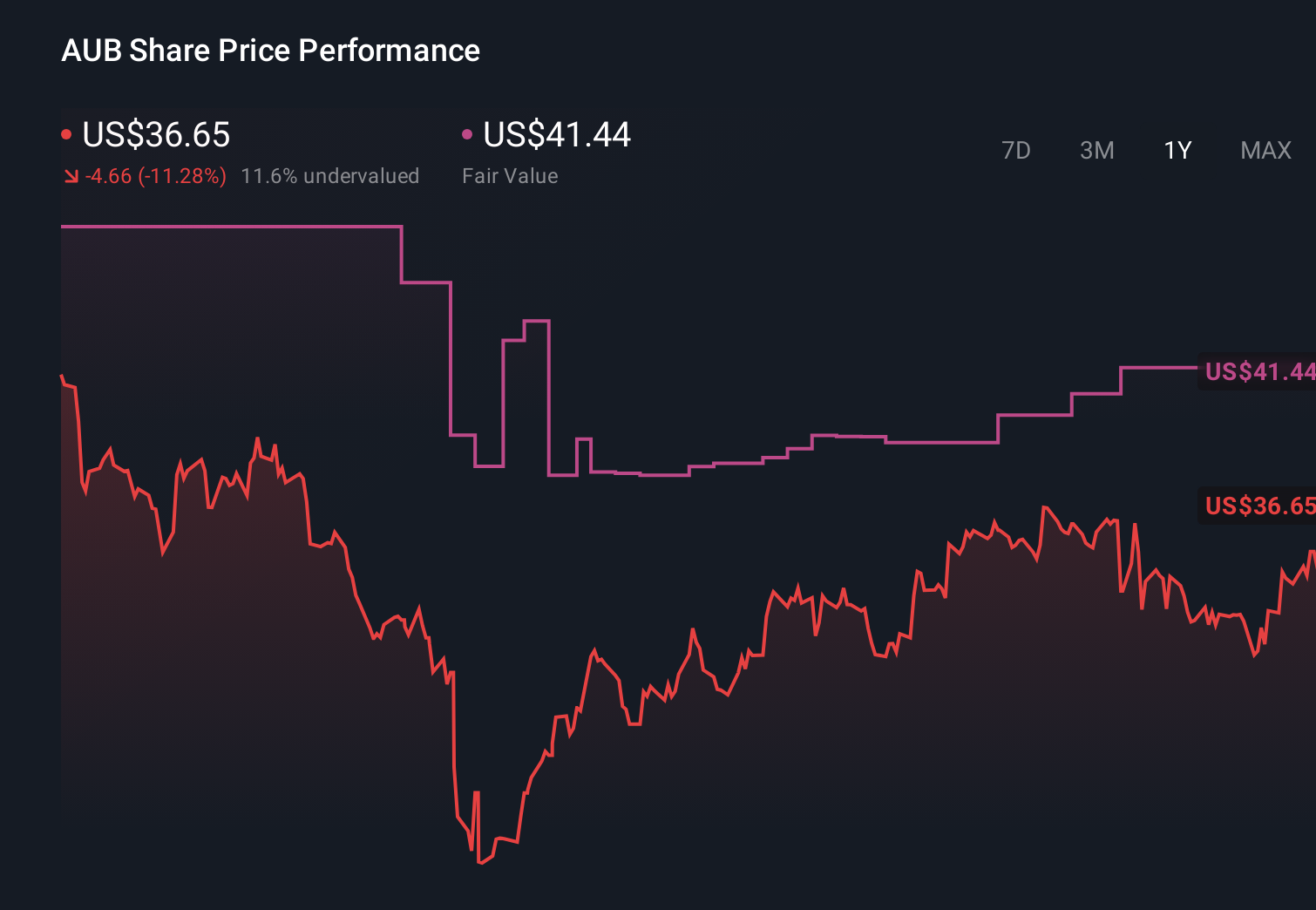

Atlantic Union Bankshares' narrative projects $1.8 billion revenue and $699.9 million earnings by 2029.

Uncover how Atlantic Union Bankshares' forecasts yield a $45.62 fair value, a 9% upside to its current price.

Exploring Other Perspectives

Four members of the Simply Wall St Community value Atlantic Union Bankshares between US$30.79 and US$61.86 per share, highlighting very different expectations. As you weigh those views against the upcoming Q2 earnings catalyst and the ongoing integration risk from recent acquisitions, it is worth exploring several perspectives on how those factors could shape the bank’s longer term performance.

Explore 4 other fair value estimates on Atlantic Union Bankshares - why the stock might be worth 27% less than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Atlantic Union Bankshares research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Atlantic Union Bankshares research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Atlantic Union Bankshares' overall financial health at a glance.

Curious About Other Options?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 30 companies in the world exploring or producing it. Find the list for free.

- Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com